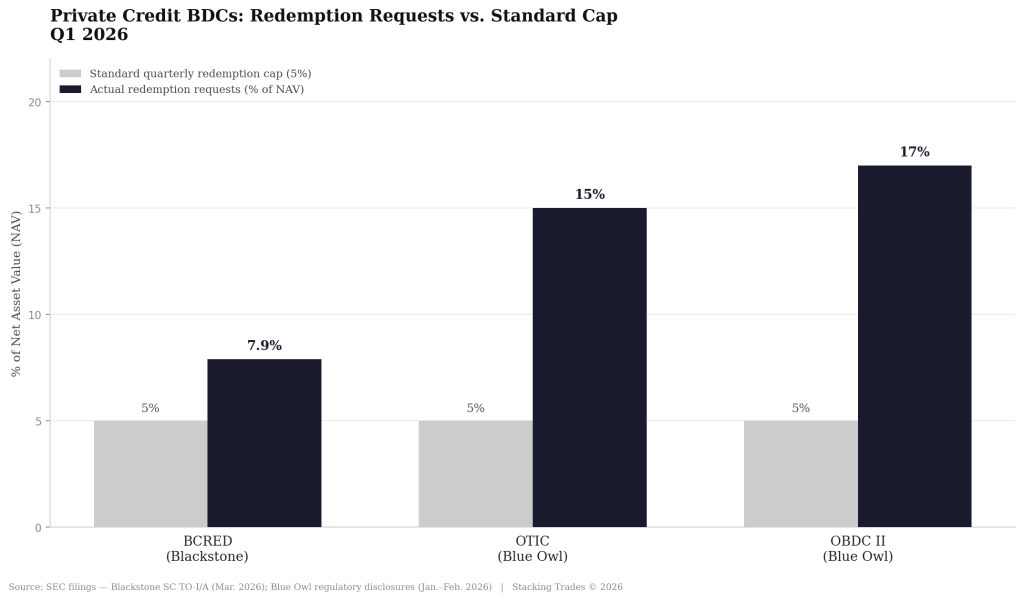

The headlines out of the private credit industry this quarter have been stark. Blackstone allowed investors to pull a record 7.9% of assets from its flagship $82 billion private credit fund — well above the standard 5% quarterly cap — after fielding roughly $3.8 billion in withdrawal requests. Blue Owl had it worse. Its technology-focused business development company saw redemption requests hit 15% of net asset value; a separate fund was gated entirely, with Blue Owl replacing quarterly tender offers with rateable return-of-capital distributions.

The industry response has been swift and, at times, defensive. Blue Owl argued it was “accelerating the return of capital,” not restricting it. Blackstone President Jon Gray said market “noise” had driven nervous retail investors toward the exits, pointing to BCRED’s 9.8% annualized return since inception as evidence the underlying portfolio remains sound. CALPERS, the California pension giant, was among the institutional buyers that swooped in to acquire loan assets Blue Owl sold at book value to fund the redemptions.

For investors who follow private market deal flow — including those active in Regulation A+ and Regulation Crowdfunding offerings — this story carries a real risk of misinterpretation. The BDC liquidity crisis is structurally specific. It does not apply to the exemption-based crowdfunding market, and conflating the two could lead to decisions that don’t match the actual exposure.

What Is Actually Breaking Down — and Why

Business development companies are a federally chartered structure, created by Congress in 1980, that package private credit — primarily loans to middle-market companies — and sell shares to retail investors. The key feature that makes them attractive also makes them fragile in stress conditions: they offer periodic liquidity. Under a typical non-traded BDC structure, investors can request to redeem up to 5% of net asset value per quarter. That cap exists precisely because the underlying loans are illiquid. Managers need runway to sell assets, collect repayments, or arrange credit lines before cash can move out the door.

When retail investors — less patient than institutional allocators who understand and accept lockups — become anxious and request more than 5% at once, the fund faces a mismatch between what it has promised and what it can deliver without forcing asset sales. That is what happened here. Blackstone resolved it by injecting roughly $400 million in firm and employee capital to offset excess redemptions, maintaining its record of meeting 100% of requests. Blue Owl’s OBDC II fund lacked that solution set and moved instead to gate the structure entirely.

“The product expanded faster than the communication infrastructure that should have accompanied it. That is the root cause of the current confidence issue.”

— Private Markets Insights, March 2026, citing Bloomberg Invest 2026 panel discussion

Morningstar, in its analysis of the BCRED situation, noted that Blackstone’s ability to use its own balance sheet as a liquidity buffer is not available to all managers. Smaller private credit funds offering semi-liquid structures but lacking a $82 billion sponsor’s resources are materially more exposed to the same dynamic. The lesson is not that private credit is broken. BCRED has outperformed leveraged loans by 360 basis points since inception. The lesson is that the structure carrying it to retail investors has stress points that were not clearly communicated.

