The headline numbers from investment crowdfunding’s best year in half a decade tell one story. The platform-level data underneath them tells a different one. Regulation Crowdfunding raised $378 million in 2025 and Regulation A+ surged 124% to $546 million, bringing the combined market to just under $925 million — the strongest annual performance since the 2021 peak. But the top-line growth obscures a structural shift that sophisticated investors evaluating crowdfunding as a deal source need to understand: the platforms hosting these offerings have spent the past two years diverging sharply in strategy, revenue model, and the type of investor they are actually built to serve.

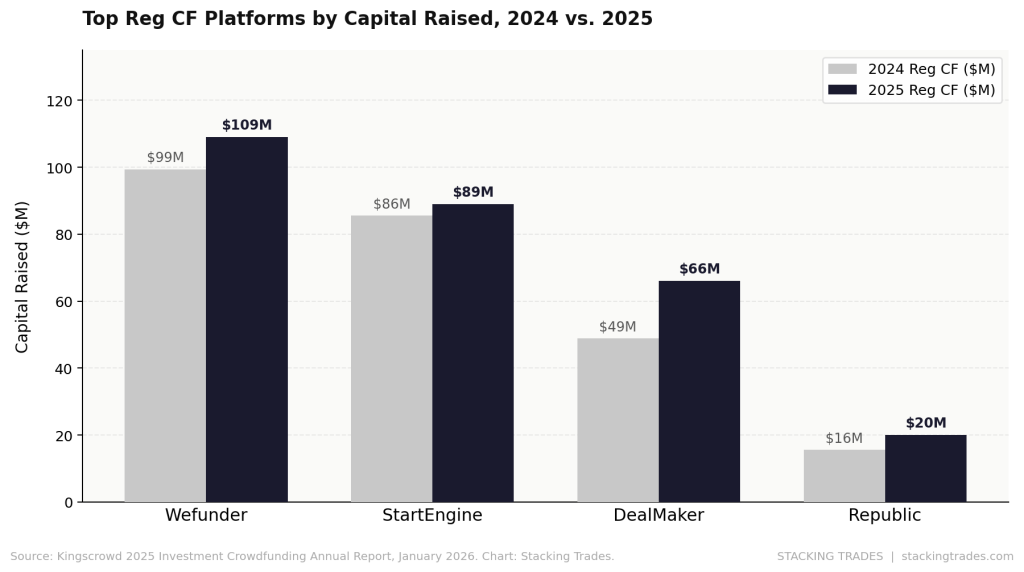

The Reg CF market is now functionally dominated by three players. Wefunder led with $109 million raised in 2025, followed by StartEngine at $89 million and DealMaker at $66 million. Republic — the platform most associated with curation and accredited investor appeal — finished fourth at $20 million in Reg CF, the same ranking it held in 2024 despite broader market growth. According to Sacra, Wefunder holds approximately 33% of total Reg CF dollars raised, compared to StartEngine’s 24%. Those four platforms collectively account for the vast majority of the market. The question for accredited investors — who face no investment caps under Reg CF and can treat crowdfunding platforms as genuine deal discovery infrastructure — is not which platform is biggest. It is which platform’s business model creates the incentive structure most aligned with deal quality over deal volume.

Wefunder: Volume as a Business Model

Wefunder’s dominance in Reg CF is structural rather than accidental. The platform was a primary architect of Reg CF itself, lobbying for the JOBS Act provisions that created the exemption, and it has operated since then on a philosophy of open access: founders self-serve into the platform, campaigns launch with relatively low friction, and the community of over 1.5 million registered investors — the largest in the Reg CF market — provides the distribution. Wefunder facilitated over 367 deals in 2025, more than any other platform by deal count, and maintains a lean cost structure that, per Sacra data, produced $2 million in net profit on $16.8 million in revenue in 2024.

