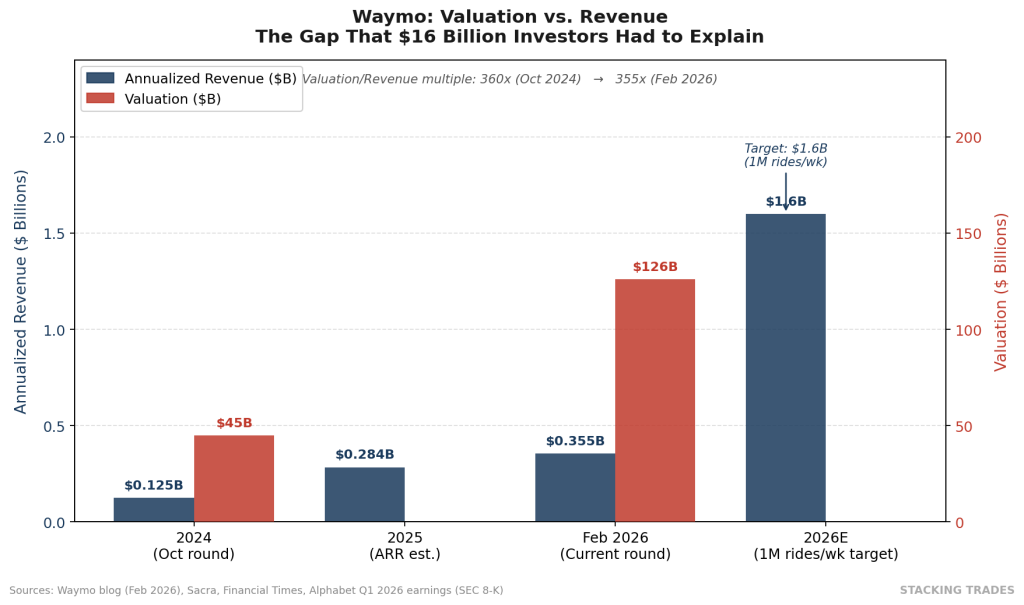

The number that should stop any institutional investor is not $126 billion. It is $355 million. That is Waymo’s annualized revenue run rate when it closed its latest funding round in February, according to Sacra and reporting by the Financial Times. The valuation is 355 times the revenue. For context, Uber — which operates in 70 countries, processes tens of billions in gross bookings annually, and has been public for six years — trades at roughly 4 times revenue. Someone has to explain the gap, and the explanation is not obvious.

The round itself was the largest single autonomous vehicle financing in history. Waymo raised $16 billion led by Dragoneer Investment Group, DST Global, and Sequoia Capital, with Alphabet anchoring approximately $13 billion of the total and maintaining its majority stake. The new investors joining the cap table include Kleiner Perkins and GV. That is not a group that routinely overpays for growth stories. Something has changed in how sophisticated capital is pricing autonomous vehicle businesses, and it is worth understanding exactly what.

What the Operational Data Actually Shows

Waymo is no longer a research program. As of Q1 2026, the company was delivering more than 500,000 fully autonomous rides per week across 10 U.S. metropolitan areas, a figure Alphabet CEO Sundar Pichai cited on the company’s Q1 2026 earnings call. That is roughly double the rate from mid-2025. In 2025 alone, Waymo completed 15 million rides, more than tripling the prior year’s volume, and has now surpassed 20 million lifetime paid trips on a fleet of 3,000 robotaxis. The company’s own target is 1 million rides per week by year-end, a figure co-CEO Tekedra Mawakana called an “inflection point” in a February Bloomberg television interview.

The revenue math that flows from those rides is relatively straightforward. Sacra estimates Waymo’s average fare at roughly $15 to $17 per ride, priced approximately 15% below Uber and Lyft in overlapping markets. At 500,000 weekly rides and $16 average fare, the annualized run rate sits around $416 million — slightly above the $355 million figure from February, consistent with the scaling trajectory. Management’s 1-million-rides-per-week target implies an annual revenue run rate approaching $1.6 billion if pricing holds. That is still a 79x revenue multiple on a $126 billion valuation. The math only closes if you believe 2026 is not the destination — it is the launch ramp.

“We are no longer proving a concept; we are scaling a commercial reality, laying the groundwork for ride-hailing operations in over 20 additional cities in 2026, including Tokyo and London.”<

— Tekedra Mawakana and Dmitri Dolgov, Co-CEOs, Waymo, February 2, 2026

Why the Valuation Gap Exists — and Why Investors Are Paying It

The standard objection to Waymo’s valuation is that no autonomous vehicle company has ever scaled profitably, and that $126 billion requires a leap of faith that the unit economics will hold across new cities, new geographies, and new regulatory environments. That objection is not wrong. But it misses the structural shift that the investor base is actually pricing: Waymo has moved from a technology demonstration into a recurring revenue business with no driver cost. Every ride a human Uber driver completes generates a fare that is immediately split — Uber takes roughly 25 to 30% and the driver takes the rest. Every ride a Waymo completes accrues almost entirely to the operator once the vehicle is depreciated. The gross margin profile of a mature autonomous fleet is structurally different from anything else in ride-hailing.

