{kind=link}

The number that matters most from the Cerebras IPO is not $185 — the price at which shares were sold — nor $350, where they opened, nor $311.07, where they closed on May 14. The number that matters is 86. That is the percentage of 2025 revenue that came from two entities in the United Arab Emirates. Everything else about this offering flows from that fact.

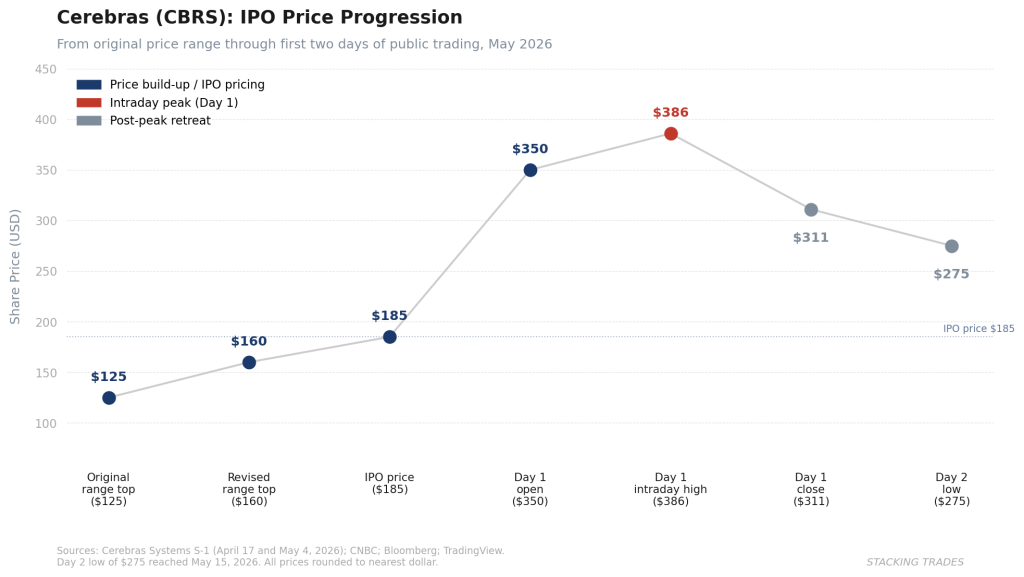

Cerebras Systems raised $5.55 billion on Nasdaq on May 14, pricing 30 million Class A shares at $185 each — more than double the original marketed range of $115 to $125 — after an order book that closed roughly 20 times oversubscribed. The stock opened at $350, hit an intraday high of $386.34 that briefly triggered a trading halt, and closed the first session up 68% at $311.07. By the following day it had given back more than 10%. It is the largest U.S. tech IPO since Uber in 2019. It is also one of the most concentrated customer bases ever presented to public market investors in a semiconductor offering.

What the S-1 Actually Says

Cerebras filed its S-1 registration statement on April 17, 2026, and amended terms on May 4. The prospectus discloses $510 million in 2025 revenue, up 76% from $290 million in 2024. Revenue has grown from $25 million in 2022 — a compelling trajectory by any measure.

The profitability picture, however, requires a close reading. Cerebras reported net income of $87.9 million in 2025 on a GAAP basis, swinging from a $484.8 million net loss in 2024. The swing is real, but it was driven primarily by a $363.3 million non-cash gain tied to extinguishing a forward-contract liability connected to G42’s original investment. Strip that out and the company posted an operating loss of approximately $146 million. Gross margins improved materially — from roughly 12% in 2022 to the low 40s by 2025 — and the direction of travel is genuine. But the company that went public on May 14 is not yet operationally profitable, and investors who read only the headline net income figure bought a different story than the one in the footnotes.

The customer concentration is worse than the summary disclosure suggests. G42, the Abu Dhabi AI conglomerate that once accounted for 85% of Cerebras revenue in 2024, has been reduced to 24% of 2025 revenue — a figure the roadshow presented as evidence of diversification. But the Mohamed bin Zayed University of Artificial Intelligence, which the prospectus identifies explicitly as a G42 related party, accounted for 62% of 2025 revenue. Together the two UAE-linked entities represented 86% of revenue. MBZUAI alone accounted for 77.9% of accounts receivable as of December 31, 2025. The S-1 states directly: “The loss of, any substantial reduction in sales to, or the default on payments by, any of our significant customers would harm our business, financial condition, results of operations, and prospects.”

What the roadshow called customer diversification was, in substance, a revenue reallocation between two connected entities in the same country. Public investors absorbed that risk at a valuation that briefly touched $100 billion on a fully diluted basis.

“There’s some whales out there, there’s some really big customers. That is one of the characteristics of this market.”<

— Andrew Feldman, CEO, Cerebras Systems, CNBC interview, May 14, 2026

The OpenAI Relationship Is the Bull Case — and the Complication

The deal that changed the Cerebras story enough to bring the IPO back from a 2024 withdrawal is the $20 billion Master Relationship Agreement with OpenAI, covering 750 megawatts of AI inference compute capacity with an option to expand to 2 gigawatts by 2030. That agreement, signed in January 2026, is the single most important commercial development in Cerebras’s history. It converts the company from a sovereign AI supplier for the UAE into something that at least resembles a hyperscaler-grade infrastructure business.

