On March 25, the House Financial Services Committee convened for a hearing titled “Tokenization and the Future of Securities: Modernizing Our Capital Markets.” Both parties agreed that tokenized securities are coming. The legal framework for them does not yet exist.

That gap — between a market already operating at scale and a statute that has not kept pace — is what the hearing was designed to document. For private market investors who have been watching tokenization move from talking point to institutional reality, the March 25 session is the clearest signal yet that the regulatory foundation for this market is being actively built.

The Market That Arrived Before the Rules

Congress was not theorizing on Wednesday. The tokenized RWA market reached $26.48 billion in distributed on-chain value as of March 23, up 5.25% in the prior 30 days alone, per rwa.xyz data. BlackRock, JPMorgan, Franklin Templeton, and Circle have all deployed institutional-grade tokenized products. The market exists, it is growing, and the statutory framework governing it is not keeping pace.

SIFMA’s Kenneth Bentsen testified that the securities industry strongly supports DLT and tokenization, while emphasizing that the strength of U.S. capital markets depends on preserving investor protections and market integrity safeguards. That framing — embrace the technology, preserve the guardrails — defines where mainstream institutional consensus sits heading into the legislative debate.

The urgency has a competitive dimension. Witnesses identified that Hong Kong, Singapore, Switzerland, the EU, and the UAE are all offering grants, publishing frameworks, and launching live pilots to capture the infrastructure layer for global capital markets. The question put to the committee: will American capital markets channel that demand, or will foreign competitors capture it?

What the Two Bills Actually Do

The hearing placed two pieces of draft legislation on the table. The Modernizing Markets Through Tokenization Act would require a joint SEC-CFTC study on tokenized derivatives, compelling both agencies to end their jurisdictional standoff. The Capital Markets Technology Modernization Act would codify the right of broker-dealers and transfer agents to use blockchain-based record-keeping under existing SEC rules.

Neither bill answers the foundational legal question. As one critic noted, the market modernization bill risks being “a delay mechanism dressed as action” — because neither measure addresses whether a tokenized asset is a security as a matter of law, leaving the SEC’s guidance as the only assurance market participants have that their tokenized instruments are governed consistently. That guidance could be revoked by a future commission.

The SEC and CFTC Already Moved Without Congress

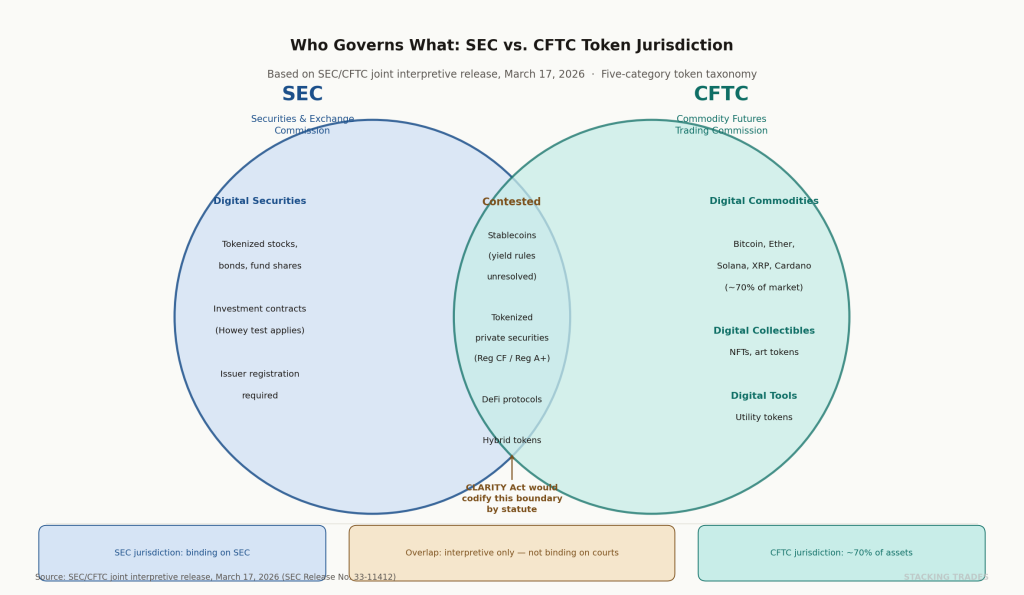

What makes the March 25 hearing significant is what happened eight days before it. On March 17, the SEC and CFTC issued a joint interpretive release — the most authoritative crypto asset guidance either agency has ever published.