That lean model has a corollary. Wefunder’s open-platform approach means deal quality is variable. The platform performs mandatory “bad actor” checks and requires SEC-mandated disclosures, but it does not apply the kind of proprietary vetting that characterizes Republic’s acceptance process. For investors browsing Wefunder’s deal flow, the volume is the signal and the noise simultaneously — a high-volume platform with a broad investor base rewards issuers that can generate momentum quickly, and Wefunder’s recommendation engine visibly surfaces campaigns that attract early investment. That dynamic benefits narrative-driven consumer brands and founders with existing communities. It does not self-evidently filter for investment quality in the way that lower-volume platforms with stricter acceptance processes do.

Republic: The Curation Play Pivoting Up-Market

Republic’s $20 million in 2025 Reg CF volume understates its strategic position. The platform accepts roughly 5% of companies that apply, giving it the most selective intake process in the U.S. crowdfunding market and the highest median deal quality ratings in Kingscrowd’s cross-platform analysis. Republic investors skew toward repeat buyers in technology, AI, and blockchain — a more sophisticated, higher-check-size cohort than the average Wefunder backer. The platform has also built out regulatory infrastructure that no domestic competitor matches: it is licensed across the U.S., UK, and EU to support fundraising, secondary trading, and financial services across jurisdictions, and it operates a registered alternative trading system for secondary market transactions.

The more interesting strategic move is Republic’s development of Mirror Tokens — digital assets that track the value of private securities in well-known private companies — launched by Republic Europe (formerly Seedrs) in August 2025. The product, structured as debt instruments, allows investors to gain exposure to companies like SpaceX or ByteDance without direct share ownership, and the ByteDance mirror offering was available through Reg D for accredited investors. Republic Capital, the platform’s institutional arm, reported two IPOs in 2025 with three queued for 2026. Republic Film raised over $31 million from more than 40,000 investors in the same period. The picture that emerges is of a platform actively expanding its footprint from retail crowdfunding into multi-asset private markets infrastructure — a very different business from where it started, and one where Reg CF volume is a credibility layer rather than the core revenue driver.

StartEngine: The Infrastructure Bet

StartEngine is the most vertically integrated player in the domestic market. It operates a FINRA-registered broker-dealer, a registered transfer agent, and an SEC-registered Alternative Trading System — the StartEngine Secondary marketplace — that allows investors to trade shares in private companies post-offering. The platform acquired SeedInvest in 2023, adding a later-stage, VC-backed deal flow and expanding its investor base to over 2.1 million. StartEngine generated $70 million in revenue in the first half of 2025 alone, tripling year-over-year, with a significant portion driven by StartEngine Private — a service launched in late 2023 that gives accredited investors access to funds holding shares in late-stage private companies.

That last product is the most significant development at StartEngine from an accredited investor standpoint. StartEngine Private generated 57% of 2024 revenue in its first full year of operation, per the company’s SEC 10-K filing. The product sits structurally between traditional crowdfunding and private equity: accredited investors can access pooled vehicles invested in pre-IPO names, with the secondary marketplace providing a path to liquidity that most private market products lack. StartEngine’s stated goal is to facilitate $10 billion in total platform funding by 2029, a target that implies the company views itself as a retail private markets destination rather than a Reg CF utility. The secondary marketplace currently has over 400 issuers signed up, though only 25 companies had been quoted to date as of the company’s last 10-K.

DealMaker: The White-Label Infrastructure Nobody Talks About

DealMaker Securities does not compete for the same investor attention as Wefunder or Republic. It operates primarily as white-label infrastructure for large Reg A+ raises — providing the backend compliance, payment processing, and investor onboarding that large issuers need to run major campaigns without building those systems themselves. DealMaker led all platforms in Reg A+ volume in 2024 with $123 million — more than half of the entire Reg A+ market — and processed over $300 million in the first half of 2025. Its largest raises include a $75 million Newsmax offering that dominated the Reg A+ leaderboard in 2025.

DealMaker recently moved its headquarters to New York and began accepting USDC payments, signaling ambitions beyond its traditional compliance-services positioning. For accredited investors, DealMaker-hosted raises tend to be larger, later-stage, and consumer-facing — a different risk and return profile than the early-stage company-building focus of Wefunder or Republic’s curated offerings. The platform is less a deal discovery destination than a capital markets execution layer.

