Every year, the equity crowdfunding conversation centers on the same two or three names. Wefunder has the community. Republic has the brand. StartEngine has the secondary market ambitions. DealMaker, meanwhile, quietly processed more than $500 million in capital raises across 2025 — roughly $57,000 every hour — and dominated Reg A+, the highest-dollar exemption in the retail capital stack, by a margin that isn’t close.

The gap between DealMaker’s market position and its coverage is one of the more interesting disconnects in private markets right now. Understanding why it exists — and what it says about where the crowdfunding industry is actually heading — is worth the time for any investor paying attention to this space.

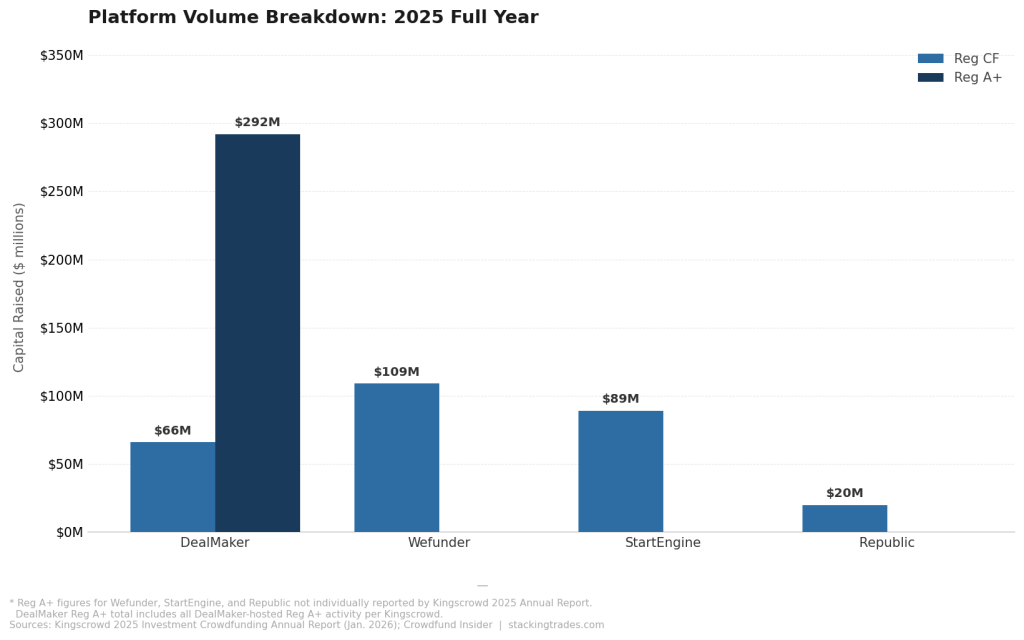

The Volume Leadership Nobody Talks About

Per the Kingscrowd 2025 Investment Crowdfunding Annual Report, DealMaker raised $292 million in Reg A+ last year — more than 50% of all capital raised under the exemption across the entire U.S. market. Combined with $66 million in Reg CF activity, DealMaker processed more than $358 million across both exemptions in 2025 alone. Its Reg A+ volume grew 157% year-over-year. By the company’s own accounting, total capital processed for the year cleared $500 million across all raise types on the platform.

In Q1 2026 — a difficult quarter for the category overall, with Reg CF volume falling 29% and Reg A+ dropping 45% from the prior year — DealMaker still led the Reg A+ market with $62.7 million raised, more than five times StartEngine’s second-place total of $12.3 million. In a quarter defined by contraction, DealMaker’s lead over the field widened.

Why the Model Is Different — and Why It Matters

Wefunder and Republic are marketplaces. Investors come to their platforms, browse deals, and invest. The platform controls the discovery layer and owns the investor relationship. DealMaker operates on a fundamentally different logic: it is infrastructure. Companies using DealMaker run their raises on their own branded pages, own their investor data, and control the relationship with every person who invests. DealMaker provides the compliance engine, payment processing, transfer agent services, and investor relations tools underneath — invisibly.

That white-label structure is the source of DealMaker’s margin advantage and its strategic optionality. A marketplace earns from deal discovery. An infrastructure provider earns from every transaction that flows through its rails, regardless of where the investor found the deal. As the crowdfunding market matures and capital concentrates in fewer, larger raises — exactly the pattern Kingscrowd documented in 2025, with 20% fewer new Reg CF offerings but meaningfully higher average raise sizes — the infrastructure provider benefits from higher per-raise economics rather than being diluted by shrinking campaign counts.

“We cannot afford to leave billions of dollars in potential economic impact on the table. Expanding these capital-raising frameworks will create jobs, fuel innovation, and level the playing field for founders outside of traditional financial hubs.”

— Rebecca Kacaba, CEO and Co-Founder, DealMaker, testimony before the U.S. House Financial Services Committee, February 26, 2025

From $2 Billion to $5 Billion: The Trajectory the Numbers Tell

DealMaker was founded in 2018 by capital markets lawyers — a founding story that shaped what the company built. It entered the U.S. Reg CF market in July 2022, later than its peers, and reached its first billion in cumulative capital processed later than Wefunder or StartEngine. But the trajectory accelerated sharply. The company announced its New York City headquarters in April 2025, citing the need to be closer to the capital markets ecosystem it was increasingly serving. By November 2025, total cumulative capital raised had crossed $2.3 billion and the company closed a $20 million financing round from Information Venture Partners and existing partner CIBC Innovation Banking. By the end of 2025, the company was citing more than $5 billion raised since inception across all raise types on its platform.

