For the past two years, the AI infrastructure trade has lived at Nvidia. The logic was simple: training large models requires massive GPU clusters, Nvidia supplies the clusters, and everyone else is downstream. That framing was accurate as far as it went. It didn’t go far enough.

The enterprise hardware tier — the servers, networking gear, and storage systems that sit beneath the GPU stack and handle the actual deployment of AI into corporate workflows — just posted its clearest earnings cycle yet. Dell, HPE, and NetApp all reported within 72 hours of each other. The numbers are not incremental. They are structural.

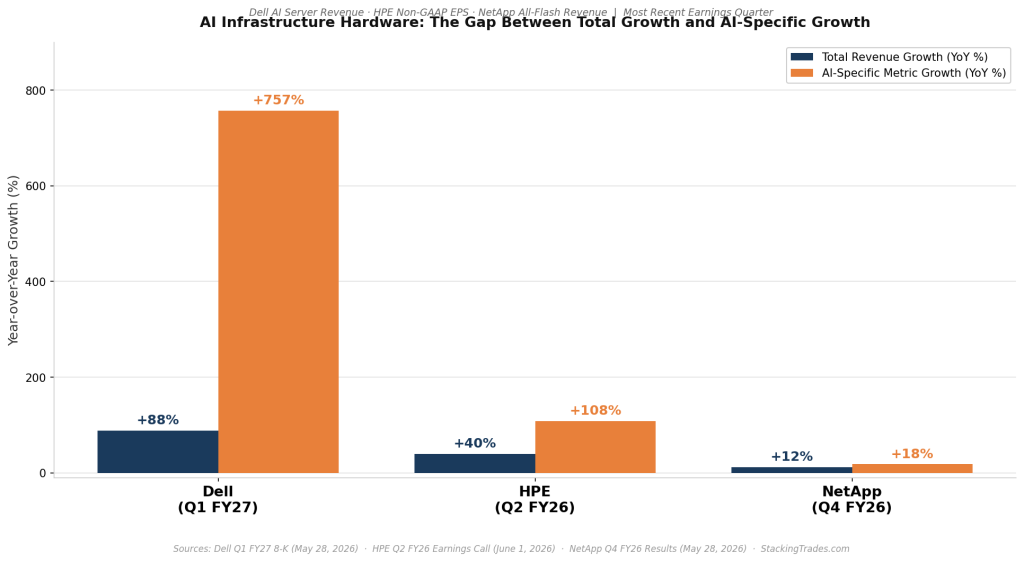

Dell Set the Tone First

Dell Technologies reported fiscal first-quarter 2027 results on May 28, 2026, and the figures were difficult to contextualize at normal scale. Total revenue reached $43.8 billion, up 88% year over year — the fastest growth rate in the company’s history as a public company. AI-optimized server revenue hit $16.1 billion in a single quarter, a 757% year-over-year increase. The company booked $24.4 billion in AI orders and exited the quarter with a record $51.3 billion in AI backlog.

Vice Chairman and COO Jeff Clarke raised the company’s full-year AI server revenue forecast to $60 billion. To put that in context: Dell’s entire revenue for fiscal year 2024 was $88 billion. It is now guiding for more than two-thirds of that figure from a single product category in a single year.

“Demand was even stronger than revenue growth. Orders more than doubled, significantly outpacing revenue, resulting in a record company backlog. Customer investments in agentic AI and AI inferencing accelerated.”

— Antonio Neri, President & CEO, Hewlett Packard Enterprise, Q2 FY26 Earnings Call, June 1, 2026

HPE: Where Demand Runs Ahead of Revenue

HPE’s fiscal second-quarter 2026 results, reported June 1, reinforced the Dell read from a different angle. Revenue of $10.7 billion was up 40% year over year, and non-GAAP EPS of $0.79 increased 108% — but the more important number was in the backlog. Orders more than doubled and significantly outpaced revenue growth, leaving HPE with a record AI systems backlog of $5.9 billion as it entered the third quarter. The company booked $1.8 billion in new AI systems orders during the quarter alone, bringing cumulative AI systems bookings to $16.4 billion.

The supply constraint that is limiting HPE’s revenue conversion — memory and processor availability — is the same one Dell flagged. In both cases, the message is the same: the ceiling on near-term revenue is supply, not demand. That distinction matters. A demand cliff can emerge without warning. A supply constraint resolves as procurement agreements are locked in and capacity comes online, and HPE noted it already has supply locked for known demand scenarios.

HPE raised its full-year fiscal 2026 EPS guidance by more than 40%, to $3.35–$3.45, and its free cash flow outlook to at least $3.5 billion. It also issued an early fiscal 2027 framework — a step the company rarely takes — citing durable demand visibility as the reason. CEO Antonio Neri was specific about what is driving the acceleration: agentic AI workloads. The shift from training to inference and, increasingly, to agentic deployment is expanding the addressable hardware market beyond pure GPU infrastructure into networking, compute, storage, and memory simultaneously.

