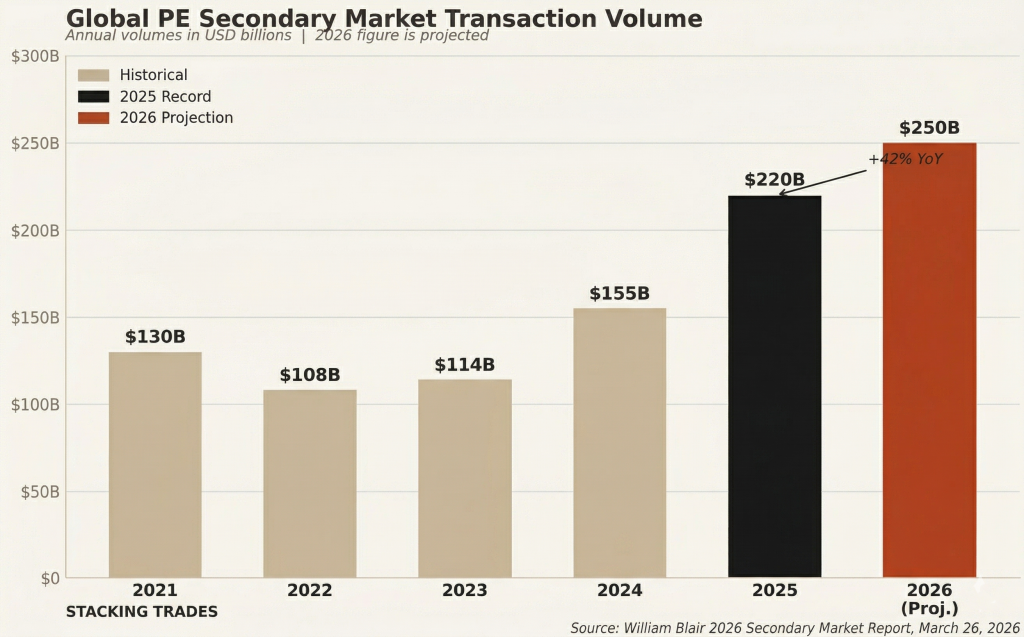

The private equity secondary market does not generate the kind of headlines that attach themselves to IPOs or earnings beats, but it has quietly become one of the most consequential corners of institutional finance. Last week, William Blair reported that the global secondary market hit $220 billion in transaction volume in 2025, a 42 percent year-over-year increase, with respondents in its annual survey projecting volume will climb to $250 billion this year. Some forecasters see the market reaching $400 billion by the end of the decade.

Then, on the morning of March 30, the Department of Labor proposed new rules that could eventually funnel a portion of the $13 trillion held in American 401(k) plans toward that same market. The timing was coincidental. The implications are not.

Why the Secondary Market Keeps Growing

The basic dynamic driving secondary market volume is straightforward: private equity funds are holding assets longer, and limited partners who need liquidity cannot simply sell shares on an exchange. The secondary market exists to solve that mismatch, connecting sellers who want out with buyers who want in at a discount to net asset value.

What has changed in recent years is the scale and sophistication of the supply side. In the annual survey, 81 percent of respondents cited a slow pace of distributions as a primary driver of deal flow, with the M&A slowdown adding further pressure. General partners who once relied on IPOs or strategic sales to return capital to investors are now turning to continuation vehicles — GP-led structures that allow them to transfer assets into new funds rather than sell them outright.

The secondary market has now hit a second consecutive record year and still represents only about 5 percent of the roughly $4 trillion in global buyout assets under management. There is room to grow.

The $250 billion projection for 2026 is broadly shared across the market’s largest buyers, with approximately 40 percent of survey respondents having deployed more than $1 billion in secondary transactions in 2025. Pricing is expected to hold. Ninety-six percent of those surveyed said they expect LP-led and GP-led pricing to remain stable or increase this year.

“The department’s days of picking winners and losers are over. Our rule clearly spells out that managers must evaluate any and all potential product offerings by following a prudent process.”

— Keith Sonderling, Deputy Secretary of Labor, March 30, 2026

What the DOL Rule Actually Does

The rule proposed Monday is more procedural than prescriptive, and that distinction matters for understanding what it does and does not open up. The proposal gives plan fiduciaries “maximum discretion and flexibility” in selecting alternative assets, while laying out a checklist of factors they must evaluate, including performance, fees, liquidity, and valuation.

What it does not do is put a private equity fund directly on your 401(k) menu. Mayer Brown partner Erin Cho put the limits plainly: plan participants are going to obtain only limited exposure through vehicles such as target-date funds, not standalone alternative funds. The legal architecture is still built around diversified wrappers, not direct fund access.

The rule is the direct product of an August 2025 executive order from President Trump directing the DOL and the SEC to relieve what the administration characterized as regulatory overreach that had kept 401(k) plans out of asset classes routinely used by pension funds and endowments. The Biden-era DOL supplemental statement that had cautioned plan sponsors against private equity allocations was rescinded shortly after the executive order was signed.

