For most of its existence, the private company secondary market has operated on a simple principle: the people who know the most trade the most, and everyone else waits. A founding engineer sells shares through a bank-sponsored tender. A late-stage growth fund takes a stake at a negotiated price. The information that moved those transactions never left the room. On Tuesday, Polymarket and Nasdaq Private Market announced an exclusive partnership designed to change that dynamic — or at least route around it.

The deal is straightforward in structure. a new category of contracts tied to private company milestones — valuation thresholds, IPO timing, secondary market activity — with Nasdaq Private Market serving as the exclusive resolution data provider. The first wave of markets covers OpenAI, Anthropic, SpaceX, Stripe, Kraken, Anduril, and Databricks. Traders are not buying equity. They are taking positions on whether specific, verifiable events happen — whether OpenAI’s IPO values the company above $1 trillion before 2027, whether Anthropic crosses $500 billion in 2026, whether Stripe goes public at all. The contracts settle based on NPM’s transaction and valuation data from primary and secondary markets.

What Nasdaq Private Market Actually Brings

The credibility of any prediction contract is only as good as its resolution mechanism, and that is where NPM’s role matters. The firm has operated since 2013, facilitating nearly $80 billion in liquidity across more than 1,000 company-sponsored programs for over 200,000 eligible shareholders. Its ownership — a bank consortium that includes Goldman Sachs, Morgan Stanley, and Citigroup — positions it as a platform that works with institutional capital, not against it. When a Polymarket contract resolves on whether Stripe’s valuation crossed a given threshold, the data anchoring that outcome will come from the same infrastructure the largest private wealth platforms already rely on.

Rodolfo Sanchez, VP of Data at Nasdaq Private Market, framed the partnership as a two-way signal in a joint statement Tuesday: “We anchor every market with institutional-quality data on the underlying companies, and the activity in those markets becomes a real-time signal that institutional investors can use on private company performance reflected back through a much broader market.” That framing is deliberate. NPM is not positioning this as retail entertainment. It is positioning it as a new pricing layer that flows information back into a market that has historically struggled to produce any continuous price signal between funding rounds.

The Discovery Problem It Is Trying to Solve

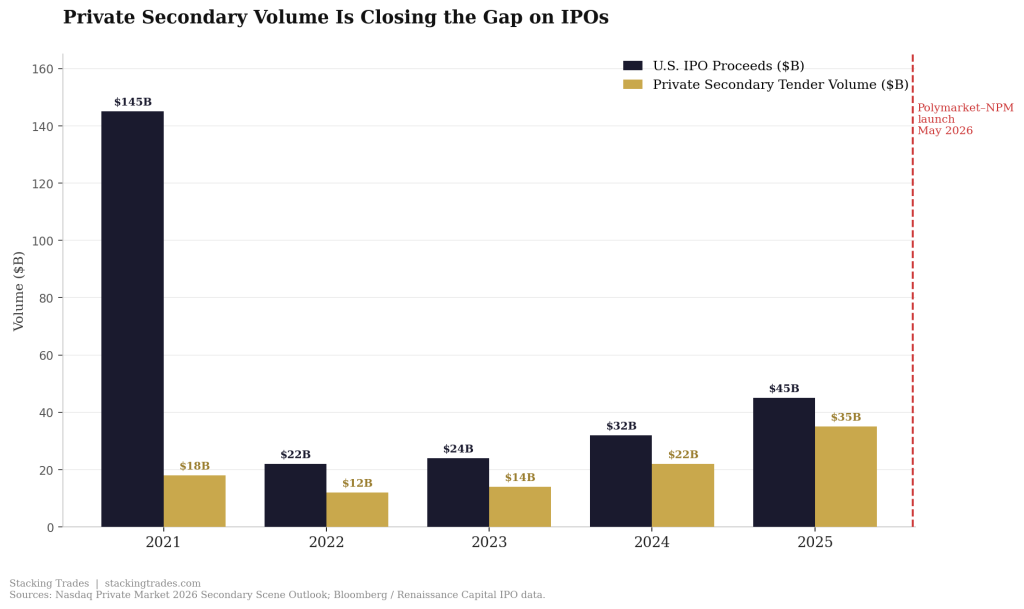

Private company valuation has always been episodic. A company raises a round, a price gets set, and then nothing verifiable happens for 12 to 18 months. Secondary trades fill some of the gap — NPM’s own 2026 outlook shows tender volume hit $35 billion in 2025, compared to roughly $45 billion in IPO proceeds — but those transactions are bilateral, private, and reported with a lag. The result is a market where even sophisticated investors are effectively pricing off stale data, rumor, and secondary aggregators that rely on self-reported transaction details.

Polymarket’s pitch is that a liquid prediction market, continuously traded, produces a faster signal. Its CEO, Shayne Coplan, said in Tuesday’s joint statement that “prediction markets are one of the most powerful tools we have for democratizing access to financial information and opportunity.” Tom Callahan, NPM’s CEO, put the resolution side plainly: “Polymarket has built the platform that can open access to a broader audience. We are proud to provide the data that ensures every market resolves accurately.”

The concept has precedent in public markets, where event-driven contracts — on earnings beats, M&A closing conditions, regulatory approvals — have been used by institutional traders for years to price binary outcomes between announcement and execution. The question is whether that logic ports cleanly to private companies, where the information set is smaller and the events themselves are harder to define cleanly.

