The numbers were supposed to confirm a structural shift. Instead, they confirmed a competition problem.

Investment crowdfunding posted its worst quarter in two years to start 2026, with Reg CF capital falling 29% year over year and Reg A dropping 45%, according to Kingscrowd’s Q1 2026 update. In raw terms, Reg CF raised $72.4 million in Q1 2026, down from $101.9 million in the same period a year earlier. The Reg A decline was sharper — a category that had been on a multiyear run powered by a handful of large, consumer-facing campaigns suddenly lost nearly half its quarterly volume.

Both declines arrived at an awkward moment. Congress passed the INVEST Act in April. The SEC has a pending petition to raise the Reg CF cap from $5 million to $20 million. The regulatory environment, at least on paper, has never been more favorable. The market, at least in Q1, did not care.

The Explanation Is Not a Recession

Crowdfunding’s supporters will point to the winter seasonality argument, and they are not wrong to. February 2026 Reg CF totals came in at roughly $21.95 million, a soft month consistent with how the industry has historically opened the year. But Q1 2025 had the same seasonal pattern and produced $30 million more in Reg CF alone. The gap is not explained by weather.

The more honest explanation is that the category is losing the attention war. Kingscrowd’s own 2025 annual report identified the structural shift plainly: investment crowdfunding is no longer competing primarily with other crowdfunding deals. It is competing with a fast-growing universe of retail-accessible private market products — tokenized funds, BDC feeder vehicles, pre-IPO ETFs, and prediction markets — that are increasingly easier to buy, explain, and distribute through mainstream brokerage channels. The Q1 2026 data suggests that competition is landing.

The AI boom compounded it. Retail investors with genuine risk appetite who might have put $500 into a Reg CF startup campaign in 2024 now have a direct path into AI-adjacent positions through public equities, thematic ETFs, and options. The cognitive and financial bandwidth that crowdfunding platforms have historically captured at the margin is under direct pressure from instruments that clear through existing brokerage accounts with no new platform registration required.

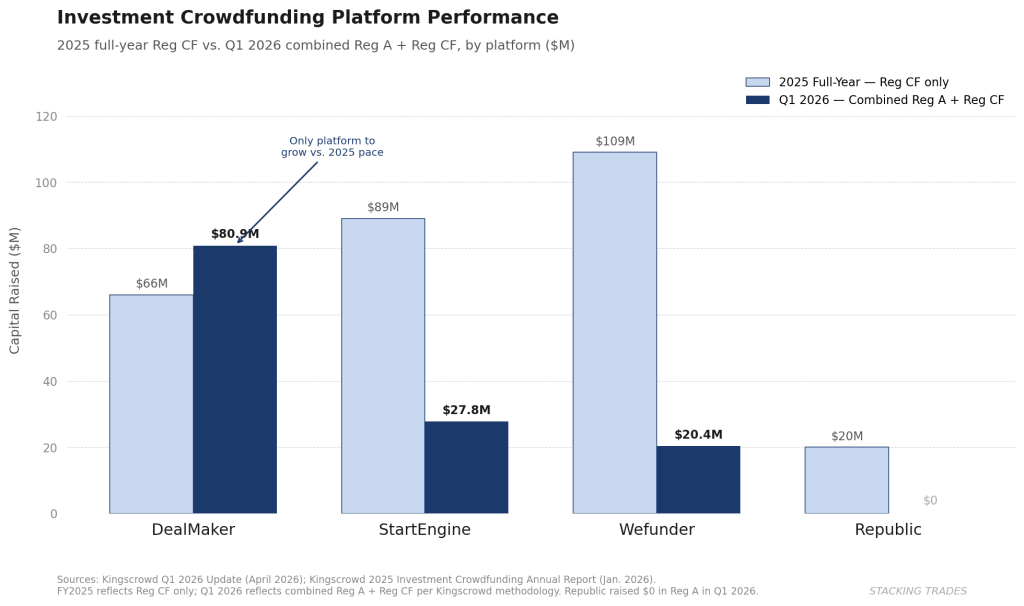

DealMaker Wins a Down Market

Inside the sector-level decline, the platform-level data tells a different story — and it is the more important one for investors tracking where this market is actually going.

DealMaker captured the largest combined Reg A and Reg CF share in Q1 at roughly $80.9 million, followed by StartEngine at $27.8 million and Wefunder at $20.4 million. Republic raised no Reg A funds during the quarter. Those rankings are a significant reversal from the 2025 full-year Reg CF standings, where Wefunder led at $109 million, StartEngine came second at $89 million, and DealMaker — then primarily a white-label infrastructure provider — trailed at $66 million in Reg CF alone.