The path to finalization is not short. The proposal still requires a public comment period, likely 60 days, followed by a review and final rule. And looming over the entire process is Anderson v. Intel Corp., a case the Supreme Court agreed to hear on January 26, 2026, which could determine whether ERISA fiduciary-breach claims can survive the pleading stage when a plan offers private equity allocations inside a target-date structure. The pending litigation may push the DOL toward an explicit safe harbor provision for plan sponsors, without which many plan fiduciaries will remain on the sidelines regardless of what the final rule says.

The Capital Math

Even a small allocation from defined contribution plans would be transformative for private markets. Retirement assets in DC plans hit a record $48.1 trillion, per ICI data published in January. If the proposed rule eventually leads to one percent of that capital finding its way into private markets, the potential inflow would exceed $480 billion. Against a secondary market that did $220 billion last year, that is not marginal.

Asset managers understand this arithmetic. Fidelity and Vanguard are already in discussions with private equity firms about building the fund structures that could serve as access vehicles inside managed accounts and 401(k) plans. The logistical challenge is real: private funds are not built to process the continuous contributions, redemption requests, and valuation queries that come standard in a defined contribution plan. Building the infrastructure to accommodate those flows without violating the daily-pricing conventions most plan participants expect is a significant undertaking.

SEC Chair Paul Atkins has been public about his intention to work with the DOL on guardrails. The agency will ensure protections are in place because these investments can be illiquid and valuation is difficult. Atkins also made the structural argument that has been central to the industry’s lobbying position: there are roughly half as many public companies today as there were 30 years ago, and keeping retail investors locked out of private markets means keeping them away from a growing share of the economy.

The Case Against Going Fast

The counterargument has found serious voices. A financial watchdog analysis published in early March noted that the SEC’s March 4 roundtable on “responsible retailization” did not include a single panelist representing retail investors. Several panelists represented firms that manage private market investments and would directly benefit from expanded access.

The group also highlighted recent losses in the continuation vehicle market as a cautionary data point: Fortress Investment Group, Ares Management, and Blackstone collectively suffered what it characterized as a $1.4 billion loss in a Platinum Equity continuation fund. A separate Clearlake Capital continuation fund invested in Wheel Pros — which declared bankruptcy — resulted in a total wipeout for investors that included pension funds in New York, Connecticut, and Nevada.

These are institutional investors with dedicated alternatives teams. The question of whether retail savers, or the fiduciaries nominally watching over them inside a 401(k) plan, are positioned to underwrite that kind of downside is not settled.

TD Cowen analyst Jaret Seiberg said in a March research note that actual plan adoption may lag the rulemaking by years. Fiduciaries are unlikely to act until the courts have confirmed the new language protects them from litigation, and that process could take several years regardless of when the final rule is published.

What This Means for the Secondary Market Now

For investors already active in the secondary market, the near-term story does not hinge on retail access. The structural drivers — a lack of distributions, GP-led liquidity pressure, and a slow M&A market — are intact and are pushing volume higher on their own. The longer-term question is whether the potential entry of 401(k) capital creates pricing pressure at the better end of the market, compressing the discounts that secondary buyers have historically depended on.

The broader context is stark: private equity is now a mature industry, and the conditions that once amplified returns — declining rates, expanding multiples, abundant leverage — have largely passed. Alpha will increasingly come from operational value creation and disciplined entry pricing rather than market tailwinds. If new pools of retail capital flood into secondaries through passive wrappers, it could make disciplined pricing harder to maintain at the margin.

That is a 2028 problem, or maybe a 2030 problem. For now, the secondary market is heading into a third consecutive record year, the DOL rule is proposed not final, and the Supreme Court has yet to rule on the fiduciary question that could determine how quickly plan sponsors are willing to act. The opportunity is large. The timeline is longer than the headlines suggest.

WHAT TO WATCH NEXT

- DOL comment period deadline. The proposed rule is expected to open for a 60-day public comment window. Watch for statements from major plan sponsors, asset managers, and advocacy groups — particularly any coalition pushing for an explicit litigation safe harbor as part of the final rule.

- Anderson v. Intel Corp. at the Supreme Court. The Court granted certiorari on January 26, 2026. A ruling that raises the bar for ERISA fiduciary-breach claims against plan sponsors who offer alternatives could be the single most consequential event for the pace of adoption. Watch for oral argument scheduling.

- Secondary market pricing through Q2. Survey respondents across the largest secondary buyers project stable or rising pricing in 2026. Any meaningful softening in bid-ask spreads on LP-led transactions would signal a change in supply-demand dynamics worth tracking.

- The first named 401(k) product launch. The real signal that this is moving from policy to practice will be when a major recordkeeper — Fidelity, Vanguard, or a large insurance platform — announces a specific private markets sleeve inside a target-date or managed account structure. That announcement has not happened yet.

- SEC accredited investor rule revisions. The August 2025 executive order directed the SEC to consider revising the definitions of “accredited investor” and “qualified purchaser.” Any formal rulemaking proposal from the Commission would materially expand the universe of retail-accessible private fund products.