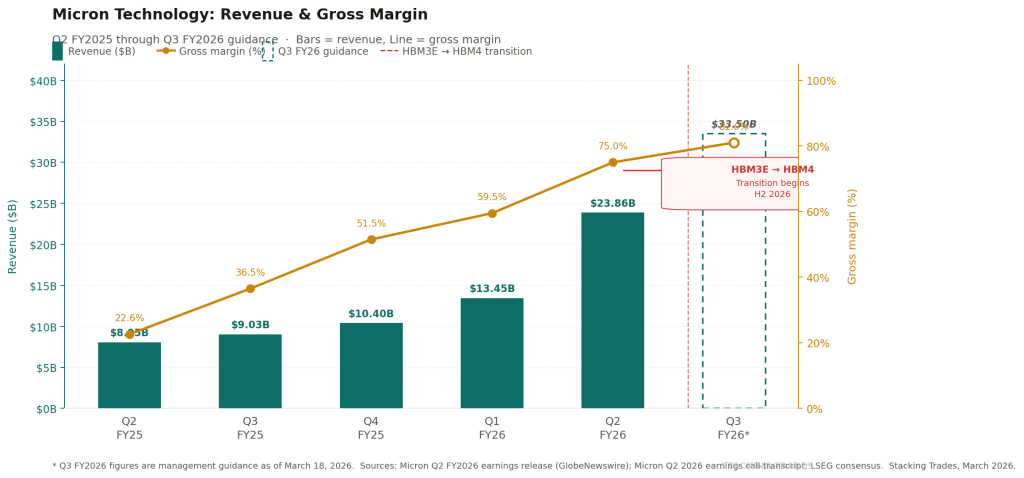

There is a version of Micron’s fiscal second quarter that sounds like the greatest corporate turnaround in semiconductor history. Revenue hit $23.86 billion — a 196% increase year-over-year and the fourth consecutive quarter of record results. Earnings per share came in at $12.20 adjusted, against analyst expectations of $9.31. Forward guidance projected Q3 revenue of $33.5 billion with gross margins approaching 81%.

Then the stock slipped.

Shares fell roughly 3.9% in the session following the report — a reaction that, on its face, makes no sense. But it makes complete sense once you understand what Micron has become and what investors are now being asked to price.

How Memory Became the Bottleneck for AI

To understand Micron’s quarter, you first need to understand why memory is no longer a commodity business. For most of its history, DRAM was treated like a bulk chemical — cyclical, price-sensitive, interchangeable between suppliers. The AI era has changed the physics of the problem.

Every Nvidia Blackwell B200 GPU requires six stacks of High Bandwidth Memory, totaling 192 gigabytes per chip. The upcoming Blackwell Ultra is expected to push that to eight stacks. And Nvidia’s next-generation Rubin architecture, announced at GTC 2026, will use HBM4 — a product still in early mass production qualification.

This is the supply chain reality that produced Micron’s numbers. Every business segment reported that higher pricing was the primary driver of revenue growth, while bit shipments were either flat or slightly down — a classic sign of a supply-constrained market. Micron did not sell dramatically more memory. It sold the same memory at dramatically higher prices, because its customers had no alternative and no leverage.

HBM capacity is sold out through 2026. That single fact is the entire bull case in one sentence.

The Numbers Behind the Numbers

Micron’s adjusted EPS of $12.20 beat analyst expectations by nearly 39% — a margin of surprise that is almost unheard of for a company this size. Operating cash flow reached $11.9 billion, up 202% year-over-year. Cash on hand stood at $13.9 billion.

Gross margin expanded from approximately 22.6% in fiscal Q2 2025 to 75% in fiscal Q2 2026 — an expansion driven almost entirely by the pricing premium attached to AI-grade HBM memory over traditional DRAM.

The automotive segment also quietly posted a record. Cloud, mobile, core data center, and automotive units each grew materially, reflecting both growing memory content in modern vehicles and the pricing premiums automakers pay to secure allocation in a constrained market. AI is pulling memory demand from every direction simultaneously — data centers, autonomous vehicles, edge devices — and Micron sits across all of it.

“In the AI era, memory has become a strategic asset for our customers, and we are investing in our global manufacturing footprint to support their growing demand.”

—Sanjay Mehrotra, Chairman, President and CEO, Micron Q2 FY2026 earnings release

Why the Stock Fell Anyway

The answer is $25 billion. Micron raised its fiscal 2026 capital expenditure budget to over $25 billion and warned that 2027 capex will see a meaningful step up to fund the construction of new fabrication plants in Idaho and New York.

That number frightened investors for two reasons. First, it raises the stakes on the demand thesis considerably — if AI infrastructure spending cools, Micron will be left holding enormous fixed costs and excess capacity built at the top of the cycle. Second, it echoes the setup of every previous memory boom, each of which ended in a supply glut and a brutal price correction.

The CHIPS Act adds another layer of uncertainty. Micron’s $25 billion capex is partially subsidized by $6.1 billion in direct CHIPS Act grants. But a recent policy shift under Commerce Secretary Howard Lutnick — exploring whether the government should take equity stakes in companies receiving large subsidies — has introduced regulatory ambiguity that the market is still working through.

Micron, Samsung, and SK Hynix are collectively spending over $58 billion on capex in 2026. At that scale of coordinated investment, the risk of overshooting demand is real — even if today’s demand picture looks unimpeachable.

The HBM4 Transition Is the Next Inflection

The shift to HBM4 in the second half of 2026 is expected to carry even higher average selling prices than current HBM3E products. In early 2026, Micron began volume shipments of its 36GB 12-Hi HBM4 modules for next-generation AI accelerators — a transition that could lead to more stable, long-term pricing arrangements rather than the spot-price volatility that has historically plagued the memory industry.

If that structural shift in pricing holds, it would represent a genuine re-rating of Micron’s business model — from cyclical commodity supplier to something closer to a strategic partner embedded in hyperscaler infrastructure roadmaps. That is the bull case that justifies the capex.

SK Hynix currently leads the HBM market with 62% share, Micron holds 21%, and Samsung trails at 17%. Samsung has resumed construction of its Pyeongtaek P5 fab and is positioning its sixth-generation DRAM process as a stepping stone to volume HBM4. If Samsung resolves its yield issues faster than expected, the combined output of all three giants could shift the supply picture materially by 2028.

WHAT TO WATCH NEXT

- HBM4 customer commitments. The transition to custom base dies means Micron will likely announce named hyperscaler partnerships for HBM4 supply. Any such announcement would confirm the pricing stability thesis and likely trigger significant upward estimate revisions.

- Q3 gross margin execution. Management guided 81% gross margins for Q3. Delivering on that number — while simultaneously ramping HBM4 production — would remove the market’s biggest near-term concern about execution risk.

- Samsung’s recovery timeline. Samsung currently holds roughly 17% of the HBM market and is fighting to regain its footing. If Samsung accelerates its HBM ramp faster than expected, it compresses Micron’s pricing power window.

- CHIPS Act equity provision. The question of whether future CHIPS funding will require government equity stakes is unresolved. Resolution in either direction removes uncertainty from Micron’s balance sheet planning.

- Nvidia Rubin launch timing. Rubin will use HBM4, with 16-Hi stacks targeting Q4 2026. Any delay in the Rubin ramp would push out HBM4 volume demand and affect Micron’s Q4 and fiscal 2027 revenue trajectory.