.jpg){kind=link}

The four companies that now spend more on artificial intelligence infrastructure than most nations spend on defense all reported first-quarter results on the same evening this week, handing investors a rare side-by-side test of a thesis that has driven equity markets for two years: that the hyperscaler capex binge will pay off in durable cloud revenue growth. Three of them passed. One of them passed and still fell 8%.

The divergence tells you more about where we are in this cycle than the top-line numbers do.

What the Numbers Actually Said

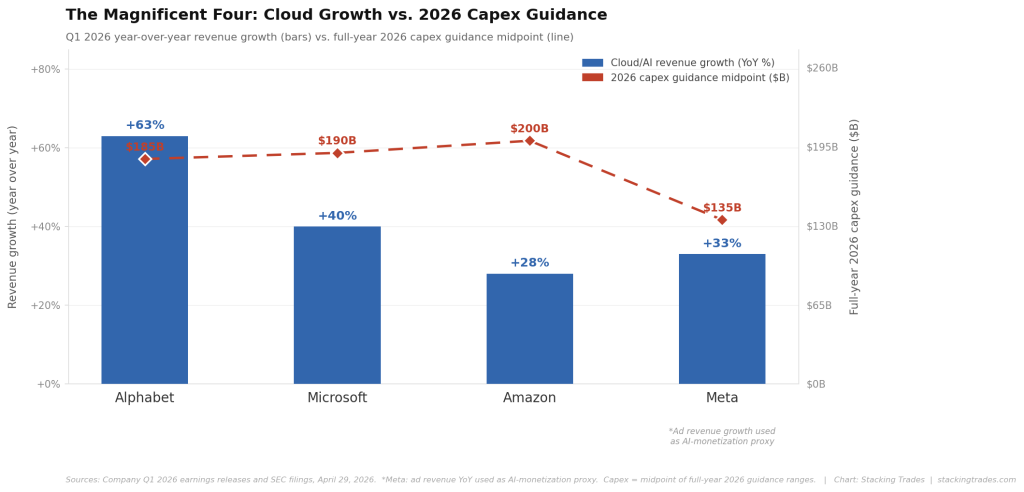

Microsoft’s fiscal third quarter came in at $82.9 billion in revenue, up 18% year over year, with Azure growing 40% — above the 37–38% guidance range management had set three months earlier. The commercial remaining performance obligation, the most important demand indicator in the entire report, rose 99% to $627 billion. CEO Satya Nadella put the AI business run rate at $37 billion annualized, up 123% from the prior year. CFO Amy Hood guided fourth-quarter capex above $40 billion, citing roughly $5 billion from higher component pricing. Total fiscal 2026 spend is now expected to reach $190 billion. The stock fell 5% Thursday as investors processed what $190 billion in capex does to near-term free cash flow.

Alphabet’s filing was the cleanest print of the four. Revenue reached $109.9 billion, up 22%, with Google Cloud accelerating to 63% growth and $20 billion in revenue — more than double its pace from a year ago. The Cloud backlog nearly doubled quarter over quarter to $462 billion. CFO Anat Ashkenazi said the company expects just over half of that backlog to convert to revenue in the next 24 months and flagged that 2027 capex will increase significantly from this year’s revised $180–190 billion range. Alphabet shares rose 7% in after-hours trading. That reaction was the market’s verdict on what credible AI monetization evidence looks like.

Amazon reported AWS growth of 28% to $37.6 billion — the segment’s fastest pace in 15 quarters — alongside a chips business that topped a $20 billion annualized run rate growing at triple-digit percentages year over year. CEO Andy Jassy disclosed in the earnings release that Amazon processed more tokens through its Bedrock platform in Q1 2026 than in all prior years combined. Capital expenditures reached $44.2 billion in the quarter, driving trailing twelve-month free cash flow down to $1.2 billion from $25.9 billion a year ago. The stock fell roughly 3% after hours despite the beat, entirely on the capex line.

Meta posted revenue of $56.3 billion, up 33%, the fastest growth the company has seen since 2021. Net income rose 61% to $26.8 billion, though the headline EPS figure was inflated by an $8.03 billion tax benefit. Strip that out and the quarter was still a strong beat. None of it mattered to the market. Meta’s earnings release disclosed full-year capex guidance raised to $125–145 billion from the prior range of $115–135 billion. Meta said the revision “reflects our expectations for higher component pricing this year and, to a lesser extent, additional data center costs to support future year capacity.” The stock fell 8% by Thursday morning.

The Capex Divergence Is the Story

All four companies raised capital expenditure guidance in the same week. Only Alphabet got rewarded for it. The difference is not the size of the raise — Meta’s $10 billion upward revision is smaller in absolute terms than Alphabet’s. The difference is what investors can see on the other side of the spending.

Google Cloud’s backlog nearly doubling quarter over quarter to $462 billion is a contracted demand signal. It says the spending is being pulled forward by real customers committing real dollars, and that more than half of it converts to revenue within two years. Meta’s capex raise came with Zuckerberg describing the company’s AI-spending framework to an analyst as “a very technical question.” That language, paired with a second consecutive upward revision in two quarters, told the market something specific: the return on investment timeline remains undefined.

