{kind=link}

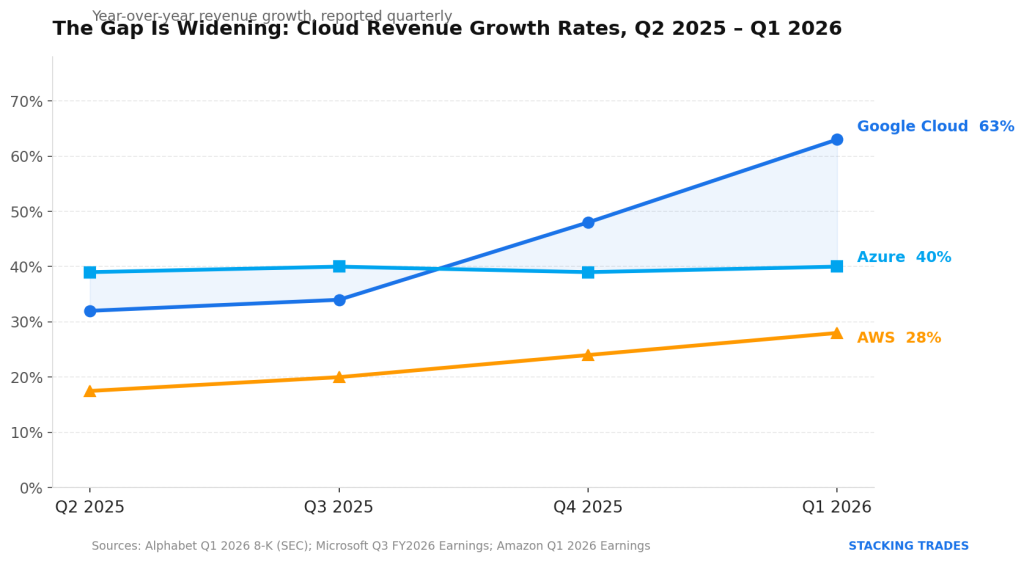

Google Cloud just posted its strongest growth quarter in years — 63% year-over-year, crossing $20 billion in revenue for the first time — while Azure grew 40% and AWS grew 28%. That gap is new. For most of the past three years, the three hyperscalers ran within a tighter band. Something has changed, and the question investors need to answer is whether Google’s acceleration is pulling spend away from its competitors or simply capturing its share of an expanding market.

The distinction matters enormously. If Gemini is growing by adding net-new enterprise AI workloads that didn’t previously exist on any cloud, that’s a rising-tide story. If it’s growing by displacing OpenAI-dependent Azure deployments, that’s a zero-sum story — with different implications for Microsoft investors, for OpenAI’s pre-IPO valuation, and for how the enterprise AI market ultimately settles.

The Backlog Is the More Important Number

The revenue figure is already history. The more forward-looking signal is the backlog. Google Cloud’s remaining performance obligations — contracted future revenue — nearly doubled quarter-over-quarter to $462 billion. That is not a forecast. It is money already committed by customers who have signed multi-year agreements and haven’t yet drawn it down. At the current quarterly revenue run rate, it represents roughly five years of cloud spending already on the books.

CFO Anat Ashkenazi told analysts that Alphabet expects to convert just over 50% of that backlog within the next 24 months. That timeline creates a visible revenue floor through at least mid-2028 — before a single new contract is signed. It also means Google Cloud’s growth rate is increasingly underwritten by existing commitments rather than by the volatile process of winning new customers every quarter.

The Full-Stack Argument Is Starting to Win Real Deals

The structural case Google Cloud has been making for two years — that owning the model, the silicon, and the infrastructure removes the friction and licensing costs its competitors absorb — is now producing named enterprise commitments. KPMG deployed Gemini Enterprise to its 55,000 U.S. professionals and had nearly 90% of employees actively using the platform within two weeks of launch. Valeo is rolling out Gemini for Workspace to its entire 100,000-person global workforce. These are not pilots. They are organizational commitments that are difficult and expensive to reverse.

The KPMG decision is particularly informative because it was a competitive evaluation. According to commentary from KPMG’s own technology leadership, Google won because it offered the integrated stack — models, infrastructure, and an agent-building platform — rather than requiring the firm to assemble components from multiple vendors. That is the same argument Google Cloud CEO Thomas Kurian has made at every major conference for two years. It is now appearing in actual customer-selection rationales.

