Elliott Hill has been running Nike for a little over a year. In that time, he has pushed back on every strategic premise his predecessor left behind, rebuilt wholesale relationships that had been deliberately cut, and started dismantling the DTC-only thesis that eroded Nike’s retail presence over several years. He has also presided over seven consecutive quarters of gross margin decline, a stock that touched eleven-year lows in April, and an acknowledgment that the comeback is moving slower than he would like.

The Q4 FY2026 print, scheduled for June 30, is the formal close of Hill’s first full fiscal year. What it won’t be is a clean report. But investors who focus only on the headline revenue number — guided down two to four percent year-over-year — will miss the more consequential signals buried inside the quarter. Nike’s investment case right now is not about whether this year is good. It’s about whether the foundation being built is real.

What “Win Now” Actually Did to the Business

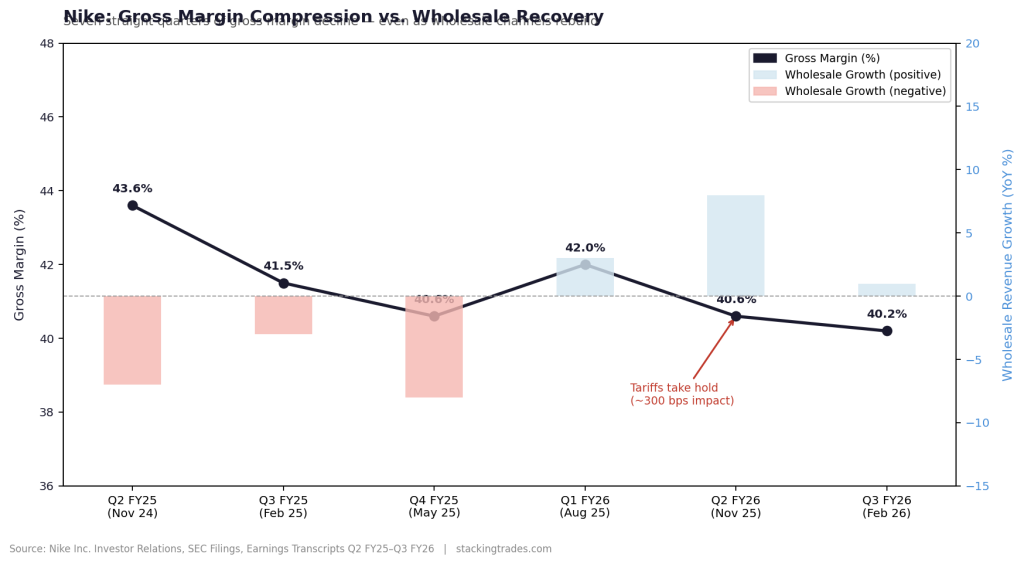

Hill’s restructuring program is called Win Now, and the name is at least partially misleading. The strategy was never about immediate revenue acceleration. It was about resetting the channel economics Nike had distorted under the previous leadership, pulling excess inventory out of the market, and returning the brand to sport-specific credibility. Those actions have measurable costs, and they have been showing up in the income statement every quarter since Hill took over in October 2024.

In Q3 FY2026, the most recent reported quarter, Nike’s gross margin fell to 40.2 percent — down 130 basis points from a year earlier and including 300 basis points of direct impact from U.S. tariffs in North America. Net income dropped 35 percent. Nike also took a $230 million restructuring charge for employee severance concentrated in supply chain and technology. These are not numbers that signal a turnaround arriving on schedule. They signal one that is still in the middle of being engineered.

The wholesale channel tells the better story. After years of Nike pulling back from retail partners to prioritize its own digital storefronts, wholesale revenue has grown in each of the past two reported quarters — up eight percent in Q2 and up one percent in Q3, with North America wholesale specifically up eleven percent in the most recent period. Foot Locker shelf space has expanded, and Nike has moved toward a return to Amazon after deliberately pulling off the platform under John Donahoe. The wholesale rebuild is one of the clearest execution wins of Hill’s tenure so far.

“While our comeback is taking longer than I would like, I am confident that our progress in the areas we prioritize points to where we are ultimately heading across our portfolio.”

— Elliott Hill, President & CEO, Nike Inc., Q3 FY2026 Earnings Call, March 31, 2026

The China Problem Is Structural, Not Seasonal

Greater China is where the turnaround case gets complicated. Revenue in the region fell ten percent in Q3 and is guided to fall approximately twenty percent in Q4, as Nike accelerates marketplace cleanup and intentionally reduces wholesale sell-in to align supply with full-price demand. Management has been explicit that this cleanup will continue into fiscal 2027. Hill told analysts on the Q3 call that improvements in China are “not happening at the level or the pace we need.”

