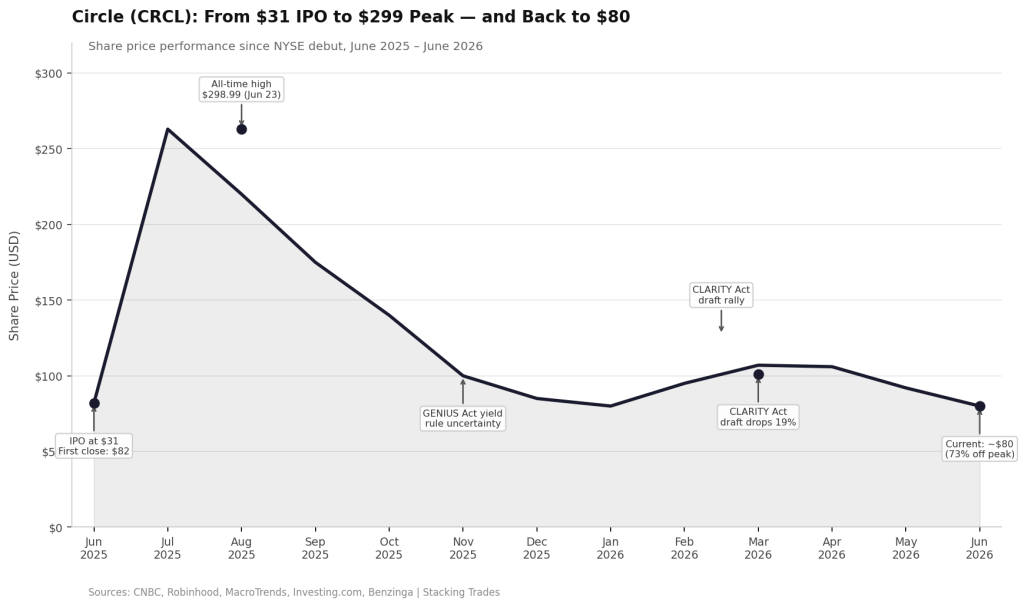

Circle Internet Group priced its IPO on June 4, 2025, at $31 per share. By June 23, the stock was trading near $299. Less than a year later, it sits around $80 — down more than 73% from its peak — and the company’s core revenue arrangement is facing a regulatory rewrite with no confirmed outcome. For investors who bought the USDC story, the question is no longer whether Circle won the stablecoin race. It’s whether the business model it built to monetize that win is structurally sound.

The mechanics are worth understanding before the risk. Circle earns money primarily by holding the dollar reserves that back every USDC token in circulation. Those reserves are invested in short-term U.S. Treasuries, and Circle keeps the interest. As of late 2025, USDC in circulation had reached roughly $75 billion, and Circle’s full-year revenue came in at approximately $2.7 billion — almost entirely from that reserve income. That model works well when interest rates are elevated and USDC supply is growing. Both conditions held through 2025. Neither is guaranteed going forward.

The Coinbase Deal Is the Pressure Point Nobody Wants to Say Out Loud

Circle does not keep all of that reserve income. Under a revenue-sharing agreement established in 2023 when Circle dissolved its Centre Consortium with Coinbase, Coinbase receives 100 percent of the interest earned on USDC held on its own platform, plus 50 percent of the interest earned on USDC held elsewhere. That arrangement made Coinbase the most powerful distribution partner in the stablecoin market — and it made Circle permanently dependent on a deal it does not control. The arrangement is up for renewal in 2026.

The renewal is not a routine renegotiation. The GENIUS Act, signed into law in July 2025, introduced the first federal framework for payment stablecoins and banned issuers from paying yield directly to holders. The OCC’s February 2026 proposed rulemaking went further, flagging the Coinbase-Circle revenue-sharing arrangement specifically as a potential violation of that prohibition. The OCC’s position: if a third party pays stablecoin holders interest in connection with holding the token, and the stablecoin issuer has an arrangement with that third party tied to balances, it may constitute prohibited yield. The comment period closed May 1 with no final rule issued. Circle and Coinbase both remain exposed to the ambiguity.

“We saw very strong growth in Q3. I think that growth has come from, yes, the regulatory clarity.”

— Jeremy Allaire, CEO, Circle Internet Group, Q3 2025 earnings call, November 2025

That confidence was tested on March 24, when draft CLARITY Act language targeting passive stablecoin yield landed without warning. Circle fell nearly 19 percent in a single session, erasing roughly $2 billion in market capitalization on volume nearly four times the 20-day average. Coinbase dropped 11 percent the same day. The stocks moved together because the income they share moves together.

The Rate Sensitivity Is Structural, Not Temporary

Circle’s margin problem runs deeper than the regulatory argument. The Federal Reserve cut its policy rate three times in late 2024, bringing the target range from 5.25 to 5.50 percent down to 4.25 to 4.50 percent by December. Additional cuts are expected in 2026. Each 100 basis points of cuts removes an estimated 25 to 30 percent from Circle’s gross reserve income — before distribution costs to Coinbase are applied. A terminal rate of 3.75 percent by end-2026, on a $60 billion USDC supply, would reduce gross reserve income from approximately $3 billion annualized to approximately $2.25 billion. That $750 million shortfall is not marginal. It is the gap between the story the IPO told and the earnings trajectory the current rate path implies.