That cumulative figure reflects a business that has moved well beyond its early positioning. DealMaker’s issuer base now includes high-growth startups, consumer brands running Reg A+ campaigns as capital formation tools, and publicly traded companies raising supplemental capital directly from retail investors post-IPO. The Monogram Technologies story — which raised $13 million through DealMaker, then listed on Nasdaq, and was ultimately acquired by Zimmer Biomet for $177 million — became an illustration of the full-cycle thesis the company has been building toward. The raise funded the company; the listing provided liquidity; the acquisition returned capital to retail investors who got in at the private stage.

The Regulatory Bet Is Already Placed

CEO Rebecca Kacaba testified before the House Financial Services Committee in February 2025, specifically advocating for raising the Reg CF annual cap from $5 million and for increasing the Reg A+ ceiling. The INVEST Act, which passed the House in April 2026, includes provisions to double the Reg A+ cap to $150 million. A separate SEC petition to raise the Reg CF cap to $20 million remains pending.

Both reforms, if enacted, benefit DealMaker disproportionately relative to its peers. A $20 million Reg CF cap transforms the exemption from a community-funding tool into a meaningful growth capital pathway — one that attracts later-stage, more sophisticated issuers who currently have no reason to use Reg CF at a $5 million ceiling. Those issuers require a compliance-grade infrastructure layer and a capital markets execution partner, not a discovery marketplace. The same logic applies to a $150 million Reg A+ cap, which would allow DealMaker’s already-dominant Reg A+ position to compound into a far larger addressable market. DealMaker didn’t just position for regulatory reform — it testified for it, and built the platform to absorb the volume if and when it arrives.

The Moves That Signal Larger Ambitions

Several recent DealMaker developments are worth reading together rather than individually. The New York headquarters move put the company physically inside the financial ecosystem it wants to serve at larger scale. The acceptance of USDC stablecoin payments — one of the first platforms in the crowdfunding space to do so — opens the door to a broader, digitally-native investor base without requiring traditional payment rails. The launch of DealMaker Sports created a vertical built around fan ownership, a category that produces high investor engagement, strong brand alignment, and repeat participation across multiple raises.

The pattern is consistent: DealMaker is building distribution adjacencies that compound the value of its core infrastructure rather than competing with marketplace peers on deal discovery. Each vertical expansion — sports, consumer brands, public company retail raises — brings a new issuer type and a new investor community onto the same underlying platform. The infrastructure earns from all of them. The November 2025 financing round, relatively modest at $20 million for a company processing $500 million annually, reads less like a growth round and more like a strategic signal — a named institutional investor in Information Venture Partners, a deepened relationship with CIBC Innovation Banking, and a company that does not appear to need the capital as much as it needs the strategic alignment it brings.

What the Industry Isn’t Saying About This Yet

The crowdfunding category discussion in 2026 is still largely organized around Wefunder and StartEngine, with Republic occupying a separate lane as it builds out its tokenized private market products. DealMaker does not compete in that framing. It operates in a different strategic layer, one that sits beneath the platforms investors are familiar with and above the raw regulatory infrastructure of the JOBS Act exemptions. That positioning — deliberately invisible to investors, intentionally valuable to issuers — is exactly what makes it easy to overlook and potentially important to understand before the regulatory reforms that would most benefit it are resolved.

The $75 million Reg A+ ceiling has been the binding constraint on DealMaker’s largest issuers. A $150 million ceiling creates a category of raise that looks, from a capital formation perspective, less like crowdfunding and more like a small listed offering. DealMaker, with its compliance infrastructure, capital markets relationships, and issuer-centric model, is currently the best-positioned platform in the country to execute those raises at scale. That is not a narrative that has made it into the coverage yet.

What to Watch Next

- Senate Banking Committee action on the INVEST Act’s Reg A+ cap provisions. The House passed the doubling to $150 million; Senate markup will determine whether the number holds, gets amended, or gets stripped. DealMaker’s addressable market changes materially depending on where the cap lands.

- SEC response to the Reg CF cap petition (petition 4-889). A public comment window opening would signal the Commission is moving toward action. A $20 million Reg CF ceiling transforms the types of issuers DealMaker can serve under that exemption and extends its infrastructure advantage to a new issuer tier.

- DealMaker’s next strategic move. The New York headquarters, USDC payments, DealMaker Sports, and the $20 million financing round collectively suggest a company building toward something larger than white-label compliance services. Watch for a broker-dealer expansion, a move into direct secondary trading, or an acquisition in the investor-relations or capital markets execution space.

- Full-year 2026 Reg A+ volume figures. If the category rebounds from Q1’s soft quarter and DealMaker maintains its 50%-plus market share, the gap between its platform dominance and its public recognition becomes harder to overlook — particularly for institutional investors starting to price the retail private markets opportunity.

- Issuer pipeline through the IPO window. DealMaker’s model is most valuable to issuers who are on a path to a public listing — Reg A+ as a capital formation step before a Nasdaq or NYSE debut. As the IPO window reopens through H2 2026, watch for DealMaker-hosted raises in the pre-IPO pipeline and any announcements of named exchange relationships or listing partnerships.