The release established a five-category token taxonomy: digital commodities, digital collectibles, digital tools, stablecoins, and digital securities. Per Jones Day’s analysis, the definition of “digital commodity” parallels the CLARITY Act’s language and covers approximately 70% of all digital assets traded — meaning the CFTC, not the SEC, would govern the majority of the crypto market.

“After more than a decade of uncertainty, this interpretation will provide market participants with a clear understanding of how the Commission treats crypto assets under federal securities laws. This is what regulatory agencies are supposed to do: draw clear lines in clear terms.”

— SEC Chairman Paul S. Atkins, March 17, 2026

The important caveat: the interpretation is binding on the SEC and CFTC but not on federal courts. Private litigation exposure remains. And as both chairmen acknowledged, only Congress can provide statutory durability — which is precisely why the March 25 hearing mattered.

The CLARITY Act Clock

The hearing and the SEC/CFTC release are both best understood as supporting moves in a larger legislative sequence. Per FinTech Weekly, the CLARITY Act passed the House 294-134 in July 2025. The Senate Agriculture Committee advanced its portion in January 2026. The Senate Banking Committee markup — the next required step — is now targeted for the second half of April, following a stablecoin yield agreement reached in principle last week.

The CLARITY Act would determine by statute whether a given tokenized asset is a digital security under SEC jurisdiction or a digital commodity under CFTC jurisdiction. That single determination drives every subsequent legal question: which registration requirements apply, which exchanges can list the asset, which investor protections attach, and which enforcement mechanism governs any violation.

The timeline is tight. A late April Banking Committee markup leaves the bill’s remaining legislative steps a narrow window before election-year politics compress the fall calendar.

What It Means for Private Market Investors

For investors using Reg A+, Reg CF, or private placement structures, the tokenization regulatory moment has direct practical implications — most of which have not yet arrived but are being actively shaped right now.

The most immediate question concerns secondary market liquidity. Tokenized private company shares — the kind Robinhood explored with its EU equity products and that Republic has pursued through Mirror tokens — depend entirely on legal clarity about what those tokens are and who governs trading in them. If the CLARITY Act passes and codifies the SEC/CFTC taxonomy, a tokenized Reg CF security becomes a legally defined instrument with a clear regulatory home. Without that, platforms building liquidity infrastructure for these instruments are building on interpretive guidance that the next administration could reverse.

As Disruption Banking summarized: the hearing produced a bipartisan, on-the-record acknowledgment that the current framework is broken for this market. That does not mean Congress will fix it quickly. But it does mean the window for doing nothing has closed.

WHAT TO WATCH NEXT

- Senate Banking markup date. The April target is the most consequential near-term variable. A delay pushes real decisions into late 2026 and creates additional uncertainty for institutional capital deploying into tokenized structures.

- SEC exemptive rulemaking. In his March 17 speech, Chairman Atkins previewed possible exemptive rulemaking building on the taxonomy. Watch for a proposed rule in Q2 that translates the interpretation into operational requirements for issuers and exchanges.

- Trump family crypto provisions. Per CoinDesk, Ranking Member Maxine Waters raised the Trump family’s estimated $1 billion in crypto profits and their stake in World Liberty Financial. If Democratic opposition coalesces around those conflict-of-interest concerns, the April markup timeline becomes significantly more uncertain.

- TEFRA barrier. Testimony identified the Tax Equity and Fiscal Responsibility Act of 1982 — written to prevent bearer bonds — as an overlooked legal obstacle to tokenizing bonds on permissionless public blockchains. Watch for either legislative language or IRS guidance addressing this specific barrier.

- Securitize IPO. The tokenization firm that works closely with BlackRock plans to go public as soon as it receives SEC approval, likely in Q2. Its debut will be a live test of institutional appetite for publicly traded tokenization infrastructure.