For most of its decade-long existence, investment crowdfunding operated in a corner of the capital markets that big institutions mostly ignored. The deal sizes were small, the regulatory frameworks were niche, and the investor base — enthusiastic but modest — wasn’t worth the compliance overhead for a JPMorgan or a Fidelity. That dynamic has shifted sharply in the past six months, and the implications for platforms like Wefunder, StartEngine, and Republic are only beginning to come into focus.

The Year Crowdfunding Almost Hit $1 Billion

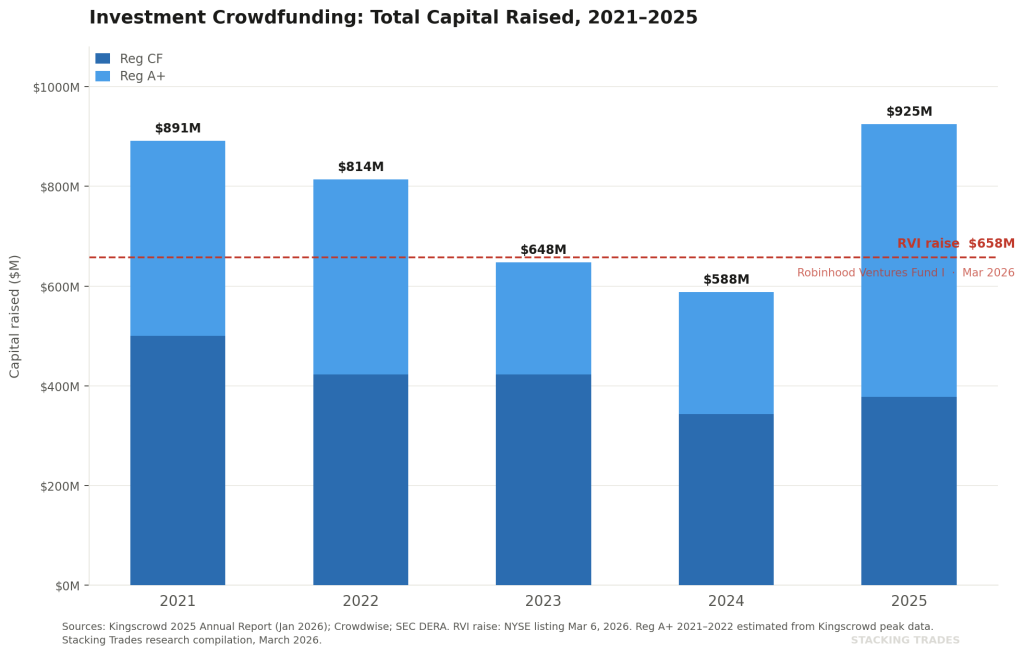

The industry’s own numbers tell a meaningful story. Investment crowdfunding — combining Reg CF and Reg A+ — grew 58% in 2025 compared to 2024, reaching $924.8 million raised. That is not a niche market. It is a market approaching institutional relevance, and it grew through a year when the S&P 500 swung violently on tariff headlines and rate uncertainty.

The platform rankings held steady. Wefunder led Reg CF with $109 million raised, followed by StartEngine at $89 million, DealMaker at $66 million, and Republic at $20 million — the exact same top-four ranking as in 2024. On the Reg A+ side, the story was more concentrated. DealMaker dominated with $292 million raised in Reg A+ — more than half of all capital raised under that exemption.

StartEngine’s cumulative investment volume on the platform surpassed $1 billion by 2024 and exceeded $1.5 billion by mid-2025. Wefunder, which has operated longer and built its identity around mission-driven founders, claims similar momentum. The platforms are no longer scrappy upstarts running on goodwill and JOBS Act optimism. They are scaled marketplaces with real infrastructure — and real competition arriving at the door.

Robinhood's Bet and Its First-Day Stumble

The clearest sign that Wall Street has moved into the retail private markets space landed on March 6, when Robinhood debuted its Robinhood Ventures Fund I on the New York Stock Exchange under the ticker RVI. The fund raised $658.4 million, offering retail investors access to high-profile late-stage private companies including Databricks, valued at $134 billion as recently as February, fintech firm Ramp at $32 billion, and Revolut.

