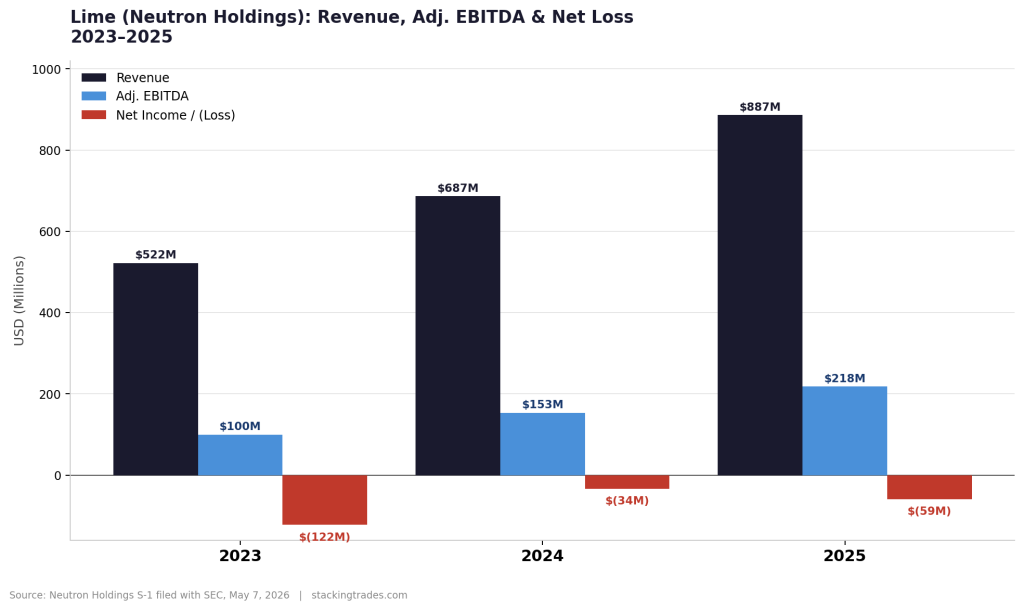

Lime filed its S-1 registration statement with the SEC on May 7, 2026, applying to list on the Nasdaq Global Select Market under the ticker LIME. Goldman Sachs, J.P. Morgan, and Jefferies are leading the deal. On the surface, the filing tells a credible growth story: revenue grew 29% to $886.7 million in 2025, adjusted EBITDA reached $218 million, and the company has generated positive free cash flow for three consecutive years. Lime operates in roughly 230 cities across 29 countries and holds approximately 48% dockless market share in the United States.

But buried in the risk factors is a disclosure that makes this one of the more unusual IPO bids in recent memory. The company warned investors that it does not have “sufficient liquidity” to repay its lenders, and that “substantial doubt exists” about its ability to continue as a going concern. The IPO is not optional growth capital. It is, by the company’s own admission, a survival mechanism.

The Debt Wall Is the Whole Story

Lime reported approximately $1 billion in current liabilities at the end of March 2026, with roughly $846 million due within the next 12 months. About $675.8 million of that is owed by the end of December 2026. The company had $261 million in cash on hand as of March 31. That gap is not something a normal operating cadence closes.

The debt originated in a different rate environment. Lime, like many of its sharing-economy peers, borrowed heavily during the zero-interest-rate years and is now facing maturities in a market that looks nothing like the one those loans were priced into. It is a situation that is becoming increasingly common across corporate credit. According to PitchBook LCD, around $85 billion in loan maturities will fall due between 2026 and 2029, putting borrowers under compounding refinancing pressure.

“The company needs this IPO to address the 2026 maturities, and that dependence is itself a risk. But if they have a refinancing path and are using the IPO to de-lever instead, that’s constructive.”<

— Sebastian Kian, Senior Private Credit Research Analyst, PitchBook LCD, May 2026

That framing matters for how institutional allocators think about the deal. If IPO proceeds retire the debt in full and the company emerges with a clean balance sheet, the going-concern warning becomes a historical footnote. If pricing comes in too thin to cover the obligation, Lime will need parallel refinancing, which means the underwriters hold more leverage than they typically would in a growth IPO.

Growth Metrics That Would Otherwise Be Compelling

Strip out the balance sheet and Lime’s operational trajectory is genuinely strong. Revenue has grown from $522 million in 2023 to $887 million in 2025, and adjusted EBITDA has nearly doubled over the same period, from $100 million to $218 million. The company turned operating profitable in 2024, posting $47 million in operating income, and held that ground with $70 million in 2025 despite wider GAAP net losses driven by interest expense on that debt pile.

The revenue per vehicle per day figure of $7.47 in 2025 indicates the fleet is being utilized efficiently, and the company’s 116% operational fleet retention rate suggests it is not burning through hardware at a pace that erodes unit economics. These are numbers that, in a different capital structure, would support a straightforward growth story.

