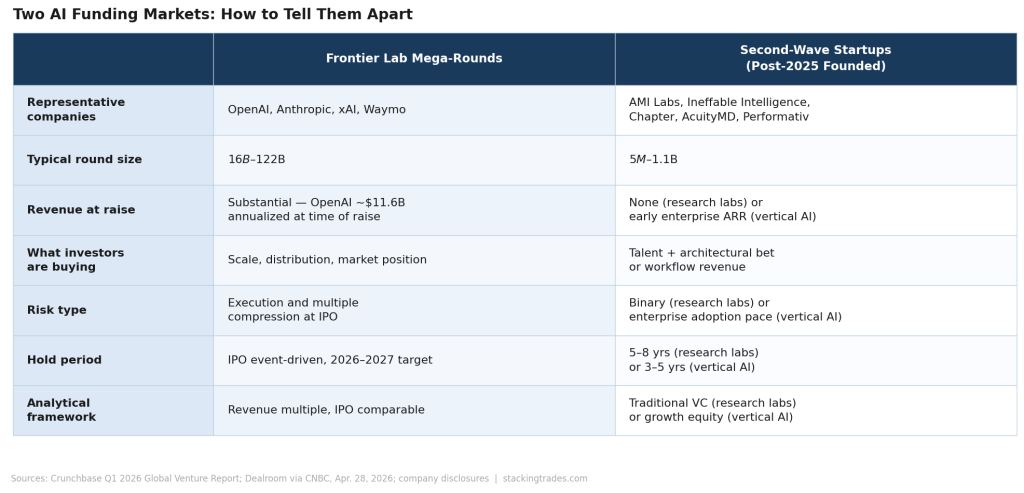

The headline number from Q1 2026 has been told many times: $300 billion in global venture investment, 80% of it flowing to AI, four of the five largest venture rounds in history closing in a single quarter. OpenAI raised $122 billion. Anthropic raised $30 billion. xAI raised $20 billion. Waymo raised $16 billion. Those four deals alone account for $188 billion — nearly 65% of everything invested globally in the quarter.

That story is well-covered. The one running alongside it is not.

According to Dealroom data cited by CNBC in late April, venture capitalists have already funneled $18.8 billion in 2026 into AI startups founded since the start of 2025. That figure is tracking ahead of the $27.9 billion raised by similarly new companies across all of 2025. A parallel funding market is running — smaller in absolute terms, structurally different in almost every other way, and increasingly relevant to investors trying to find returns that don’t require getting into a $1 trillion IPO at the ground floor.

What the Frontier Labs Left on the Table

The concentration of capital at the top of the AI stack has a predictable side effect. When the largest labs compete to release the best frontier model on the shortest cycle, large areas of applied research get deprioritized — not because they lack value, but because they don’t move benchmark scores or win press cycles. That creates an opening.

“When you’re in a race, you narrow focus. That creates a vacuum. Entire areas of research, like new architectures, agents, interpretability and vertical models, are being deprioritised, not because they don’t matter, but because they don’t win the immediate race.”

— Elise Stern, Managing Director, Eurazeo, speaking to CNBC, April 28, 2026

Eurazeo backed AMI Labs, the Paris-based startup founded by Yann LeCun after he left his role as Meta’s chief AI scientist. AMI Labs raised $1.03 billion in a seed round — from Bezos Expeditions, Nvidia, and Samsung — focused on AI systems that understand the physical world, maintain long-term memory, and handle complex reasoning in real-world settings. That is precisely the territory the frontier labs have had least incentive to develop aggressively while the benchmark arms race for text and multimodal generation remains the primary commercial and reputational priority.

AMI Labs is not alone. Former Google DeepMind reinforcement learning researcher David Silver announced a $1.1 billion seed round for Ineffable Intelligence in late April. Another ex-DeepMind researcher, Tim Rocktäschel, is reported to be raising up to $1 billion for Recursive Superintelligence, which focuses on continuous learning architectures. Recursive Intelligence — co-founded by former Anthropic and Google DeepMind researchers Anna Goldie and Azalia Mirhoseini — raised $335 million across two rounds after launching in September 2025, focused on AI tools for chip design. These are seed-stage investments. Most of these companies have no product and no revenue. Investors are paying for the talent, the insight into what the frontier labs are not doing, and the architectural bets that may not produce returns for years.

The More Investable Side of This Wave

The billion-dollar seed rounds capture attention, but they are the thinnest part of the $18.8 billion figure to underwrite. The more instructive pattern — and the more relevant one for sophisticated investors evaluating private market exposure — is what is happening in the application layer, where companies founded since 2025 are raising at Series A and B on the strength of real enterprise revenue rather than researcher pedigree.