The structure of the arrangement, though, carries its own complexity. OpenAI advanced Cerebras a $1 billion working capital loan in January at 6% annual interest, secured by warrants to purchase up to 33.4 million Cerebras shares at a near-zero exercise price. Amazon Web Services holds similar warrants as part of a March 2026 term sheet that would make AWS the first hyperscaler to deploy Cerebras hardware in its own data centers. At the $350 opening price, the OpenAI warrants alone would be worth approximately $11.7 billion if fully vested — a stake that gives OpenAI substantial economic interest in Cerebras’s public market performance while simultaneously being its largest commercial customer. That relationship is not arms-length, and investors in CBRS are underwriting it whether they know it or not.

The backlog figure is genuinely unusual. Total remaining performance obligations — contracted revenue not yet recognized — stood at $24.6 billion against $510 million in trailing revenue, a ratio of roughly 48 times. D.A. Davidson analyst Gil Luria pegged a fair value near the backlog level and suggested a target around $115 per share, well below the IPO price. Renaissance Capital flagged the valuation as “quite high even out to 2028.” Neither view stopped the book from going 20 times covered.

The Arm Approach Nobody Expected

The morning of May 13, the day before trading began, Bloomberg reported that Arm Holdings and its parent SoftBank had made a preliminary acquisition approach to Cerebras in the weeks prior. Cerebras rejected it. Representatives for all three companies declined to comment.

The approach is significant in both directions. For Arm and SoftBank, it signals strategic ambition beyond the chip architecture licensing model — a push toward owning full-stack AI silicon capability at a moment when the company was shaping its own public market pitch. For Cerebras, the decision to reject the approach and proceed to public markets at a valuation that briefly cleared $100 billion on a fully diluted basis is a clear statement about how the company’s leadership assesses its independence value versus its acquisition value. The $350 opening price validated that judgment in real time, at least on the first day.

As we wrote in April when the S-1 was first filed, the central question for Cerebras was never whether the wafer-scale technology works. It is whether inference-specialized silicon can hold a durable position against Nvidia’s platform — CUDA, networking, software, and enterprise distribution — plus AMD’s renewed data-center push and Google’s and Amazon’s custom ASIC programs, all in a market where Nvidia still commands an estimated 81% share of AI accelerator spend.

What the First Day Taught Institutional Investors

The 68% first-day pop followed by a 10%-plus decline on day two is a familiar pattern for high-profile AI offerings — strong institutional demand at pricing, retail enthusiasm at the open, and then a valuation reality check once the lock-up calendar and customer concentration get priced properly. The stock traded as low as $275 during the first two days, giving back more than a third of the first-day closing gain before stabilizing.

The more useful signal for the investment case is the backlog-to-revenue ratio and what it requires. For CBRS to justify even its IPO price of $185 at a reasonable forward multiple, Cerebras needs to convert a substantial portion of that $24.6 billion in remaining performance obligations into recognized revenue on an accelerated timeline, do so with improving gross margins, and reduce its operating losses while simultaneously funding the infrastructure buildout that the OpenAI and AWS agreements require. Each of those variables is subject to the pace of OpenAI and AWS deployment decisions — which are in turn subject to their own capital allocation priorities and competing infrastructure commitments.

The hyperscaler capex context matters here. As we covered in our analysis of the $690 billion infrastructure cycle, the 2026 buildout is running at historically unprecedented levels. That is the demand tailwind Cerebras is riding. It is also the environment in which Nvidia, AMD, and custom ASIC programs from Google, Amazon, and Microsoft are all competing for the same infrastructure dollars. The tailwind does not guarantee Cerebras a share of it.

For the broader IPO pipeline, the Cerebras debut serves the function we anticipated when SpaceX’s confidential filing dropped in April: it tests public market appetite for AI infrastructure stories at private-market valuations before the much larger SpaceX and OpenAI offerings arrive. The result — massive demand at pricing, a 68% first-day pop, then immediate pressure on valuation — suggests the market has appetite for AI chip stories but not unlimited patience for the concentration risk hiding inside them. That is useful data for anyone pricing the next one.

What to Watch Next

- Cerebras’s first earnings report as a public company. The S-1 disclosed trailing revenue and a backlog; the quarterly print will show whether OpenAI and AWS volume is converting into recognized revenue on the timeline the prospectus implies. Any revenue shortfall against the backlog pace will reprice the stock materially.

- OpenAI’s deployment disclosures. The $20 billion MRA commits OpenAI to purchase capacity, but delivery is staged and the terms allow for adjustment. Watch any OpenAI commentary on compute infrastructure for signals about whether the Cerebras relationship is expanding or being managed conservatively.

- AWS Bedrock integration timeline. The March term sheet put AWS in position to become the first hyperscaler deploying Cerebras chips in its own data centers. A formal launch date and any disclosed pricing would provide the first indication of whether the relationship generates commercial volume beyond the OpenAI account.

- Customer concentration metrics in subsequent filings. The 86% UAE revenue figure is the single variable that most constrains the institutional investor base willing to hold CBRS. Any quarterly filing showing Western enterprise revenue growing as a share of the total is the clearest path to multiple expansion.

- Lock-up expiration dynamics. The 180-day lock-up places insider and early investor selling pressure in the November 2026 window. Fidelity controls approximately 11% of shares and Benchmark holds approximately 9%. How the stock absorbs that potential supply will be the second-most-important pricing event after the first earnings report.