What changed is that DealMaker’s Reg A volume is now doing the work. The platform dominated Reg A+ in 2025 with $292 million raised, accounting for more than 50% of all Reg A+ capital that year. That infrastructure advantage — DealMaker serves as a capital markets execution layer for larger, later-stage issuers rather than a deal discovery destination for retail investors — held up in a quarter when smaller, earlier-stage Reg CF campaigns contracted sharply. When retail investor attention cools, the platforms serving issuers who treat fundraising like a real capital markets transaction outperform the ones serving issuers who treat it like a marketing campaign.

That distinction matters more as the market consolidates. As we noted in our earlier analysis of platform consolidation dynamics, DealMaker’s New York headquarters move and USDC payment integration in 2025 signaled an ambition beyond white-label compliance. Q1 2026 is the first hard data point that the ambition is converting into market share.

Wefunder’s Open Model Is Being Tested

Wefunder led Reg CF in Q1 at $20.4 million — still first in that specific exemption, but down significantly from the $109 million it raised across all of 2025. The open-platform model that made Wefunder the dominant community-round destination has a known vulnerability in soft markets: the platform’s breadth works against it when retail investor attention is selective. More listings do not help if fewer investors are looking.

StartEngine’s Q1 positioning is more complicated. The platform raised $27.8 million in combined Reg A and Reg CF — better than Wefunder in the combined measure, consistent with its diversification into secondary trading and the Vinovest acquisition in March. But the comparison against its own 2025 Reg CF performance of $89 million annually suggests the platform is also operating in a lower-volume environment, even as its product surface has expanded. Secondary market liquidity on StartEngine remains thin. As we covered in our StartEngine build-out analysis in April, over 400 issuers are enrolled on StartEngine Secondary but active secondary market quotes remain a fraction of that number. That liquidity gap continues to constrain the narrative.

The Cap Reform Question Gets More Urgent

The Q1 data sharpens the stakes around the SEC petition to raise the Reg CF offering cap from $5 million to $20 million. As we wrote when the petition was first filed, the cap is the binding constraint that keeps later-stage, higher-quality issuers from using Reg CF as a serious capital markets tool. Those issuers — the kind that might attract genuine retail investor attention in a competitive environment — have little reason to run a Reg CF campaign when $5 million is the ceiling and Reg A or a private round can clear more without the per-investor disclosure overhead.

A Q1 decline of 29% makes that calculus more visible. The platforms that would most benefit from a cap increase — those with compliance infrastructure and investor depth to handle larger, more complex raises — are already outperforming. The platforms most dependent on volume and community to drive results are the ones showing the steepest softness. If the SEC moves on the petition, the competitive dynamics that produced Q1’s rankings are likely to accelerate, not reverse.

Kingscrowd called Q1 a possible “reset quarter” and described the combined market as remaining “constructive.” That framing is defensible if spring and summer volume rebounds materially. The 2025 full-year Reg CF total of $378 million was built on a smaller number of higher-quality raises concentrated in a shorter window — the category can produce strong annual numbers from a weak first quarter if the right campaigns come to market.

But the structural pressure is real and it is not going away. The competition for retail investor attention will not ease as Cerebras trades publicly, SpaceX’s S-1 drops, and the AI IPO pipeline fills the calendar through Q3. Crowdfunding platforms are building against a tide of new, increasingly accessible alternatives for exactly the investor they have always depended on — the engaged, risk-tolerant retail participant who wants early exposure to companies that have not yet gone public. That investor now has more options than at any point in the category’s history, and Q1 2026 is the first quarter where the data shows the cost of that competition clearly.

What to Watch Next

- Q2 Reg CF volume as the true seasonality test. Spring is the industry’s historically strongest period; if Q2 does not show a meaningful rebound from Q1’s $72.4 million, the reset-quarter thesis fails and a structural decline becomes harder to dismiss.

- SEC response to petition 4-889 on the Reg CF cap. Any signal that the Commission is moving toward a public comment window would reset the addressable market for platforms with the infrastructure to serve larger issuers — and compress the runway for platforms that cannot.

- DealMaker’s next strategic move. The Q1 data confirms market share leadership in combined volume. Watch for a formal broker-dealer buildout, a move into direct secondary trading, or an acquisition that would signal DealMaker is building toward a capital markets platform, not just a compliance layer.

- Wefunder’s issuer pipeline quality. In a market that is rewarding fewer, higher-quality raises over volume, Wefunder’s open-platform model requires issuers with real traction to hold its position. Watch whether the platform begins curating more aggressively or maintains open access and accepts lower average raise sizes.

- Republic’s Reg A return. The platform raised nothing under Reg A in Q1. Whether that reflects a strategic pivot toward its Mirror Token and institutional products or a temporary gap in its issuer pipeline will become clear by mid-year.