When the SEC raised the Regulation A+ Tier 2 offering cap to $75 million in late 2020, the intent was straightforward: give growing companies more room to raise public capital without the full burden of a registered IPO. Five years on, the cap looks less like a runway and more like a hard stop — one that successful issuers keep hitting, and that many others are avoiding entirely because the economics no longer make sense at that ceiling.

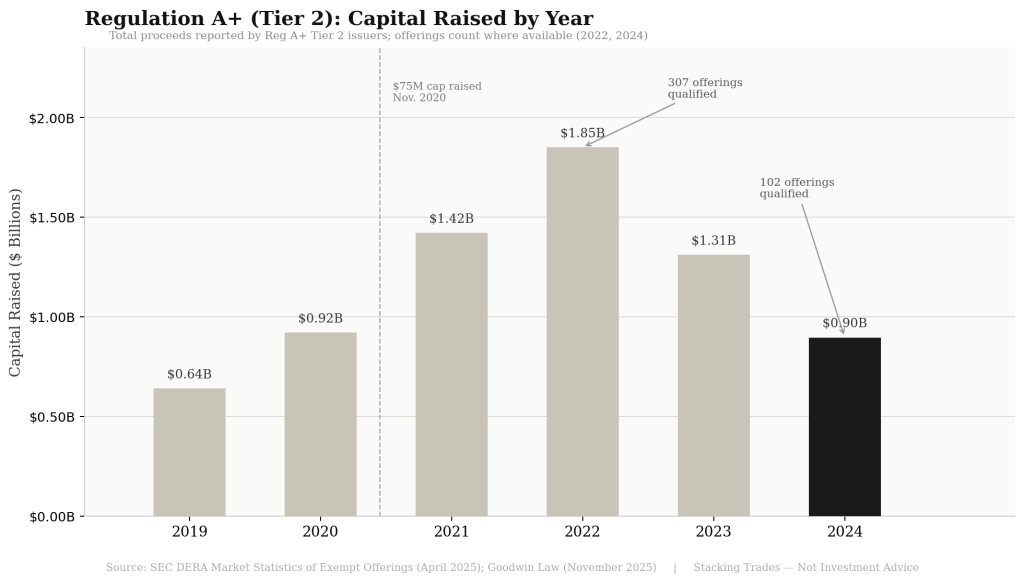

The numbers are stark. Reg A+ issuers raised approximately $1.85 billion in 2022 across roughly 307 qualified offerings. By 2024, that figure had collapsed to $896 million across just 102 qualified offerings — a 52% drop in proceeds and a 67% drop in deal count from peak. Meanwhile, Regulation D — available only to accredited and institutional investors — raised approximately $2.15 trillion in 2024 alone.

That gap is not just a market-structure curiosity. It represents a capital formation bottleneck that Congress and the SEC are now actively working to address, with competing proposals on the table and a Senate review process that could reshape the market’s architecture for the next decade.

Why the Cap Creates a Trap, Not Just a Limit

To understand the problem, you have to understand what happens when a Reg A+ issuer approaches $75 million. Issuers conducting continuous offerings who want to raise beyond the cap in a rolling 12-month period must file either a post-qualification amendment (PQA) or an entirely new offering statement on Form 1-A. Both options require SEC review and re-qualification before sales can resume.

The problem is that the PQA process creates serious operational friction precisely when issuers are most active. Goodwin’s analysis walks through the mechanics: if an issuer raises $5 million in each of the first two months of a continuous offering and then sells the remaining $65 million over the next ten months, it can only file a PQA at month 13 to qualify the $5 million that has freed up. If it wants to keep selling at pace, it has to file consecutive PQAs each month — each requiring legal opinions, auditor consents, and SEC review. The cost per amendment can run into the tens of thousands of dollars before professional fees are counted.

The SEC’s own 2018 rulemaking estimated that issuers spend approximately 731 hours preparing and filing a single Form 1-A offering statement. That burden compounds with every PQA. The message that sends to scaling companies: once you’re close to $75 million, the marginal cost of staying in Reg A+ starts to rival the cost of a full registered offering.

“The top reason cited by Goodwin clients for not utilizing Regulation A is that the dollar limit is too small given the amount of time and money it would take to launch an offering.”

— Goodwin Law, November 2026

Congress Steps In With a Double

The legislative response arrived in December 2025. Rep. Marlin Stutzman introduced the Regulation A+ Improvement Act of 2025 (H.R. 6541), which would double the Tier 2 cap from $75 million to $150 million annually and add an inflation-adjustment mechanism tied to the Consumer Price Index, recalibrated every five years. The House Financial Services Committee advanced the bill 28-23 on December 17, 2025, along party lines.