The bull response is USDC supply growth. Circle projects a 40 percent compound annual growth rate in USDC circulation. If USDC balances grow fast enough, the larger supply base offsets the lower rate on each dollar of reserves. That math works, but it requires a continuation of the distribution relationships — primarily Coinbase — that are simultaneously under regulatory review. Faster USDC growth and a renegotiated Coinbase deal are not independent variables. They are correlated, and the correlation runs in the wrong direction.

New Competition Is Arriving With Balance Sheets Circle Does Not Have

The GENIUS Act’s federal licensing framework was supposed to be Circle’s competitive moat. The theory was that a clear federal standard would validate USDC as the compliant dollar stablecoin of record and slow potential entrants who lacked Circle’s regulatory groundwork. The theory was correct about the framework. It was wrong about the competitive dynamics it would create.

Any bank holding a national charter can now apply for a Permitted Payment Stablecoin Issuer license under the GENIUS Act. JPMorgan Chase announced its JPMD stablecoin pilot in March 2025 and is targeting broad availability in late 2026. Stripe, Visa, and Mastercard are reported to be near the launch of a joint stablecoin platform. These are not venture-backed startups building distribution from scratch. They are institutions with existing payment rails, existing merchant relationships, and existing consumer trust. Their entry into the stablecoin market is possible precisely because Circle helped build the regulatory argument for the category — and they arrive with structural cost advantages Circle does not possess.

Circle’s operating cost base does not compress with interest rates. Compliance infrastructure, legal costs, and technology headcount remain fixed regardless of what the Fed funds rate does in the second half of 2026. Bank-chartered stablecoin issuers do not face the same cost structure, and they arrive with distribution that Circle spent years building at significant expense through the Coinbase revenue-sharing arrangement that is now at risk of renegotiation.

What the Arc Bet Actually Represents

Circle’s answer to the reserve-income problem is its Arc blockchain, a Layer-1 network the company launched on public testnet in Q3 2025 with more than 100 institutional partners, and which it plans to bring to mainnet in 2026. Arc is designed as an enterprise-grade infrastructure layer for stablecoin-native applications — AI agent payments, cross-border settlement, tokenized asset issuance. The bet is that fee-based revenue from network usage can eventually supplement or diversify beyond the Treasury income dependency.

The investment case for that bet is real. USDC adjusted transfer volumes grew approximately 320 percent year over year in 2025, a figure that suggests transaction-based usage is accelerating alongside the growth in outstanding supply. The Circle Payments Network, which went live in 2025, is building toward a fee structure that does not depend on interest rates. Allaire has argued publicly that usage-driven models — cashback on transactions, merchant loyalty programs, tiered enterprise pricing — are the correct direction regardless of what regulators decide about yield.

The timing problem is that Arc has no disclosed revenue and no public milestone against which to measure execution. It is the growth story for a company whose current earnings story is under simultaneous rate pressure, regulatory uncertainty, and distribution risk. Investors who bought Circle near its peak were implicitly paying for Arc’s option value at the same time the market was pricing the reserve-income stream at full capacity. Both assumptions fit when the stock was at $299. At $80, the question is which one the market still believes.

The IPO Comparison That Matters Most Right Now

Circle is not the only company navigating the gap between its private-market story and its public-market reality. The broader 2026 IPO pipeline has been shaped by exactly this dynamic: companies with compelling structural theses that priced into compressed multiples once institutional investors engaged with the underlying earnings mechanics. Circle’s version of that problem is particularly concentrated because 96 percent of its 2025 revenue came from a single source — interest on reserves — that is simultaneously rate-sensitive, structurally dependent on one distribution partner, and now under active regulatory scrutiny.

The average analyst price target on CRCL sits near $143, implying meaningful upside from current levels if the Coinbase renewal closes favorably and the OCC’s yield prohibition does not extend to the revenue-sharing structure. That is a real scenario. It is also a scenario in which the thesis requires three separate favorable outcomes — rate stability, regulatory clarity, and a renegotiated Coinbase deal — to arrive simultaneously. Investors are being asked to pay for optionality on all three, in a period when each is genuinely uncertain.

What to Watch Next

- The OCC’s final rule on the GENIUS Act yield prohibition. The comment period closed May 1. Any final language that explicitly exempts white-label distribution payments — the structure that most closely describes the Coinbase arrangement — would remove the largest regulatory overhang on the stock. Language that affirms the presumption of violation would force a restructuring of the deal before renewal.

- The Coinbase revenue-sharing renewal terms. The 2023 agreement is up for renegotiation in 2026. Any public disclosure of revised terms — either in an 8-K, earnings commentary, or investor presentation — will be the single most consequential data point for modeling Circle’s net reserve income through 2027.

- USDC circulation trajectory through Q2 and Q3. Circle’s Q3 2025 earnings showed USDC in circulation at $73.7 billion, up 108 percent annually. The Q2 2026 figure will show whether the growth rate is sustaining, moderating, or compressing. A supply figure above $85 billion would support the rate-offset thesis; below $70 billion would not.

- JPMorgan JPMD availability and Stripe-Visa-Mastercard stablecoin platform launch. These are the first institutional-distribution competitors with the balance sheets to challenge USDC’s position in enterprise payment infrastructure. Their go-to-market timing and initial merchant adoption will define whether the competitive threat is structural or manageable.

- Arc mainnet launch and first disclosed fee revenue. Any announcement of a named enterprise partner committing volume to the Arc network — or any commentary in Circle’s next earnings that quantifies non-reserve fee income — would be the first evidence that the diversification thesis is converting from roadmap to income statement.