NetApp Is the Storage Signal Everyone Is Underreading

NetApp reported fiscal fourth-quarter 2026 results on May 28. Total revenue of $1.95 billion was up 12% year over year — modest by Dell and HPE standards, but the composition matters more than the headline. All-flash array revenue for the quarter hit $1.2 billion, up 18% year over year, and the full-year all-flash figure reached $4.2 billion. CEO George Kurian disclosed more than 1,100 AI and data preparation wins for the fiscal year, compared with roughly 400 the prior year.

Kurian’s explanation of the storage demand dynamic is worth tracking closely. Roughly half of NetApp’s AI use cases were tied to data preparation and large-scale analytics — not model training or inference directly, but the underlying data work that precedes both. The other half was split between training and inferencing. That breakdown reveals something about where enterprise AI deployment actually lives: in messy, unstructured data pipelines that require high-performance, scalable storage infrastructure long before a GPU ever processes a query.

NetApp guided fiscal 2027 revenue growth at roughly 8% at the midpoint, raised its buyback authorization by $1 billion, and stated its intent to return up to 100% of free cash flow to shareholders. For a company trading at more restrained multiples than its server-focused peers, the shareholder return posture signals management confidence in the durability of the demand environment.

Why This Cluster of Results Changes the Portfolio Conversation

The hyperscalers — Microsoft, Google, Amazon, Meta — have been the visible faces of the AI infrastructure buildout. Their capital expenditure commitments have been covered in detail here and elsewhere. What this week’s earnings cycle revealed is that the $690 billion in hyperscaler capex is not an abstraction. It is flowing through the hardware supply chain as real purchase orders, real backlog, and real revenue at companies that trade at fractions of the hyperscaler multiple.

Dell’s Infrastructure Solutions Group now generates more revenue in a single quarter than most large-cap companies generate in a year. HPE’s backlog-to-revenue gap is a leading indicator of near-term earnings revisions, not a risk factor. NetApp’s AI win count tripled year over year. Taken together, these three reports are the earnings-cycle confirmation of a thesis that has been priced speculatively in the hyperscalers for two years and is only now showing up in the enterprise hardware tier at scale.

The market moved accordingly. Dell surged more than 30% after hours on May 28. HPE jumped roughly 30% in after-hours trading on June 1. NetApp moved in the same session. These are not typical earnings reactions. They reflect a rerating event — investors updating their models on what AI infrastructure actually looks like when it converts from capital commitment to shipped revenue.

What the Margin Picture Is Telling You

Not every signal here is straightforwardly positive. Dell’s AI server gross margins are compressing. The Infrastructure Solutions Group margin came in at 10.5% in the most recent quarter, below historical levels, because AI-optimized servers carry lower gross margins than traditional enterprise hardware. The volume is extraordinary; the per-unit profitability is thinner. HPE has flagged that it expects continued elevated costs into fiscal 2027 due to supply chain pressures, particularly in memory. NetApp is managing component cost increases affecting its all-flash line.

The margin question is the right analytical tension to hold. Revenue growth at 40% to 88% is extraordinary. The durability of that growth at current margins — or the pace at which margins normalize as supply constraints ease and mix shifts toward software and services — is the variable that separates this from a one-cycle event. HPE’s explicit commentary on its path to margin recovery, tied to inferencing demand growth through the end of the decade, suggests management sees the margin compression as transitional rather than structural. The next two quarters will either confirm or challenge that read.

What to Watch Next

- HPE Q3 FY26 results, expected late August — the company guided revenue of $11.5 billion to $12.1 billion. Whether backlog conversion accelerates as supply constraints ease is the central test. Any commentary from CFO Marie Myers on whether the $5.9 billion AI systems backlog is converting at pace or continuing to build will reset near-term estimates.

- Dell Q2 FY27 results, also expected late August — the $60 billion full-year AI server revenue target implies roughly $15 to $16 billion per quarter for the remaining three periods. Whether Dell hits the midpoint is the single clearest test of whether the AI server supercycle is sustaining or beginning to exhaust addressable near-term demand.

- Memory pricing and supply availability. Both Dell and HPE explicitly cited memory as the primary near-term supply constraint. Any announcements from Micron, Samsung, or SK Hynix on HBM and NAND allocation timelines will directly affect how quickly either company can convert backlog into revenue — and whether Q3 guidance can be exceeded or will face continued supply-side friction.

- AI inferencing margin data as it surfaces. HPE’s Neri said he expects inferencing to represent the majority of long-term AI demand. The margin profile of inferencing hardware — which requires less custom GPU and more networking, memory, and storage — is where HPE and NetApp are best positioned relative to Dell. Watch for any product-level margin disclosures that begin to separate inferencing economics from training economics in public filings.

- Enterprise AI adoption data from software companies. HPE and NetApp’s backlog growth is a forward indicator, but the sustainability of that demand ultimately depends on whether enterprises are deploying AI at scale rather than piloting it. Salesforce, ServiceNow, and SAP earnings will provide the best read on whether enterprise AI spend is compounding or flattening at the application layer.