{kind=link}

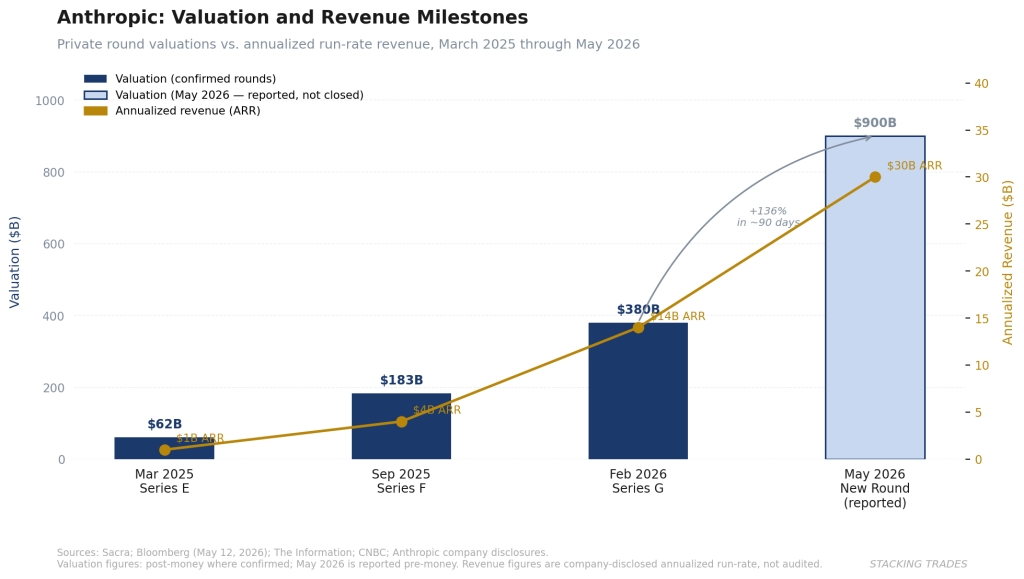

Three months ago, Anthropic closed a $30 billion funding round at a $380 billion post-money valuation and described it as the second-largest private tech financing in history. That round has since been lapped — by Anthropic itself.

The company is now in early talks to raise at least another $30 billion, this time at a pre-money valuation exceeding $900 billion. Dragoneer, Greenoaks, Sequoia Capital, and Altimeter Capital have agreed to co-lead the round, with each expected to invest $2 billion or more, per The Information. The round is expected to close by the end of May. No term sheet has been signed. The deal, if it closes at the reported figure, would give Anthropic a higher headline valuation than OpenAI’s $852 billion mark from its March financing — a competitive fact that is not incidental to the timing.

The velocity of the move is the story. At the February Series G close, Anthropic’s annualized run-rate revenue was $14 billion. On April 7, the company said that figure had crossed $30 billion — a number it described, in Dario Amodei’s public comments, as reflecting roughly 80-fold growth over the prior year. The valuation went from $380 billion to $900 billion in approximately 90 days. One of those numbers reflects what happened. The other reflects a bet on what happens next.

What Actually Moved

The revenue acceleration is real. Anthropic ended 2025 with approximately $9 billion in annualized revenue. By the February 2026 Series G close it was at $14 billion. By April 7, it had crossed $30 billion. The product driving the surge is Claude Code, the AI coding assistant that launched publicly in May 2025, reached $1 billion in annualized revenue by November 2025, and passed $2.5 billion by February 2026. Enterprise customers spending at least $1 million annually doubled from 500 to 1,000 in under two months following the Series G. Anthropic has said eight of the Fortune 10 are now Claude customers.

The compute story is equally significant. At the company’s May 6 Developer Conference, Chief Product Officer Ami Vora announced that Anthropic would take over the entire computing capacity of xAI’s Colossus 1 data center in Memphis within the month — more than 300 megawatts and 220,000 Nvidia GPUs. The arrangement is being described publicly as a compute partnership. The economics, according to Fortune, are expected to generate between $3 billion and $4 billion in annual revenue for SpaceX. Anthropic needed capacity now; xAI had a facility that Grok’s user base never grew into. The strategic logic is transactional, not ideological.

The longer-dated infrastructure commitments are larger still. Amazon has agreed to invest up to $25 billion in Anthropic and secured up to 5 gigawatts of training and deployment capacity. Google committed up to $40 billion — $10 billion immediate at a $350 billion mark, with $30 billion more contingent on performance milestones — and separately locked in multiple gigawatts of next-generation TPU capacity through a three-way deal with Broadcom. Claude is now the only frontier model available natively across AWS Bedrock, Google Cloud Vertex AI, and Microsoft Azure Foundry simultaneously, a distribution position no competitor currently holds.

The Valuation Math — and Its Problems

At a $900 billion pre-money valuation and $30 billion in annualized revenue, Anthropic is being priced at roughly 30 times run-rate revenue. That multiple is lower than it looks in a historical context: Salesforce traded above 30 times revenue at peak, and it was generating cash. Anthropic’s gross margins have reportedly improved from 38% a year ago to above 70% — a number that, if accurate, suggests the unit economics of frontier model deployment are improving faster than the market expected. But Anthropic has not published audited financials. The $30 billion run-rate figure is a company-disclosed number. The gross margin improvement comes from secondary reporting. Investors committing $2 billion or more to this round are doing so without the disclosure architecture that would normally support a commitment of that size.

