Sam Altman spent years calling advertising a last resort. He was right to be cautious. He was also, eventually, overruled by the math.

On February 9, 2026, OpenAI activated paid advertising inside ChatGPT for free and Go-tier users in the United States. Six weeks later, the pilot had crossed $100 million in annualized revenue. By April, the company had opened a self-serve Ads Manager to any U.S. business. On June 6, Benji Shomair, OpenAI’s VP of Monetization, confirmed the pilot was live in the United Kingdom — the first market outside North America, Australia, and New Zealand — with Japan, South Korea, Brazil, and Mexico to follow. An advertising business that did not exist five months ago is now operating on four continents.

The pace is not an accident. OpenAI is heading toward a September IPO targeting a valuation above $1 trillion. The advertising business is part of the filing narrative whether it appears as a formal line item in the S-1 or not.

The Free Tier Problem That Ads Are Supposed to Solve

ChatGPT reached 900 million weekly active users in February 2026, roughly doubling its base from a year earlier. Of that audience, approximately 95 percent pay nothing. The paid subscriber base — Plus, Pro, Team, and Enterprise — accounts for around 50 million users. That ratio is the structural pressure the ad business is designed to address.

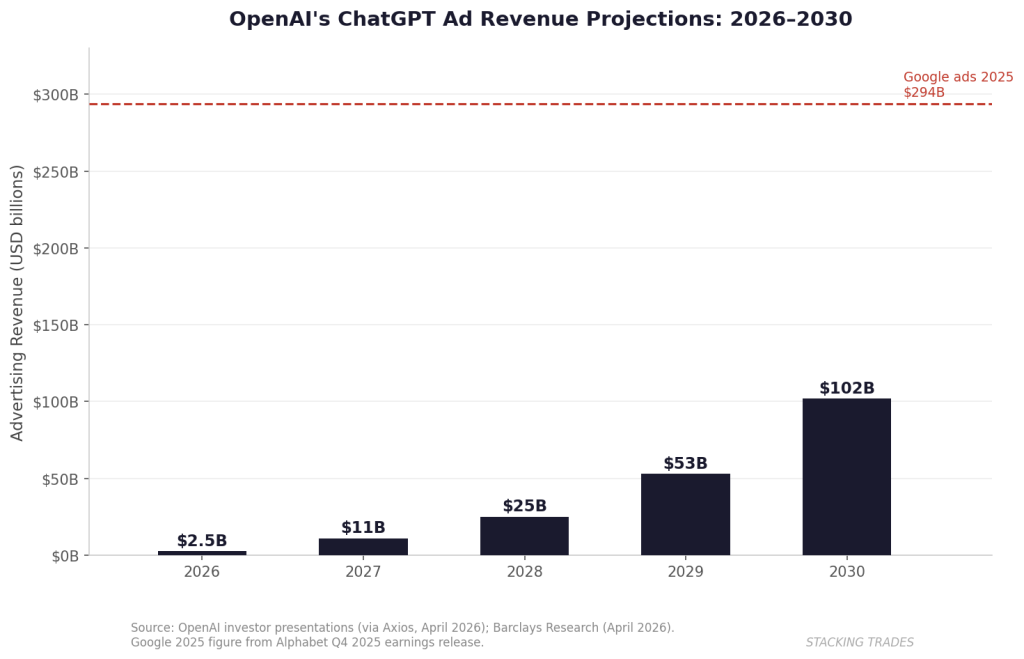

OpenAI is projecting $2.5 billion in ad revenue for 2026, rising to $11 billion in 2027, $25 billion in 2028, $53 billion in 2029, and $100 billion by 2030. Those projections, shared with investors and first reported by Axios in April, assume the platform reaches 2.75 billion weekly users by the end of the decade. The forecasts are not modest. Google’s total advertising revenue in 2025 was approximately $294 billion; OpenAI’s 2030 target represents about one-third of that, built from scratch, in four years.

Barclays published a separate projection in April that arrived at $102 billion by 2030 through a model built on user growth, query volume, and revenue per query. The methodology is different from OpenAI’s internal numbers; the destination is nearly identical. That alignment between an outside sell-side model and the company’s own investor presentations is what gives the projection real weight.

What “Intent Advertising” Is Actually Worth

The initial launch CPM of $60 — roughly three times what Meta charges on Facebook and Instagram — signaled how OpenAI was positioning the product from day one: not as a reach channel, but as a high-intent environment where users arrive with specific problems, not passive scroll habits. A person asking ChatGPT how to refinance a mortgage is more commercially actionable than a person encountering a mortgage ad in a news feed.