The problem is that the Q1 2026 data complicates the picture heading into the roadshow. Lime recorded a net loss of $61.3 million in the three months ended March 31, 2026, slightly worse than the $56 million loss in Q1 2025. Free cash flow went negative by $79 million in the quarter. The company attributes this to seasonal patterns and first-quarter fleet expansion spending, which is consistent with how the business works. But arriving at a roadshow with a fresh negative quarter while simultaneously disclosing a going-concern risk is not an easy ask for institutional buyers.

Uber Is Both a Strength and a Single Point of Failure

Uber led Lime’s $170 million financing round in 2020, absorbing its Jump e-bike subsidiary in the process. The two companies have operated under a mutually exclusive integration since then: Lime vehicles appear as a ride option inside the Uber app across nearly all of Lime’s shared markets, giving Lime direct access to Uber’s global user base without paying conventional customer acquisition costs.

That partnership accounted for approximately 14.3% of Lime’s total revenue in 2025 and 14.0% in Q1 2026. The current agreement was renewed last May and runs through 2028. Lime acknowledges in its S-1 that it is subject to Uber’s strategic decisions in a way that few companies in its position would be comfortable disclosing so plainly. If Uber deepens its investment in autonomous vehicles or deprioritizes the Lime integration, roughly one-seventh of Lime’s revenue becomes structurally uncertain. That is not a theoretical risk for the 2026 market; Uber has been publicly accelerating its AV partnerships and rideshare automation investments throughout this cycle.

The flip side is that the Uber relationship is also what makes Lime defensible as a category. The 2026 IPO window has been dominated by AI and deep-tech stories, and Lime is the first meaningful consumer mobility company to test institutional appetite for a different kind of growth narrative. The Uber distribution gives that narrative credibility that a pure standalone scooter operator could not credibly claim.

What Pricing at $2 Billion Actually Means

Sources cited in reporting from TechCrunch and MLQ put Lime’s target valuation at approximately $2 billion. At $886 million in 2025 revenue, that implies a price-to-sales multiple of roughly 2.3x — modest by 2021 standards, and arguably appropriate for a business with a going-concern disclosure and a compressed roadshow timeline. The comparison that matters is not to AI infrastructure companies or even to software platforms. It is to Bird, Lime’s most direct competitor, which went public via SPAC in 2021 and subsequently filed for bankruptcy. That outcome has permanently attached a skepticism premium to the category.

Lime’s bulls would argue the comparison is unfair. Bird competed in an unsustainable subsidy war and never developed the operational discipline or unit economics Lime has demonstrated over the past three years. That case is plausible. But institutional memory around micromobility’s SPAC-era performance is not something underwriters can simply argue away at a roadshow, particularly when the company is simultaneously disclosing that it needs the offering to stay solvent.

The more useful frame for investors is not whether Lime deserves a premium multiple. It is whether the company can raise enough at any multiple to retire the debt wall, stabilize the balance sheet, and then trade on operating fundamentals. At $2 billion, with a typical 15–20% float, the primary raise would be in the $300–400 million range — well short of covering $846 million in near-term maturities. That math requires either a significantly larger float, debt-for-equity exchanges negotiated with existing creditors, or parallel refinancing arranged concurrently with the offering.

The IPO Market Question Lime Is Really Testing

The timing is not incidental. Lime is filing directly into a window shaped by SpaceX’s forthcoming mega-listing, which is expected to dominate institutional allocation bandwidth for consumer and growth equity through much of the summer. SpaceX’s offering alone is expected to test whether the public market infrastructure can absorb a deal at a scale it has never seen before. Lime arrives as a fundamentally different kind of bet — a cash-flow-positive but balance-sheet-distressed business asking public investors to take a position that private investors, over nine years and $1.5 billion in funding, never quite resolved.

That is not necessarily disqualifying. Distressed-for-control-type narratives have found institutional buyers before, and Lime’s operating leverage story is real. But the question this offering answers for the broader market is narrower than whether Lime is a good business. It is whether public investors in 2026 will fund a going-concern warning at a growth premium, in a category with a recent bankruptcy analog, while the biggest IPO in history is staged to absorb the room’s attention two weeks later.

The answer to that question will tell you something material about where the IPO market actually is, as distinct from where the league tables say it should be.

What to Watch Next

- The amended S-1 with a pricing range and share count. The current filing contains no dollar figures for the offering price or proceeds. The amendment will be the first hard data point on whether the raise is sized to cover the debt wall or falls short and requires parallel refinancing.

- Uber’s Q2 2026 earnings commentary on micromobility and autonomous vehicle investment. Any language suggesting Uber is accelerating AV-first urban transport would directly reprice the durability of Lime’s 14% revenue dependency.

- Roadshow demand signals from Goldman and J.P. Morgan. Given the going-concern disclosure, institutional allocations will be unusually transparent about risk tolerance. Watch for any book-build reporting that indicates order quality, not just volume.

- Creditor behavior ahead of the December 2026 maturity. If convertible note holders begin negotiating debt-for-equity exchanges in parallel with the roadshow, it would indicate the IPO raise is not expected to fully cover the obligation and that the capital structure needs a concurrent fix.

- First-day trading relative to the offering price. Lime’s opening print will be the clearest signal of whether public investors priced in the balance sheet risk or bid as though it was already resolved.