Why Reg A+ and Reg CF Work Differently

Regulation A+ and Regulation Crowdfunding offerings are not semi-liquid funds. They are exempt securities offerings governed by the SEC under the Securities Act of 1933 — specifically, Title III of the JOBS Act for Reg CF and Regulation A for what is commonly called Reg A+. The investor relationship in these structures is categorically different from a BDC investor’s relationship with a redemption window.

When an investor puts capital into a Reg CF offering, they are buying an equity stake — or, in some cases, a revenue-share or debt instrument — in a private company. There is no fund manager offering periodic redemptions. There is no quarterly tender offer. There is no liquidity window that can be gated. The investor holds a security in a company, and that security becomes liquid only through a defined event: a company IPO, an acquisition, a secondary market transaction, or a structured repurchase. Reg A+ securities, notably, may be sold immediately to any investor without the one-year holding period that applies to Reg CF securities. That makes them more liquid by design, not less.

The table below summarizes the structural differences that matter for investors trying to separate the BDC story from the broader private markets story.

Structure

Liquidity promise

Redemption risk

Investor relationship

Non-traded BDC

(e.g., BCRED, OTIC)

Quarterly tender, typically 5% of NAV

High — mismatch between promise and underlying illiquidity

Fund shareholder with periodic redemption rightsInvestor relationship

Reg CF offering

None — exit via liquidity event only

None — no redemption window to gate

Direct equity/debt holder in issuer

Reg A+ (Tier 2) offering

Immediate secondary market sale allowed

None — securities are freely transferable

Direct securities holder; may trade without restriction

Interval fund / evergreen BDC

Periodic (quarterly or semi-annual) limited redemption

Medium — gating possible under stress; structure-dependent

Fund investor with contractual liquidity window

The DOL Rule That Changes the Stakes

All of this arrives in the same week the Department of Labor published a proposed rule that would make it materially easier for 401(k) plans to include private market investments. The rule, released March 30, creates a process-based safe harbor for fiduciaries who want to add alternatives — including private equity, private credit, and cryptocurrency — to their defined-contribution menus. Labor Secretary Lori Chavez-DeRemer said the rule would “show how plans can consider products that better reflect the investment landscape as it exists today.”

With roughly $12 trillion in defined-contribution assets sitting largely outside private markets, the opportunity is significant. So is the timing problem. The DOL is proposing to pipe more retail capital into structures that have just spent two months generating headlines about redemption failures and communication breakdowns. Critics were immediate. Sen. Elizabeth Warren described it as a mechanism for “Wall Street buddies” to access retirement savings. The Employee Benefit Research Institute flagged that current market instability complicates the outlook for adoption regardless of what the rule says.

More substantively, legal analysts at TD Cowen said they remain skeptical the rule will move fiduciaries off the sidelines without court confirmation that its safe harbor language holds against litigation. That is not a fast-moving variable. Employers that were sued over their 401(k) menus do not move quickly in response to proposed rules. They move in response to finalized rules — and then only after attorneys confirm the shield actually works.

What Issuers Should Take From This

For companies running Reg A+ or Reg CF campaigns, the noise around private credit redemptions is not your risk — but it is your opportunity. The BDC episode is teaching a generation of new private market investors a lesson about structure and liquidity. Some of those investors will be more cautious going forward. Others will be looking for private market exposure that does not carry a redemption-window risk, which is precisely what equity crowdfunding offers at the design level.

The sophistication gap that Blue Owl’s co-founder acknowledged — the gap between the pace of product expansion and the pace of investor education — is not unique to BDCs. Reg CF issuers that communicate clearly about what their securities are, when liquidity can be expected, and what milestones govern that timeline are positioned to attract investors who just received an expensive tutorial on what happens when those things go unexplained. The issuers that treat their post-raise investor communications with the same discipline they apply to the campaign itself are the ones who will benefit from the BDC sector’s credibility problem.

WHAT TO WATCH NEXT

- Whether any additional non-traded BDC gates redemptions in Q2 2026, particularly from managers without Blackstone-scale balance sheets to absorb excess requests.

- The DOL’s public comment period outcome on its 401(k) alternatives rule — the 60-day window will determine how quickly fiduciaries can act, and whether the rule survives legal challenge.

- Blue Owl’s orderly liquidation of OBDC II — if the fund returns capital at book value to all shareholders by mid-year, it becomes a model case study; if asset sales produce discounts, the narrative shifts toward credit quality concerns.

- SEC activity on Reg CF cap reform — the pending petition to raise the Reg CF limit from $5 million to $20 million gains relevance if institutional interest in the crowdfunding channel increases as BDC credibility falters.

- Whether any Reg A+ or Reg CF platforms explicitly position against BDC risk in their investor communications — that marketing angle has not been used publicly yet and may become a differentiator.