Nobody rings a bell when the IPO window opens. But Entrata’s S-1, filed Thursday on the NYSE under the proposed ticker “ENT,” comes as close as any single document can. The Silver Lake-backed property management software company posted $143.5 million in Q1 2026 revenue, up 23% year over year, alongside $23.3 million in net income. It is profitable, growing, and competing for capital at the same time SpaceX is consuming the oxygen in every institutional allocator’s conversation. How Entrata prices and trades in the next few weeks will carry implications well beyond multifamily software.

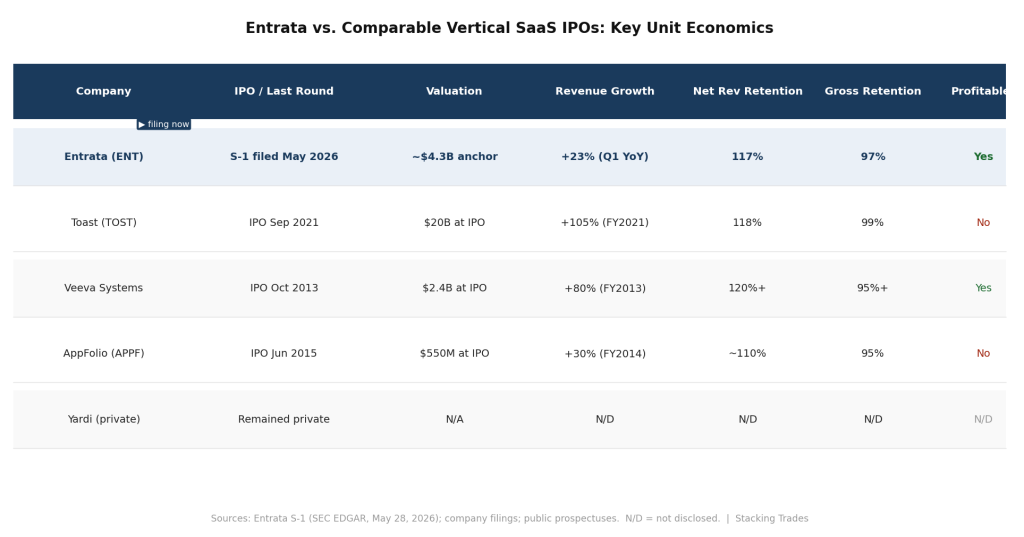

The company has spent two decades building what it calls an operating system for apartment communities — a single platform covering leasing, payments, maintenance, accounting, and resident communications. That framing matters for investors, because vertical software that sits at the operational core of a customer’s business tends to generate the kind of retention numbers that make institutional underwriters comfortable. Entrata’s net revenue retention held at 117% in both 2024 and 2025. Gross retention stayed at 99% in 2024 and 97% in 2025. Those are not metrics that get accidentally produced.

A Platform 2.5 Million Units Deep

As of March 31, 2026, Entrata powers 2.5 million residential units across the United States. Four of the ten largest multifamily operators in the country — as ranked by the National Multifamily Housing Council — run on Entrata, along with ten of the top fifty. The platform processes more than 4.5 billion system transactions per day through its Unified Data Layer, a proprietary architecture designed to capture operational data across every touchpoint from lease signing to rent collection.

The company’s AI layer, which it calls ELI — Entrata Layered Intelligence — is embedded across the operating system at no charge in its base form, with a premium tier called ELI+ covering agentic tools for leasing, payments, renewals, and maintenance. That embedded approach is strategically significant. It means AI adoption is not a separate sales motion requiring new contracts and new budget conversations. It is a default feature for every customer on the platform, which positions Entrata well as property managers face growing margin pressure and regulatory scrutiny around fee transparency.

“Over twelve million residents in properties across the largest property management portfolios in the world utilize the Entrata operating system.”

— Adam Edmunds, CEO, Entrata, May 2025

The Blackstone Anchor and What It Implies

The most useful pricing reference for institutional investors is not a comparable company multiple — it is the $4.3 billion valuation Blackstone placed on its $200 million minority stake in May 2025. That number is now over a year old, and the company has continued growing since. Entrata reported full-year 2025 revenue growth of 24% over 2024, and Q1 2026 came in above that pace. If the offering prices above the implied $4.3 billion anchor, it signals that the market is crediting the growth trajectory. If it prices below, the more interesting question becomes whether institutional buyers are discounting the Silver Lake controlled-company structure — Entrata will list with a three-class share structure that gives Silver Lake retained voting control after the offering.