The competitive moat argument is also more durable than it looks from the outside. Physical AI at commercial scale is extraordinarily expensive to replicate. Waymo has logged more than 200 million fully autonomous miles on public roads — a training and safety data set that no new entrant can acquire quickly. Its safety record is verifiable: 90% fewer serious injury crashes than human drivers across 127 million rider-only miles through mid-2025, according to the company’s own published research, with independent Swiss Re analysis corroborating the property damage figures. Regulators in new cities move faster with a company that already has that record than they do with one that is still accumulating it.

The fleet cost problem is real, and worth taking seriously. Co-CEO Dmitri Dolgov has disclosed that the current Jaguar I-PACE platform costs roughly $175,000 per vehicle — approximately $75,000 for the car and $100,000 for the sensor stack and compute hardware. Getting from 500,000 to 1 million weekly rides on the current platform requires adding roughly 3,500 vehicles, which implies over $600 million in capital expenditure on vehicles alone before accounting for mapping, remote support, and per-city regulatory overhead. The next-generation Zeekr RT platform is expected to bring the total vehicle cost significantly lower, which is part of why investors are willing to fund the expansion now rather than wait for profitability at the current cost structure.

The Alphabet Relationship Is the Asset Investors Are Really Buying

Waymo’s majority owner contributed approximately $13 billion of the $16 billion raised — and that is not incidental to the valuation. Alphabet’s balance sheet backstops the expansion in ways no independent startup could replicate. The compute infrastructure, mapping data, and regulatory relationships Waymo inherits from Alphabet represent a structural cost advantage that does not appear directly in any revenue multiple. Alphabet CEO Sundar Pichai has said publicly that Waymo should begin contributing meaningfully to Alphabet’s bottom line by 2027. That is not a vague aspiration — it is guidance from a company that has already committed $13 billion to the outcome.

The Other Bets segment, which includes Waymo, reported $411 million in Q1 2026 revenue, down slightly from $450 million in the year-ago quarter. That sequential softness is not a Waymo signal; Other Bets includes several businesses at different stages. What matters is that Waymo’s ride volume is scaling while Alphabet’s broader AI platform — Google Cloud up 63% year-over-year, Gemini paid subscriptions reaching 350 million — provides the financial cushion for Waymo to build the fleet it needs without pressure to optimize unit economics prematurely.

The Questions the $126 Billion Doesn’t Answer

The investor case is coherent. That does not mean it is certain. Three questions remain genuinely open. First, the international expansion is unproven. London and Tokyo represent Waymo’s first right-hand-drive deployments, in regulatory environments that are more cautious and jurisdictionally complex than any U.S. city. The company is mapping both cities and has begun testing, but the timeline from mapping to paid commercial operations has varied widely in U.S. markets — from a few months in some cities to years in others. A stumble in London, which carries significant media visibility, would reprice the global expansion thesis quickly.

Second, the competitive landscape is no longer as clear as it was in 2023. Tesla’s robotaxi ambitions remain unverified at the scale Elon Musk has described, but the company controls its own vehicle manufacturing at volumes Waymo cannot match. Chinese autonomous vehicle competitors including Baidu Apollo and WeRide are operating in their domestic market under conditions that could produce cost structures significantly below Waymo’s current baseline. And Travis Kalanick’s new autonomous vehicle venture — backed by Uber — is an explicit bet that Waymo’s moat is narrower than its valuation implies. None of these are immediate threats. All of them are worth modeling over a five-year horizon.

Third, the profitability timeline is structurally dependent on the vehicle cost coming down faster than the expansion costs go up. The Zeekr RT platform, which is expected to lower per-vehicle costs substantially, is entering the fleet now. If the cost curve bends as projected while ride volume compounds toward 1 million per week, the unit economics argument becomes much easier to make by late 2026. If the Zeekr deployment lags, or if city-by-city expansion proves more expensive than the current model assumes, the 2027 bottom-line contribution Pichai referenced becomes harder to achieve.

The gap between $355 million in revenue and $126 billion in valuation is not evidence that the market is wrong. It is evidence that the market is pricing a very specific future — one in which autonomous ride-hailing scales to millions of weekly rides globally, with a margin profile that no human-driven competitor can replicate, under the financial shelter of one of the most profitable technology companies on the planet. That future is possible. The 2026 operational data will do more to confirm or challenge it than any analyst model.

What to Watch Next

- Waymo’s weekly ride volume trajectory through Q3 2026. The 1-million-rides-per-week target implies roughly doubling from the current 500,000 pace. Whether the ramp is linear, accelerating, or plateauing will be the single most important data point for validating the expansion thesis before any IPO filing.

- London commercial launch timing. Waymo has begun testing in the UK, but moving from mapping to paid rides in a right-hand-drive international market is unproven territory. The first revenue-generating trip in London is the threshold event that opens the global expansion narrative to institutional underwriting.

- Zeekr RT fleet deployment cost in practice. The new-generation platform is supposed to lower per-vehicle total cost substantially from the current $175,000 baseline. Actual procurement and deployment data — which will eventually surface through Alphabet filings — will determine whether the unit economics improvement is real or delayed.

- Any Waymo IPO or spin-off signal from Alphabet. Pichai’s 2027 bottom-line contribution comment may simply be an operating target — or it may be the precursor to a formal separation discussion. Watch for changes in how Alphabet reports Waymo financials, which would be a structural indicator of an independent path.

- Competing autonomous vehicle safety data. Tesla’s robotaxi launch, if it proceeds in 2026, will generate its own safety dataset for the first time. Any comparison between Waymo’s 200 million miles of autonomous data and Tesla’s emerging record will reset the safety-moat conversation among institutional investors.