The structural dimension is harder to fix than inventory. Adidas has gained measurable ground in China, and domestic brands including Anta and Li-Ning have captured significant share in sport-specific categories where Nike once held dominant positioning. Goldman Sachs, JPMorgan, and Bank of America all downgraded the stock following the Q3 print, with Bank of America flagging that return-to-growth expectations had been pushed from Q1 FY27 to at least Q3 FY27. China recovery remains the variable that no amount of wholesale re-engagement in North America can fully offset.

The Margin Math That Actually Matters for June 30

Tariffs are the most immediate financial variable heading into Q4. Nike’s exposure is substantial — the company has flagged approximately $1.5 billion in annualized incremental product costs from U.S. tariff policy, with roughly 250 basis points of gross margin impact expected in Q4 alone. CFO Matthew Friend guided for Q4 gross margin to be down 25 to 75 basis points sequentially, which would represent an improvement over the severity of compression seen in Q3. That sequential improvement is the near-term number worth watching. Nike is not unusual in facing this pressure, but its exposure runs directly through a Vietnam-heavy supply chain that has few short-term alternatives.

Management has committed to gross margin beginning to expand in Q2 FY27 — the quarter ending November 2026 — as tariff headwinds begin to anniversary and Win Now cleanup costs roll off the income statement. That is a credible timeline, but it is also a forecast that requires tariff policy to remain stable and China recovery to proceed at some pace faster than current trends. Both assumptions carry meaningful uncertainty right now.

Running Is the Signal Investors Should Watch

Inside the noise of the headline numbers, Nike Running has been one of the clearest early signs that the brand reset is working. Running grew more than twenty percent in Q3 in North America, with management citing it as the category where the sport-focused product strategy has advanced furthest. Basketball was up high single digits. Global Football grew double digits. These are not incidental gains — they represent the category proof of concept for a strategy Hill is now trying to replicate across the full portfolio in fiscal 2027.

Sportswear is the gap. That segment — which includes the Classics business that drove significant revenue under the prior strategy — declined double digits globally in Q3. Nike intentionally pulled more than four billion dollars of Classics revenue from peak levels as part of its repositioning, creating roughly five percentage points of headwind to Q3 reported results. The Sportswear drag is expected to ease as the portfolio shift completes, but the exact timing has been repeatedly pushed later than original guidance implied. Q4 commentary on Classics inventory levels and Sportswear sell-through will be one of the clearest forward signals available from the June 30 print.

What the June 30 Print Needs to Show

The Q4 FY2026 report is not a recovery announcement. The setup makes that nearly impossible — Greater China guided down twenty percent, SG&A guided flat to slightly down, revenue guided to decline. What Q4 can do is demonstrate execution discipline: that the channel reset is proceeding as described, that North America wholesale momentum is holding, and that the gross margin trajectory is turning in the direction management committed to. Sequential margin improvement, even modest, removes the biggest near-term bear case.

Hill has acknowledged the frustration. The harder question heading into fiscal 2027 is whether the sports-first product strategy can compound from Running into the rest of the portfolio fast enough to offset the ongoing China reset — and whether a tariff environment that remains fluid will allow the margin recovery timeline to hold. The June 30 earnings call will not resolve all of that. But it will show whether the first year set the foundation Hill claims it did, or whether the rebuild has further to go than management has been willing to say.

What to Watch Next

- Q4 gross margin sequential direction. Management guided Q4 gross margin down 25 to 75 basis points. Any result at the favorable end of that range — or any commentary indicating the tariff impact is narrowing faster than expected — is the single most meaningful forward signal for the FY27 margin recovery thesis.

- North America wholesale order books into fall. Q3 showed North America wholesale up 11 percent, with management flagging strong order books. Watch for specific commentary on fall 2026 sell-in commitments and whether key retail partners including Foot Locker and Dick’s Sporting Goods are expanding Nike allocations or stabilizing at current levels.

- Greater China sell-in guidance for Q1 FY27. The region is guided down roughly 20 percent in Q4 as Nike deliberately reduces partner inventory. The first quarter where China year-over-year comparisons begin to normalize — expected around Q2 FY27 — is when the recovery narrative becomes quantifiable. Listen for any revision to that timeline on the June 30 call.

- Sportswear segment trajectory. The Classics reset has cost Nike several billion dollars in revenue and five-plus points of quarterly growth. Management has indicated the pullback is largely complete. Any Q4 commentary showing Sportswear stabilizing — rather than continuing to decline double digits — would be early evidence that the drag is turning into a tailwind.

- Tariff scenario planning from CFO Friend. The Section 301 investigations launched after the IEEPA ruling have 12-to-18-month resolution timelines. Nike’s Vietnam exposure means any change in applicable tariff rates would directly affect the gross margin expansion commitment for Q2 FY27. Watch for any updated tariff sensitivity disclosures on the call.