The bill was folded into the broader INVEST Act package (H.R. 3383), which passed the full House 302-123 on December 11, 2025. The bill was received in the Senate on December 15 and referred to the Senate Banking, Housing, and Urban Affairs Committee. As of early February 2026, no Senate action had been taken, with timing and the possibility of amendment remaining unclear.

The bipartisan House margin is notable — it signals genuine political demand for reform — but the Senate is a different committee. Senate Banking Chair Tim Scott has championed capital formation legislation in prior sessions, which proponents cite as a favorable signal. Whether the Reg A+ provisions survive Senate markup intact is a separate question.

The Cap Debate Is Bigger Than $150 Million

Among practitioners, $150 million is considered a floor, not a destination. Goodwin has formally called for raising the cap to at least $300 million. Former SEC Chair Jay Clayton suggested the appropriate number might be $1 billion to $2 billion. The SEC’s own small business forum considered $150 million as a reference point as recently as its 44th annual report.

These positions reflect a structural argument: Reg A+ was conceived as a bridge between the fully private markets of Regulation D and a registered public offering. At $75 million — or even $150 million — the bridge doesn’t reach far enough for companies that have found genuine product-market fit and need institutional-scale capital to continue growing before they’re ready for an S-1.

Goodwin’s November 2025 white paper also flagged a mechanic that has been largely overlooked: the annual PQA filing requirement creates a compounding burden for successful continuous-offering issuers that is entirely disconnected from investor protection. Their proposal would allow issuers to bank an additional $75 million of qualification capacity into the annual required PQA — so that active issuers don’t have to file separately every time the rolling 12-month window frees up capacity.

The Sector Concentration Problem Nobody Wants to Talk About

The strongest counterargument to expanding Reg A+ isn’t that the cap is set correctly — it’s that the market’s composition raises its own concerns. SEC DERA data found that financial sector issuers accounted for roughly 46% of aggregate financing sought under Reg A+ and an even larger share — approximately 64% — of actual reported proceeds. Real estate issuers, REITs, holding companies, and non-depository financial institutions dominate the top of the leaderboard.

The House Financial Services Committee minority noted this directly in the H.R. 6541 committee report: a $150 million ceiling would make the framework more attractive at scale for exactly these financial-sector vehicles, increasing retail exposure to illiquid and complex products. The concern is less about operating companies issuing Reg A+ shares and more about structured finance vehicles using the framework to access a retail investor base that may not have the tools to evaluate what they’re buying.

This is a real tension. Reg A+ was built around the idea of investor access — allowing unaccredited investors to participate in private-market-style offerings subject to investment limits. If the framework’s primary beneficiaries at scale are shadow finance vehicles and real estate vehicles rather than operating startups, lifting the cap may simply make an existing concentration worse before it gets better.

What the Decline in Filings Actually Signals

The 67% drop in Reg A+ offering volumes from peak is doing several things at once, and conflating them produces the wrong diagnosis. Part of the decline reflects the normalization of pandemic-era capital markets activity — Reg CF and Reg A+ both surged in 2020-2022 on the back of retail investor enthusiasm and low rates. The hangover was inevitable.

But the structural argument holds even after discounting the cycle. The drop in Reg A+ filings significantly exceeded the drop in broader capital market activity, suggesting that the framework’s structural costs — compliance overhead, cap constraints, the PQA cycle — are driving away precisely the mid-size issuers the tool was designed to serve. Companies that could realistically raise $50 million to $100 million and graduate toward a public listing are doing Regulation D rounds instead, limiting their investor base to accredited investors and forgoing the retail capital access that was Reg A+’s original value proposition.

That outcome benefits nobody the reform was designed to help: not the retail investors who are locked out of the earlier stages of company growth, and not the companies that could build a broader shareholder base as a stepping stone to eventual public markets.

WHAT TO WATCH NEXT

- Senate Banking Committee action on the INVEST Act — specifically whether the Reg A+ Improvement Act provisions survive markup intact, get amended to a different cap level, or get stripped from the package entirely.

- Whether the SEC under Chair Paul Atkins moves independently to raise the cap via rulemaking, as the agency has authority to do without Congress, and whether that would pre-empt or complement legislative action.

- DERA’s next exempt offering data release — watch whether 2025 Reg A+ volumes continue declining or stabilize in anticipation of legislative clarity, and whether the financial sector’s share of proceeds grows or contracts.

- Post-qualification amendment filing volume on EDGAR for active continuous-offering issuers: PQA frequency is the clearest leading indicator of how close issuers are to the cap in real time.

- Any formal SEC rulemaking on PQA review timelines and automatic qualification of non-material amendments, which Goodwin explicitly proposed and which could provide meaningful relief even without a cap increase.