“The strongest performers in 2026 and beyond will likely be the platforms and issuers that operate like real capital markets participants, not simply marketers running a campaign.”

— Kingscrowd, 2025 Investment Crowdfunding Annual Report, January 2026

What the Differentiation Actually Means for Deal Selection

The platforms are not interchangeable, and the distinction matters more as the market matures. Reg CF raised $378 million in 2025 across a shrinking number of new offerings — 20% fewer launches than in 2024, with capital concentrating in a smaller cohort of higher-quality raises. Nine campaigns hit the $5 million cap, triple the prior year. One hundred and one crossed $1 million. The median equity raise, however, sat at $194,000, meaning half of all issuers raised less than that. As we covered earlier this year, a formal SEC petition to raise the Reg CF cap from $5 million to $20 million is now on file — if that passes, the platforms with the infrastructure and investor base to handle larger, more complex raises will capture a disproportionate share of the expanded market.

For accredited investors using these platforms as deal flow infrastructure, the practical framework is straightforward. Wefunder provides the broadest deal flow with the highest volume and the most community-driven discovery dynamic — useful for sector scanning, less useful for pre-screened quality. Republic provides the tightest acceptance filter with the most sophisticated investor base and the clearest path toward multi-asset private markets exposure, including secondary liquidity. StartEngine provides the most complete vertical stack — primary offering, secondary trading, and accredited-investor fund access — and is building toward a retail private markets destination that competes with emerging players like EquityZen and Forge rather than traditional crowdfunding. DealMaker operates at a scale that requires a different kind of due diligence: the platform itself does not vet issuers the way Republic does, so the deal quality assessment falls to the investor.

The consolidation that is not being talked about is less about M&A and more about capability divergence. The market is quietly splitting into two tiers: platforms that are building durable capital markets infrastructure — secondary liquidity, accredited investor products, multi-jurisdiction licensing, institutional relationships — and platforms that remain primary campaign marketplaces. In a market posting near-record volumes but also facing direct competition from tokenized private equity, retail interval funds, and an expanding universe of accredited-investor products, the former tier has a structural advantage that compounding investor bases and regulatory licenses make very difficult to close.

What to Watch Next

- The SEC’s response to petition 4-889 — If the Reg CF cap rises from $5 million to $20 million, the platforms with existing infrastructure for larger, more complex raises — primarily StartEngine and Republic — are positioned to capture the incremental market. Wefunder’s open-platform model may require adjustments to handle the compliance and investor relations demands of larger issuers at scale.

- Republic’s Mirror Token regulatory treatment — The SEC has not issued formal guidance on how Mirror Tokens — debt instruments designed to track private company valuations — fit within the existing securities framework. Any enforcement action or formal classification would materially affect Republic’s most innovative product and could set precedent for how other platforms approach tokenized private market exposure.

- StartEngine’s secondary market liquidity metrics — The platform has over 400 issuers signed up for StartEngine Secondary but only 25 companies quoted as of its last 10-K. The ratio of enrolled issuers to active secondary market quotes is the most direct test of whether the secondary liquidity narrative is converting to actual investor utility or remaining a product feature in search of adoption.

- DealMaker’s capital markets ambitions — The New York headquarters move, USDC payment acceptance, and $300 million first-half 2025 volume suggest DealMaker is positioning for something larger than white-label compliance services. Whether that is a formal broker-dealer buildout, a move into direct secondary trading, or an acquisition play will become clearer in mid-2026.

- Competition from tokenized private market products — Robinhood’s launch of tokenized equities in the EU, BlackRock’s tokenized fund expansion, and the broader retail push into alternative assets all put pressure on crowdfunding platforms from the outside. If accredited investors can access late-stage private companies through tokenized wrappers on mainstream brokerage platforms, the crowdfunding market’s value proposition narrows to what it does differently — community, early-stage access, and regulatory pathways for non-accredited investors.