“We are compute constrained in the near term. Our cloud revenue would have been higher if we were able to meet the demand.”<

— Sundar Pichai, CEO, Alphabet, Q1 2026 Earnings Call, April 29, 2026

The Supply Constraint Is a Bullish Signal Wearing a Bearish Costume

Pichai’s admission that compute constraints capped Q1 revenue would normally be read as a cautionary note. In this context, it functions differently. A company saying it couldn’t serve all the demand it had is not describing a demand problem — it is describing a supply problem on the way to a larger revenue base. Alphabet raised full-year 2026 capital expenditure guidance to $180–$190 billion and flagged that 2027 capex will increase significantly again. That is not how management teams respond to fragile demand signals.

The token throughput figures confirm the demand picture. Google’s first-party models processed 16 billion tokens per minute through direct customer APIs in Q1, up 60% from the prior quarter. That is production traffic, not development or testing. It represents real enterprise workloads running in production that require ongoing capacity. The 330 Cloud customers who each processed over one trillion tokens in the trailing 12 months are embedded deeply enough that switching costs are now a structural factor in any competitive analysis.

Net New or Displacement: The Question the Data Can’t Yet Answer

Azure grew at 40% in the same quarter — exceptional by any historical standard. AWS grew 28%. None of these numbers suggest the others are losing. What they suggest is that total enterprise AI spending is expanding fast enough to let all three accelerate simultaneously while still producing a meaningful gap at the top. The multi-cloud adoption rate among enterprises — now above 89% — is consistent with this: most organizations are not choosing a single provider. They are spreading workloads across the infrastructure they trust for each specific use case.

The harder question is whether Google’s growth rate implies share gains specifically in the workloads where Azure has structural advantage — the Microsoft 365 ecosystem and the OpenAI model access that comes bundled into enterprise agreements. Azure’s exclusive OpenAI partnership has been its most defensible moat in enterprise sales. Google Cloud Next’s announcement of the Gemini Enterprise Agent Platform — which includes third-party models including Anthropic’s Claude alongside Gemini — is a direct attempt to neutralize the moat-through-model-access argument. If customers can run Claude on Google Cloud without going to Azure, the OpenAI-Azure bundling advantage narrows.

What the Margin Trajectory Tells Long-Term Holders

Google Cloud’s operating margin reached 32.9% in Q1 2026, up from near zero in 2022. Ashkenazi noted that the Wiz acquisition, which closed in March, will create a low single-digit percentage-point headwind to cloud margins for the remainder of 2026. That compression is temporary and explicable. The underlying margin trajectory — from a division that was losing money three years ago to one generating meaningful operating income on $80 billion in annualized revenue — is the more important signal for investors modeling Alphabet’s long-term earnings power.

The bears on Alphabet have spent two years worried that AI would erode Search. Instead, Search queries hit an all-time high in Q1, AI Overviews are monetizing at rates comparable to traditional Search, and Google Cloud is now the division generating the most investor excitement. The company that was supposed to be disrupted by the AI cycle has, through one quarter’s data, positioned itself as one of the clearest beneficiaries of it. Whether that holds through the back half of 2026 depends almost entirely on how fast Alphabet can build its way out of the supply constraint Pichai described on the earnings call.

What to Watch Next

- Google Cloud Q2 2026 results and backlog conversion pace. Ashkenazi committed to converting just over 50% of the $462 billion backlog within 24 months. Any quarterly disclosure showing conversion slowing would be the first real crack in the bull case. Acceleration would extend it.

- Azure Q4 FY2026 results and OpenAI model access commentary. If Microsoft discloses that OpenAI integration is driving net-new enterprise logos rather than deepening existing relationships, it strengthens the case that the two platforms are competing for distinct workloads rather than the same budget lines.

- Capex execution against the $180–$190 billion 2026 guidance. The supply constraint Pichai described is only resolved by infrastructure. Watch for sequential improvement in compute availability commentary and any revision to the full-year spending range that signals demand is outrunning the build plan.

- Enterprise renewal and expansion data from Gemini Enterprise’s early large-scale deployments. KPMG and Valeo are the reference deployments Google points to in sales conversations. Whether those organizations expand seat counts or deepen agent usage in subsequent quarters is the earliest available signal on whether the full-stack argument holds post-adoption.

- Any formal OpenAI or Anthropic commentary on Google Cloud as an infrastructure host. Both companies’ models are available on the Gemini Enterprise Agent Platform. If either discloses a meaningful volume of API traffic running through Google Cloud infrastructure, the competitive map shifts significantly.