The more useful framing is what the valuation is actually underwriting. Anthropic has been signing deals — Amazon, Google, Broadcom, now SpaceX — that collectively represent tens of gigawatts of committed compute capacity, most of it not yet online. The company is spending now to secure infrastructure for revenue it expects to generate in 2027 and 2028. The $30 billion raise is not a reward for what has already happened. It is the financing required to not lose the position the revenue growth has created. As we examined in our analysis of the structural shift in AI capital formation, frontier model companies have moved beyond venture-style financing into something closer to infrastructure pre-purchasing — and the capital requirements scale with the revenue, not ahead of it.

The secondary market has been ahead of the primary rounds on valuation. Illiquid secondary trades implied Anthropic valuations near $1 trillion in late April 2026, before the Bloomberg report. That secondary pricing, while thin and not fully representative, was the first signal that institutional appetite for Anthropic exposure had moved past the $380 billion mark established in February. The $900 billion primary round is partly catching up to where sophisticated secondary buyers were already pricing the company.

The OpenAI Comparison Is Not What It Appears

The competitive framing — Anthropic’s $900 billion pre-money versus OpenAI’s $852 billion from March — is being treated in general financial coverage as a simple scoreboard reversal. It is more complicated than that. OpenAI’s $852 billion valuation was set on a company with a consumer-driven product in ChatGPT and an enterprise business that, as of the March filing, remained smaller than its consumer revenue as a share of total. Anthropic’s $900 billion mark is being set on a company where enterprise represents more than 80% of revenue and the flagship enterprise tool — Claude Code — accounts for a documented, compounding share of developer workflow that is measurably sticky.

Those are different businesses at the same headline valuation. The question for investors is not which number is bigger. It is which revenue composition is more defensible against the hyperscaler encroachment that is coming regardless. Google, Amazon, and Microsoft are all Claude distribution partners. They are also each building or acquiring competitive alternatives. As we covered in our examination of enterprise agentic AI revenue, the same enterprise customers adopting Claude Code are running parallel evaluations of GitHub Copilot, Google Jules, and Amazon Q. Enterprise stickiness in AI coding tools has not yet been tested through a product-cycle transition. The $30 billion in run-rate revenue is impressive. Whether it has the switching-cost structure to survive a competing product at a lower price, distributed natively through Azure or AWS enterprise agreements, is a different question.

The IPO backdrop gives this round its urgency. Bloomberg has reported that Goldman Sachs, JPMorgan, and Morgan Stanley are already in early IPO discussions, with a potential public debut as soon as October 2026. The May raise, if it closes at the reported valuation, serves a dual function: it provides the compute financing the business requires in the near term, and it sets the valuation anchor that underwriters will use when they begin building the IPO order book. A company that just closed a $900 billion private round does not go public at $600 billion. The round is also, in a meaningful sense, the last chance for large institutional investors to enter at private-market terms before the prospectus defines the entry price for everyone.

The Risk the Round Doesn’t Address

The structural question that a $900 billion valuation leaves unanswered is compute dependency. Anthropic’s revenue growth depends on the ability to serve demand it is already generating — and the company has been candid that it has not always been able to do that. In a postmortem published in late April, Anthropic acknowledged that three bugs had affected Claude Code since March 4 and that internal tests had not caught them, leading to several weeks of degraded performance. The company admitted publicly that demand had created “inevitable strain on our infrastructure” and that this had impacted “reliability and performance” during peak hours.

These are not signs of a company in distress. They are signs of a company growing faster than its infrastructure. The SpaceX deal addresses the near-term capacity gap. The Amazon and Google commitments address the 2027 horizon. What remains unresolved is the window between now and when those gigawatts come online — a period during which Anthropic is asking enterprise customers spending $1 million or more annually to accept intermittent reliability as the price of being early to the platform. For most enterprise software, that is an unacceptable trade. For Claude Code, the market appears to be accepting it, at least for now. How long that tolerance lasts is the variable the $900 billion valuation is most exposed to.

OpenAI’s IPO timeline is the other accelerant. As we noted in our analysis of OpenAI’s enterprise positioning, the sequence of the two companies’ public filings will determine which one controls the comparable. If Anthropic files first at a $900 billion-plus implied IPO valuation, it sets the reference point for the entire frontier AI category in public markets. If OpenAI files first, it does. The private round being discussed now is, among other things, a move to ensure Anthropic controls that sequence on its own terms.

What to Watch Next

- Round close confirmation and final terms. Bloomberg reported the deal expected to close by end of May. Whether the $900 billion figure holds or is revised at close — and whether any major tech strategic participates alongside the four named co-leads — will define the IPO anchor valuation.

- Annualized revenue trajectory through Q2. The $30 billion run-rate was disclosed April 7. The next public signal on revenue pacing will likely come at a developer conference or from secondary reporting. Any figure suggesting the growth rate is decelerating from the Q1 pace changes the multiple arithmetic significantly.

- Colossus 1 capacity absorption timeline. The SpaceX compute deal is expected to deliver 220,000 Nvidia GPUs within a month of the May 6 announcement. When Anthropic lifts the Claude Code rate limit restrictions it imposed during the infrastructure strain, that will be the first real-time signal that the capacity is live and deployed.

- OpenAI’s fundraising timeline and S-1 sequencing. OpenAI is reportedly working on a round that could reach $100 billion. The order of primary round closings and IPO filings between the two companies will determine which one sets the public market comparable — a question with nine-figure implications for both deals.

- Gross margin disclosure at IPO. The company’s reported improvement from 38% to above 70% gross margins is the most consequential unverified number in the Anthropic story. When audited financials become available in an S-1, the margin figure will either validate the $900 billion valuation or force a significant reset.