“Our AI investments and full stack approach are lighting up every part of the business. Search had a strong quarter with AI experiences driving usage, queries at an all time high, and 19% revenue growth. Google Cloud revenues grew 63% with backlog nearly doubling quarter on quarter to over $460 billion.”<

— Sundar Pichai, CEO, Alphabet, April 29, 2026

Microsoft sits in an interesting middle position. Azure’s 40% growth beat guidance, the AI business run rate is real and growing fast, but the $190 billion full-year capex commitment — $5 billion of which is explicitly attributed to higher component pricing — compresses near-term cash generation in ways the market is still trying to price. Hood’s comment that Microsoft expects to remain capacity constrained through 2026 is bullish for demand but does not help the immediate free cash flow picture. As we noted ahead of this print, the key variables were Azure growth direction and the sequential capex change. Azure delivered. The capex variable resolved in the direction that makes the short-term cash flow math harder.

Sources: Company Q1 2026 earnings releases, April 29, 2026. Capex shown as percentage of trailing twelve months revenue.

What the AWS Chip Disclosure Actually Means

The most underreported number from the entire earnings week belongs to Amazon. Jassy disclosed that if Amazon’s custom silicon business — comprising Graviton, Trainium, and Nitro — were sold externally rather than consumed internally, its annualized revenue run rate would be $50 billion. The actual reported run rate, counting only external third-party revenue, topped $20 billion growing at triple digits year over year.

That $50 billion figure is not a projection. It is a disclosure of the shadow value of AWS’s vertically integrated silicon strategy, and it changes how investors should think about AWS margins over the next three years. Every token processed on Trainium rather than a third-party GPU is a unit of compute whose cost structure Amazon controls end to end. The Bedrock data point — more tokens processed in Q1 2026 than in all prior years combined, with customer spend up 170% quarter over quarter — confirms that the inference workloads are arriving and arriving on Amazon’s own infrastructure. This has direct implications for the hyperscaler capex thesis that has dominated the private infrastructure investment landscape since late 2024.

The conventional read on AI capex has been that it flows overwhelmingly to Nvidia. That is still broadly true in the current period. But Amazon’s disclosure this week is the clearest public-market data point yet that the largest cloud provider is building an increasingly sovereign silicon stack. The implication for Nvidia’s pricing power over its three largest customers is not immediate, but it is not speculative either.

The Real Test Is in the Revenue Conversion

The aggregate capex commitment from these four companies now exceeds $700 billion for 2026 alone. The market’s patience with that number depends entirely on whether the revenue conversion continues to accelerate. Google Cloud’s quarter — 63% growth, $462 billion backlog, operating margin expanding from 17.8% to 32.9% year over year — is the most concrete evidence available that the conversion is happening. AWS’s reacceleration to 28%, its fastest growth in nearly four years, is a close second.

Meta is the outlier in the set because its AI spending is largely internal — improving ad targeting, Reels ranking, and the inference infrastructure underlying its own consumer products — rather than external cloud revenue that can be tracked in a backlog figure. The advertising numbers confirm the investment is producing results: revenue grew 33%, ad impressions rose 19% year over year, and average price per ad climbed 12%. But investors cannot see the AI-driven component of those results in isolation, which means every capex raise forces the same argument about faith and time horizon.

The market’s willingness to fund that argument depends on what the other three companies keep demonstrating. As long as Azure, AWS, and Google Cloud are printing accelerating growth alongside their spending raises, Meta’s capex story remains defensible as part of the same infrastructure cycle. If cloud growth decelerates in Q2 — the next major test comes when all four report again in late July — the market’s tolerance for undefined ROI timelines will shrink quickly.

What This Means for Private Market Positioning

For investors with exposure to private AI infrastructure funds, power generation, or data center operators, this week’s prints confirm the demand trajectory without resolving the supply chain cost question. Meta’s explicit attribution of its capex raise to “higher component pricing” — an explanation Microsoft echoed with Nadella’s $25 billion component-cost callout — is a direct signal that GPU and memory pricing is not normalizing at the pace the bull case requires.

The investors best positioned in this environment are those who own the component suppliers and the power infrastructure, not just the applications layer. Caterpillar, whose construction equipment is used in data center buildouts, beat earnings estimates this week with a record backlog and raised its full-year revenue outlook — a quiet confirmation that the physical buildout has accelerating momentum regardless of which hyperscaler is spending the money. The agentic AI monetization thesis depends on this infrastructure being in place. This week’s results suggest it will be.

What to Watch Next

- Google Cloud’s Q2 backlog conversion rate. Ashkenazi committed to converting just over 50% of the $462 billion backlog within 24 months. Any quarterly disclosure that shows conversion pace slowing would be the first crack in the bull case for AI infrastructure investment.

- Meta’s Q2 revenue per user trajectory. The company guided Q2 revenue of $58–61 billion. Whether AI-driven ad targeting improvements show up in average revenue per person — the cleanest metric for whether internal AI spending is generating returns — will be the most watched number in the next print.

- Nvidia’s Q1 fiscal 2027 earnings, expected late May. With hyperscaler component pricing described as a headwind by both Meta and Microsoft, Nvidia’s commentary on pricing, lead times, and next-generation GPU allocation will either validate or complicate the capex trajectory these four companies just outlined.

- AWS free cash flow recovery timeline. Amazon’s trailing twelve-month free cash flow fell to $1.2 billion from $25.9 billion as the capex ramp consumed the company’s near-term cash generation. When and at what revenue level AWS free cash flow reaccelerates is the central question for Amazon bulls heading into the second half of 2026.

- Microsoft’s Build developer conference in May. The venue for Copilot monetization updates and any new enterprise AI pricing structures. Any new tier or agent-based pricing announcement would provide the first quantified look at whether Microsoft’s $37 billion AI run rate can compound at the pace the capex bill requires.