.jpg){kind=link}

For roughly two years, the central question in enterprise technology investing was whether AI would actually generate revenue, or whether it would remain a perpetual R&D story — impressive in demos, invisible in earnings. That question now has a clear answer. The harder question, the one that explains a $285 billion software sector selloff in early February and a Salesforce stock that fell 5% after the company reported the fastest quarterly revenue growth in two years, is what that revenue is actually worth.

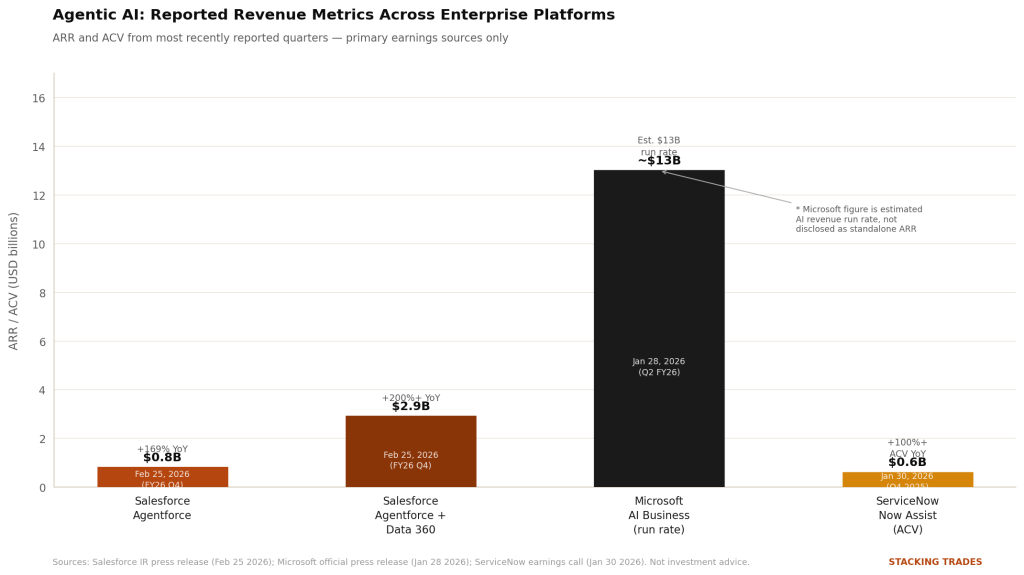

The revenue is not speculative. Salesforce reported that its Agentforce platform had reached $800 million in annual recurring revenue as of its fiscal Q4 close on January 31, 2026, up 169% year-over-year, with 29,000 total deals closed — a 50% jump quarter-over-quarter. Combined Agentforce and Data 360 ARR exceeded $2.9 billion, more than doubling in a year. Microsoft’s AI business reached an annualized run rate approaching $13 billion as of its Q2 FY2026 results, with Azure growing 39% year-over-year and AI products cited as a primary driver. ServiceNow disclosed that its Now Assist agentic AI product surpassed $600 million in annual contract value, with net new ACV more than doubling year-over-year in Q4 2025, and management targeting over $1 billion in Now Assist ACV for 2026.

None of those numbers are projections. They are reported figures from primary earnings releases and official transcripts. The problem is not that investors don’t believe the revenue. It is that the frameworks traditionally used to value enterprise software — ARR multiples, seat counts, net revenue retention — were built for a model that agentic AI is actively dismantling.

What Agentic AI Actually Does to the Per-Seat Model

The SaaS era ran on a simple, elegant assumption: more employees meant more software subscriptions. A company with 500 salespeople needed 500 CRM seats. A company with 200 support agents needed 200 helpdesk licenses. Revenue expanded with headcount, multiples compressed around that predictability, and the entire asset class was priced accordingly. Salesforce, Workday, ServiceNow, and their peers collectively built hundreds of billions of dollars in market value on that formula.

Agentic AI severs the link between headcount and software spending. An AI agent that autonomously handles customer support tickets, drafts sales outreach, or manages IT workflows does not consume a human seat. It replaces several. The enterprise does not stop paying for software — in many cases it pays more, because agents that deliver measurable business outcomes command higher prices than productivity tools — but the unit of pricing has to change. Consumption-based models, outcome-based contracts, and flat-fee agentic enterprise licenses are all competing to fill the gap that per-seat pricing is leaving behind.

AlixPartners projected in its 2026 enterprise software report that usage- and outcome-based models will account for over 40% of AI software revenue by the end of this year, with AI-native companies commanding valuations roughly five to six times higher than their SaaS-era peers. The same report noted that ARR multiples, historically the dominant valuation method for enterprise software, are projected to explain significantly less of valuations as investors grapple with the costs and structural differences of AI delivery. The framework is not broken — it is simply incomplete.

The February Selloff Was a Pricing Argument, Not an Earnings Crisis

On February 3, 2026, the enterprise software sector erased roughly $285 billion in market capitalization in a single session, in what analysts quickly labeled the “SaaSpocalypse.” The proximate trigger was a cluster of agentic AI product launches — including autonomous agent tools capable of operating enterprise software interfaces directly — which prompted investors to reprice the seat-compression risk that had been a theoretical concern since 2024. Workday, ServiceNow, Salesforce, and Adobe all saw significant intraday declines despite reporting strong earnings in the weeks prior.