“The data flows in both directions. We anchor every market with institutional-quality data on the underlying companies, and the activity in those markets becomes a real-time signal that institutional investors can use on private company performance reflected back through a much broader market.”<

— Rodolfo Sanchez, VP of Data, Nasdaq Private Market, May 19, 2026

The Structural Limits of Prediction as Discovery

There is a credible case to be made that prediction markets generate useful signals. But a working paper published last month, analyzing all trades from 2023–2025, found that roughly 3% of traders account for most price discovery on the platform. The remaining 97% provided volume and liquidity but were, in aggregate, on the losing side of trades against a small, informed minority. That finding does not invalidate the signal — concentrated expertise moves prices toward truth in traditional markets too — but it does complicate the democratization narrative. The prediction market does not aggregate the crowd’s wisdom so much as it aggregates the positions of a few well-informed traders against a much larger pool of retail capital.

For private company contracts specifically, the information asymmetry is sharper than in political or macroeconomic prediction markets. Traders with direct knowledge of a company’s recent secondary trades or cap table activity will price these contracts more accurately than those guessing from public filings and press releases. That is not a flaw in the Polymarket-NPM design — it is simply the nature of private markets. But it means sophisticated investors using these contracts as a signal should think carefully about what exactly is being surfaced. A high probability on an OpenAI $1 trillion IPO contract reflects the views of the most informed traders on that platform. It is not the same as an institution with board access revising its NAV.

The Regulatory Backdrop That Makes This Possible

This product could not have launched two years ago. Polymarket spent 2022 through mid-2025 barred from U.S. users after settling with the CFTC over unlicensed binary options contracts. The path back opened in July 2025, when the agency dropped its investigation and the company acquired QCEX, a CFTC-licensed exchange and clearinghouse, for $112 million. In November 2025, the CFTC issued an order allowing Polymarket to operate a federally regulated platform in the United States. The company has recorded nearly $39 billion in U.S. volume so far in 2026, and new market launches have hit consecutive monthly highs over the past year.

The state-level picture remains messier. Nevada, Connecticut, and several other states maintain active enforcement postures, and the CFTC is currently suing multiple states to assert federal preemption over prediction market regulation. Polymarket separately disclosed in late April that it is seeking CFTC approval to lift its remaining U.S. restrictions and bring its main offshore exchange fully back into the domestic market. That process is pending a commission vote. The private company contracts launched Tuesday operate under the existing CFTC-authorized U.S. platform, but the broader regulatory environment around prediction markets is still unsettled enough that institutional adoption will require legal teams to clear the product before trading desks use it as anything other than a supplemental signal.

What This Means for Private Market Access Broadly

The Polymarket-NPM deal arrives in a week where the private market access question is acute. OpenAI just cleared its last major legal cloud. Cerebras priced its IPO with a book more than 20 times covered. The companies that have concentrated the most pre-IPO value — OpenAI, Anthropic, SpaceX, Stripe — are exactly the names in Polymarket’s first market roster. These are also the names absorbing the most capital in a Q1 2026 venture cycle that was structurally different from prior booms.

For investors who cannot buy into these companies directly — which is virtually everyone outside the accredited investor class, and many within it — prediction contracts offer a form of expressed view, but not economic exposure. A winning bet on OpenAI’s IPO valuation pays out in USDC; it does not compound alongside the company’s growth between now and listing. Robinhood’s Ventures Fund I, which drew 150,000 retail investors by May 5, offers something closer to economic participation: a publicly traded closed-end fund with daily liquidity holding actual private equity stakes, albeit with NAV and discount dynamics that remain untested. The two models are not competing so much as addressing adjacent needs — one for information, one for return.

What Polymarket and NPM have built is, at minimum, a new pricing signal in a market that desperately needs more of them. Whether it becomes something more — a tool institutional investors use alongside, or even instead of, proprietary secondary data — will depend on how the first contracts perform and what the resolution track record looks like after a year of trading. Private market data has always moved value. Now some of it will move in public.

What to Watch Next

- The first contract resolutions. The OpenAI $1 trillion IPO contract and the Anthropic $500 billion valuation contract are the two most watched early markets. How those resolve — and whether NPM’s data matches market expectations — will determine whether institutional traders incorporate the signal into their workflows or treat it as noise.

- Robinhood Ventures Fund I trading vs. NAV. If the closed-end fund continues to trade at a discount to the net asset value of its private holdings, it reveals genuine skepticism about private valuations that the prediction market contracts are simultaneously pricing as probable. The two signals in conflict would be the more interesting story.

- Polymarket’s CFTC reauthorization vote. The commission’s decision on lifting the remaining U.S. access restrictions — currently pending with a single sitting commissioner — would materially expand the platform’s addressable U.S. trader base and increase the depth behind these new private company contracts.

- Whether any major secondary platform — NPM, Forge, or EquityZen — uses Polymarket contract prices as a public reference point in its own pricing communications. That step, if it happens, would formalize the link between prediction market sentiment and institutional secondary pricing in a way that closes the information loop.

- State-level preemption resolution. The CFTC’s lawsuits against multiple states over prediction market jurisdiction will determine whether the product’s U.S. availability remains patchwork or becomes uniform. A Supreme Court cert grant on the preemption question, currently priced by traders at 64% probability before year-end, would be the single most important regulatory event for the category.