The debut was not clean. The fund priced at $25 per share, opened at $22, and closed its first trading day at $21 — an 11% drop that cast immediate doubt on investors’ appetite for concentrated late-stage private exposure. Industry analysts pointed to a “liquidity discount” that often affects closed-end funds, where share price trades below the net asset value of the underlying holdings. In RVI’s case, the market appeared to be pricing in skepticism about private valuations that have faced scrutiny throughout early 2026.

Robinhood CEO Vlad Tenev was direct about the strategic rationale. “You have companies that are out there at valuations in the hundreds of billions, even getting into the trillions in private markets before retail investors get a chance to come in at all, and this is happening more and more,” Tenev told CNBC on the morning of the listing.

The argument is hard to dispute. The mechanism for delivering on it is a different question entirely.

“The long-awaited democratization of private equity hit a significant speed bump today. Early trading suggests investors are still working out how to price a concentrated, late-stage private portfolio in real time.”

— FinancialContent, March 6, 2026

JPMorgan Enters From the Other Direction

While Robinhood came at retail private markets from the bottom up — a consumer app expanding upmarket — JPMorgan Asset Management has moved in from the top down. The firm released its 2026 Global Alternatives Outlook in December 2025, framing private markets as “a structural mainstay of global finance” and positioning its $600 billion alternatives platform as the institutional-grade option for investors seeking exposure across private equity, private credit, real estate, and infrastructure.

The firm’s Global Head of Private Markets, Jed Laskowitz, put the thesis plainly: “As many leading companies are staying private for longer, the private markets are deep and diverse, and the opportunity for investors is immense.”

JPMorgan filed product documentation for its JPMorgan Private Markets Fund in January 2026, targeting individual investors with a vehicle designed to offer periodic liquidity through structured tender offers — a model that competes directly with the closed-end fund structure Robinhood chose. The fund’s initial management fee is being offered at a discounted rate through July 2026 as part of a contractual waiver to build early AUM.

BlackRock, Fidelity, and Charles Schwab have all been building retail-facing private market products for years, according to market reporting. The category is no longer a sideline project for these institutions.

What This Means for Wefunder, StartEngine, and Republic

The crowdfunding platforms and the institutional entrants are not, strictly speaking, selling the same product. Reg CF and Reg A+ offerings are typically early-stage companies — pre-revenue or early-revenue startups where an investor’s $500 or $5,000 goes directly to the company’s balance sheet. Robinhood’s RVI and JPMorgan’s private markets funds are secondary exposure vehicles investing in late-stage companies at valuations in the tens or hundreds of billions.

But from the perspective of a retail investor deciding where to allocate private market dollars, the category framing is increasingly the same: get access to growth companies before they go public. The pitch overlaps enough that platform traffic, investor attention, and brand credibility are now shared resources.

Kingscrowd’s 2026 outlook flagged the competitive pressure explicitly, noting that tokenization and “always-on” access from products like Robinhood’s tokenized equities in the EU, and Republic’s Mirror tokens, are pushing platforms to make private market exposure feel more like public market investing — more access, more liquidity narratives, more frequency.

The crowdfunding platforms have one structural advantage the institutional products cannot easily replicate: direct issuer relationships and deal flow at the company formation stage. A Wefunder or StartEngine campaign connects investors to a founder building something new, often in their own community or sector. RVI offers Databricks exposure. Those are different propositions for different investor psychology — but both are competing for a finite pool of retail risk capital.

WHAT TO WATCH NEXT

- RVI’s price vs. NAV. If Robinhood’s fund continues to trade at a steep discount to the net asset value of its holdings, it signals that retail investors remain skeptical of private valuations — which could dampen appetite for the category broadly, including crowdfunding.

- The $5M Reg CF cap. A pending SEC petition to raise the Reg CF limit from $5 million to $20 million per offering would dramatically change the competitive profile of crowdfunding platforms, allowing them to attract larger, later-stage companies that currently have no reason to use the exemption.

- Platform consolidation. StartEngine has diversified into secondary trading, tokenized assets, and international expansion — building higher-margin adjacencies that could justify a premium multiple or attract a strategic buyer. Watch whether the major platforms pursue M&A or a public listing of their own.

- Institutional distribution partnerships. If a Wefunder or Republic announces a distribution deal with a major wirehouse or RIA platform, that would signal the crowdfunding category is ready to compete with institutional products on their own turf.

- 2026 Reg CF volume. The first quarter of 2026 will indicate whether the 58% growth in 2025 represents a structural shift or a year driven by a handful of outsized raises like Newsmax and Pacaso.