What made the selloff instructive was what it revealed about the valuation gap. Salesforce’s Q4 report, released February 25, beat expectations handily — Q4 revenue of $11.2 billion, up 12% year-over-year; adjusted EPS of $3.81 against a consensus estimate of $3.05; Agentforce growing at triple-digit rates. The stock still fell roughly 5% in after-hours trading. Bernstein maintained an underperform rating, citing what it called “a mature business in a mature market.” Goldman Sachs retained a buy, emphasizing that differentiated outcomes with Agentforce would be the key driver. The disagreement was not about the Q4 numbers. It was about whether the transition from per-seat revenue to outcome-based revenue would expand or compress total addressable market and long-term margin profiles — a question that a quarterly earnings release cannot fully answer.

“We’ve rebuilt Salesforce to become the operating system for the Agentic Enterprise. Agentic AI is a tailwind for our business, and we’re well on our way to $63 billion in revenue in FY30.”

— Marc Benioff, Chair and CEO, Salesforce, Q4 FY2026 Earnings Release, February 25, 2026

Microsoft’s Conversion Problem Complicates the Narrative

Microsoft’s AI story is structurally different from Salesforce’s, and that difference matters for how investors should read the valuation debate. Azure’s AI workload growth is unambiguous — 39% year-over-year, with AI contributing an estimated 13 to 16 percentage points of that growth rate. The commercial remaining performance obligation reached $625 billion as of Q2 FY2026, up 110% year-over-year, with roughly 45% of that driven by OpenAI commitments. By any infrastructure measure, demand is real and contracted.

The consumer-facing product story is more complicated. After eight consecutive quarters of declining to disclose a seat count, Microsoft finally confirmed in its January 28 earnings call that Microsoft 365 Copilot had 15 million paid seats — representing 3.3% of the 450 million commercial Microsoft 365 users. Growth was strong, up more than 160% year-over-year, but the absolute penetration rate raised questions about whether the flagship AI product was converting as quickly as the infrastructure investment required. Independent survey data from Recon Analytics found Copilot’s share of the paid AI subscriber market had dropped from 18.8% to 11.5% in the six months through January 2026, even as total paid seats grew.

CFO Amy Hood’s response on the earnings call was notable. She argued that judging AI spend solely on Azure or Copilot revenue “is the wrong yardstick” — that the infrastructure creates competitive positioning across Microsoft’s entire business that no single revenue metric can capture. That framing has merit. It is also the kind of argument that buys time while adoption numbers catch up. At a $150 billion annualized capital expenditure run rate — unprecedented in corporate history — the return horizon matters.

The Metrics That Actually Matter Now

For investors trying to evaluate enterprise AI companies with available frameworks, three signals from the current earnings cycle are worth tracking more carefully than headline revenue growth. The first is the ratio of new bookings coming from existing customer expansion versus new logos. Salesforce disclosed that more than 60% of Agentforce and Data 360 Q4 bookings came from existing customers expanding their commitments — a land-and-expand dynamic that suggests genuine deployment rather than trial-stage procurement. That pattern is harder to fake than a logo count.

The second is token and workflow volume as a proxy for production deployment versus sandbox testing. Salesforce’s disclosure that its platform processed nearly 20 trillion tokens cumulatively and delivered 2.4 billion agentic work units — tasks where AI was not reasoning but completing — is precisely this kind of metric. A customer processing tokens at scale is a customer with agents in production, which is a customer whose renewal probability is structurally higher than one still evaluating.

The third, flagged explicitly in PwC’s February 2026 analysis of AI’s impact on software valuations, is gross revenue retention disaggregated from net revenue retention. In a world where AI agents are reducing seat counts while AI add-ons are increasing per-account spending, NRR can look healthy while the underlying seat base is contracting. GRR stripped of AI upsell reveals whether the core product is holding or eroding — and that separation is the most direct test of how durable any given platform’s moat actually is.

The companies that have the clearest answers to those three questions — expansion ratios, production deployment evidence, and clean retention disaggregation — are the ones most likely to survive the valuation reset with multiples intact. The ones that can only point to ARR growth rates without that supporting evidence are the ones the market is right to reprice, regardless of how impressive the headline number looks.

WHAT TO WATCH NEXT

- Salesforce FY2027 Q1 earnings — the first quarter under new guidance; management committed to organic revenue re-acceleration in H2 FY27, and Q1 results will show whether early momentum supports that trajectory or reveals a gap between Agentforce deal closings and recognized revenue.

- Microsoft Q3 FY2026 earnings (expected April 29) — Azure guidance of 37–38% growth was provided for the quarter; any miss or commentary on capacity constraints will directly affect how the market prices AI infrastructure demand. The Copilot paid-seat trajectory will also be updated for the first time since the January disclosure.

- ServiceNow’s path to $1 billion in Now Assist ACV — management stated a clear target for 2026; quarterly progress reports will be the most specific test of whether enterprise agentic AI contracts are scaling as predicted or plateauing after early adopters.

- The pricing model transition — Salesforce’s Agentic Enterprise License Agreement, described as a flat-fee “all you can eat” structure for customers ready to scale, is the clearest real-world test of whether enterprises will pay more per account under outcome-based pricing than they did under per-seat models. Deal size data from quarterly reports will show whether the math works.

- The AlixPartners prediction on valuation frameworks — the consulting firm projected that hybrid AI leverage ratio models will begin replacing pure ARR multiples as the standard for enterprise software valuation by end of 2026. Watch for the first major analyst firm to publish a formal framework shift; that moment will likely move sector multiples.