That framing is now being tested against a much wider advertiser base. The $200,000 minimum commitment that characterized the closed beta was eliminated in May when OpenAI opened its self-serve Ads Manager to any U.S. business, adding CPC bidding at a recommended starting rate of $3 to $5 per click. CPMs reportedly drifted down to $25 as the advertiser pool widened in April — a natural consequence of moving from curated brand partners to open access. The question now is whether the intent premium holds at scale or gradually compresses toward something closer to search-display blended rates.

“Creative variation has been a real key to success.”

— Benji Shomair, VP of Monetization, OpenAI, press roundtable, May 2026

The remark is revealing. In a high-intent environment, the context of a query shapes what an ad needs to do in ways that standard creative testing on Google or Meta does not surface. Someone researching running shoes mid-conversation requires a different creative execution than someone browsing a shopping feed. OpenAI is accumulating the behavioral data to act on that — but it is only four months into building that signal.

The Infrastructure Being Built in Real Time

Conversion tracking arrived in May. Cost-per-action bidding entered early access on June 5. Daily budget controls, DMA-level geo-targeting, custom audience targeting, and dynamic call-to-action units have all shipped since April. The build cadence is faster than anything Google or Meta attempted in their equivalent early periods — but both of those companies had years of advertising infrastructure elsewhere in their organizations before they launched the products that made them dominant.

OpenAI has hired quickly. David Dugan joined as Global Head of Ads in late March and confirmed Zalando as a UK launch partner. Technology integrations include Criteo, StackAdapt, Adobe, Kargo, and Pacvue. Shomair framed the access expansion explicitly around mission rather than margin: “Expanding access to advertising helps support our broader mission of making frontier AI more accessible to more people.” Whether investors read it as vision or as cover for a revenue necessity will depend on what the audited financials eventually show.

The measurement gap is the most material near-term risk. Early advertisers have reportedly complained about the absence of robust attribution tools, and the product feed ad format has moved slowly due to inconsistent merchant data quality. Those are solvable problems — Google’s first years were defined by similar limitations — but they constrain enterprise budget allocations while they persist. At $2.5 billion projected for 2026, any significant delay in measurement infrastructure arriving would leave the year-end number short.

What the Ad Business Changes About the IPO Math

OpenAI is projecting $14 billion in operating losses for 2026. Subscription revenue, enterprise licensing, and API fees are the current primary contributors. Advertising adds a structurally different revenue profile: high-margin, scaling with usage rather than new contract activity, and not dependent on compute provisioning in the way model inference is.

For the roadshow narrative, the advertising line matters more as a trajectory than as a current number. A platform with 900 million weekly users that generated $100 million annualized in six weeks, opened to self-serve in four months, and is now live in multiple international markets is a demonstrably functional ad business — not a pilot. How Goldman Sachs and Morgan Stanley frame that trajectory in the S-1 language will influence whether institutional investors treat the ad revenue projection as a credible second engine or as aspirational modeling. The Anthropic filing, which arrived first on June 1, will set the disclosure baseline that OpenAI’s prospectus has to meet or exceed on this exact question.

There is also a competitive dimension that the IPO framing will need to address. Google’s advertising revenue in 2025 reached approximately $294 billion. Meta earned close to $200 billion. Both companies have spent years building measurement infrastructure, advertiser relationships, and attribution pipelines that OpenAI is assembling in real time. The question is not whether ChatGPT can take share from those platforms — it is whether it can do so fast enough to matter to the revenue model before the company’s burn rate requires a resolution. The AI IPO sequencing between Anthropic and OpenAI means whoever discloses audited gross margins first sets the sector multiple. The advertising line, small as it is today, changes both the numerator and the story.

What to Watch Next

- The OpenAI public S-1 on SEC EDGAR. The first audited disclosure of advertising revenue as a formal line item — and whether the $2.5 billion 2026 projection is incorporated into the prospectus as formal guidance or presented as an internal estimate — will be the clearest signal of how central the ad business is to the IPO valuation case.

- CPM stability through Q3. The drop from $60 to $25 as the advertiser pool widened is worth tracking. Whether pricing stabilizes at self-serve levels or continues to compress will determine the actual revenue contribution and whether the Barclays $102 billion model holds its assumptions.

- Japan, South Korea, Brazil, and Mexico activation dates. Each market adds to the addressable user base for advertisers. The pace of international rollout through Q3 will be the most visible indicator of whether the self-serve infrastructure can support simultaneous multi-market builds.

- Measurement and attribution tool launches. Cost-per-action bidding entered early access on June 5. Full rollout and any disclosure of conversion rates against Google and Meta benchmarks would give enterprise advertisers the comparison data they need to commit significant budget — and give analysts a basis for adjusting the 2027 projection.

- Google and Meta response. Neither company has formally repositioned a product against ChatGPT ads. Any announcement of a conversational ad format from Google or an AI-native intent product from Meta would directly challenge OpenAI’s pricing premium and force a reassessment of the long-term market share assumptions underlying the 2030 projections.