That governance design is worth flagging. Under New York Stock Exchange rules, Entrata will be a “controlled company” as defined by its corporate governance standards, which exempts it from certain board independence requirements. Sophisticated investors have priced this dynamic before, from Snap to Lyft, and the discount applied — or not applied — tends to be a direct function of how much trust the market extends to the controlling shareholder. Silver Lake’s track record in enterprise software gives it more benefit of the doubt than most PE sponsors would receive in the same position.

The Timing Question Is Bigger Than Entrata

Entrata is not pricing into a vacuum. The 2026 IPO calendar has 150 U.S. listings through May 27, running about 10% ahead of 2025’s pace at the same point. But the volume figure obscures a more selective environment. Large PE-backed software companies have been notably absent from that list. Entrata is the first meaningful test of whether institutional allocators will step up for a software business valued north of $4 billion when the same capital pools are simultaneously being asked to fund SpaceX’s book-build and evaluate an OpenAI roadshow expected later in 2026.

The 10-year Treasury has been trading above 4.5% for most of May, a rate environment that compresses terminal value multiples on high-growth software. Entrata’s profile is somewhat insulated from that dynamic — the company is profitable, and its growth is driven by land-and-expand within a deeply embedded customer base rather than aggressive new customer acquisition spend. But profitability alone does not immunize a deal from rate-driven multiple compression. The question is whether the premium for capital efficiency is large enough to offset the discount applied by a risk-off backdrop. That answer will only exist after the amended S-1 carries a price range.

The IPO as Market Signal

Entrata’s reception matters for a pipeline of private-equity-backed software companies that have been waiting for exactly this kind of proof point. A deal that prices at or above the Blackstone anchor and holds above issue price in the first two weeks of trading creates a template. A deal that struggles — whether at pricing, on the first day, or in the weeks immediately following — resets the timeline for every PE sponsor calculating whether the window is open or merely ajar. The market has had other signals about IPO window conditions this year, but most of them have been negative — withdrawn deals, delayed filings, and cautious commentary from investment banks that keep adjusting their timing outlook. Entrata is a positive data point that has actually pulled the trigger. That distinction matters.

The company’s sector also plays into the read-through. Multifamily property management software is not AI infrastructure, not defense technology, and not frontier biotech. It is a mature vertical with stable demand, low customer concentration, and a business model built on monthly payment processing that has a near-mandatory character for anyone using the platform. That profile does not generate the kind of speculative excitement that drove Cerebras’s first-day trading, but it is exactly the profile that long-only institutional capital needs to see performing well before it feels comfortable broadening its 2026 IPO participation beyond the handful of marquee technology listings.

What to Watch Next

- The amended S-1 with a share count and price range — the current filing carries no dollar figures for the offering price or expected proceeds. That document is the first hard valuation data point for institutional modeling, and the spread between the implied range and the $4.3 billion Blackstone anchor will immediately set the tone for demand-building.

- Silver Lake’s retained voting percentage post-offering. The S-1 notes that Silver Lake will control the majority of voting power after the IPO, but the exact percentage depends on the share structure and offer size disclosed in the amendment. That number will determine how governance-sensitive institutional investors respond to the deal.

- Book-build signals from Goldman Sachs and J.P. Morgan. Given the rate environment and the size of competing deals in the pipeline, order quality — not just order volume — will indicate whether the institutional appetite for profitable, PE-backed software has genuinely returned or whether Entrata is absorbing the capital that would otherwise go into a more defensive position.

- First-day trading relative to the offer price. A strong opening would mark the clearest signal yet that the PE-backed software window is open and that the SpaceX-dominated narrative has not consumed all available institutional bandwidth for new issues.

- ELI+ adoption rate in the first post-IPO earnings report. Management’s embedded AI strategy is currently described in qualitative terms in the S-1. Once Entrata is a public reporting company, the contribution of premium AI products to ARPU expansion will be the most direct test of whether the ELI architecture is a genuine revenue driver or a feature positioned to look competitive during a roadshow.