The vertical AI thesis has moved from pitch deck to commercial reality in several regulated sectors. Chapter, an AI platform for Medicare advisory, raised $100 million in April 2026 to scale into one of the most structurally complex and high-willingness-to-pay environments in U.S. healthcare. AcuityMD, a commercial intelligence platform for medical device manufacturers, raised $80 million in a Series C led by StepStone Group — notable because the lead is a large institutional alternative asset manager rather than a traditional venture firm, signaling that private markets capital is following AI revenue into medtech sales infrastructure. In fintech, the pattern is consistent: Performativ raised €5.5 million for an AI-native operating system for wealth management; Marloo raised $10 million for financial adviser workflow tools. These are not demo-stage companies. They are solving compliance-heavy operational problems that enterprise buyers have budget to fix.

The common thread is workflow ownership. Vertical AI companies that sit inside a daily operational workflow — not alongside it as an assistant, but embedded in the process itself — generate the retention and expansion economics that justify enterprise software multiples. A Medicare advisory platform that improves by learning from every case it handles is harder to displace than a chatbot wrapper. A commercial intelligence platform that integrates into a sales team’s daily motion builds switching costs over time. The investors writing the larger checks in the second wave are distinguishing between these two categories sharply.

The Dependency the Second Wave Cannot Ignore

The structural question that sits beneath all of this is how closely the second wave’s returns are correlated with the first wave’s success. The application-layer companies building on top of frontier models are, to varying degrees, dependent on the pricing, availability, and capability trajectory of the underlying infrastructure they use. An agentic healthcare platform built on a foundation model faces a different risk profile in 2028 if that model’s provider has repriced API access post-IPO, or if a better-performing open-source alternative has compressed the incumbent’s moat.

That dependency runs both ways. The $300 billion Q1 investment wave was premised partly on enterprise adoption accelerating as fast as the private market assumes. The vertical AI companies now raising at Series A and B on real revenue are the clearest available evidence for whether that assumption is correct. If Chapter’s Medicare platform scales, if AcuityMD’s medtech customers renew and expand, if Performativ’s wealth management operating system crosses into institutional distribution — those outcomes provide the revenue substance that the frontier lab valuations require to be justified from below. The second wave and the first wave need each other, even when they are funded by different parts of the market on different timelines.

What Sophisticated Investors Are Actually Pricing

The $18.8 billion flowing into post-2025 AI startups is not homogeneous. The billion-dollar seed rounds for researcher-founded labs are effectively long-dated bets on architectural approaches that may or may not produce commercial products in the next three to five years. They are venture capital in its purest form — high conviction, long horizon, binary outcomes. The Series A and B rounds for vertical AI companies with paying enterprise customers are something closer to growth equity underwriting: the product works, the market is real, the question is execution at scale.

Investors who conflate these two categories — treating all $18.8 billion as a uniform signal about AI startup health — will draw the wrong conclusions in both directions. The researcher-pedigree seed rounds tell you something about where the frontier labs are not competing. The vertical AI revenue rounds tell you something about where enterprise AI spending is actually landing. Both signals matter. They require different analytical frameworks, different hold periods, and different risk tolerances. The fact that they are both being described as the “second wave” of AI funding is a convenience, not a thesis.

What to Watch Next

- First revenue disclosures from the billion-dollar seed labs. AMI Labs, Ineffable Intelligence, and Recursive Superintelligence have no disclosed revenue. When any of them announces a first commercial product or a named enterprise customer, it will be the first data point separating architectural ambition from commercial execution.

- Series B conversion rates for 2025-founded vertical AI companies. The cohort that raised Series A rounds in 2025 on early enterprise traction is now entering its Series B window. How many convert — and at what valuation step-up — will establish whether the vertical AI revenue thesis is compounding or plateauing after early adopter saturation.

- Foundation model API pricing post-IPO. OpenAI’s S-1 filing process will eventually disclose its API cost structure. Any post-IPO repricing of inference access changes the margin math for every application-layer company built on top of it and may accelerate the shift toward open-source model deployment among enterprise buyers.

- Enterprise AI renewal data in Q2 and Q3 earnings. The hyperscalers’ Q1 results confirmed that AI infrastructure spend is accelerating. The more important signal — whether enterprise software buyers are renewing, expanding, and deepening their vertical AI deployments — will start surfacing in midmarket SaaS earnings through the summer.

- Yann LeCun’s first AMI Labs product announcement. LeCun’s specific focus on grounding, causality, and physical-world reasoning represents a direct architectural critique of the current transformer-dominant paradigm. The first public demonstration of whether that critique produces a commercially usable system will be one of the more consequential AI product announcements of the year.