Nvidia entered full production on Vera Rubin on June 1, 2026 — months ahead of where most of the industry had penciled it in. The platform ships to an initial cohort of AWS, Google Cloud, Microsoft Azure, Oracle Cloud, CoreWeave, Lambda, Nebius, and Nscale in the second half of this year. Everyone else waits until 2027. That gap between who is in the first deployment cohort and who is not is the most consequential supply decision in the AI infrastructure cycle right now.

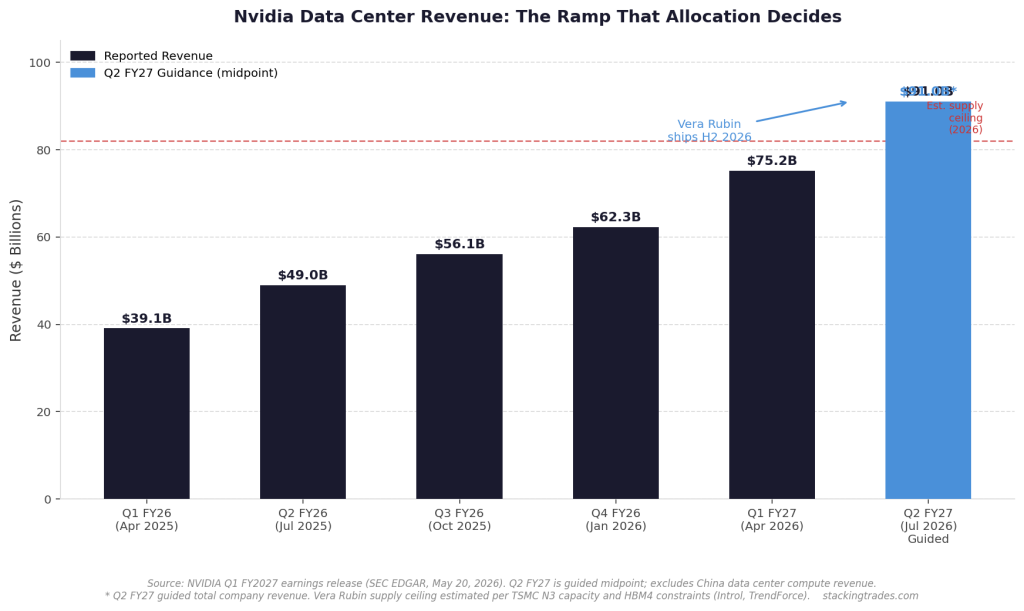

The problem is not demand. Jensen Huang told analysts on the May 20 earnings call that Nvidia sees at least $1 trillion in combined Blackwell and Vera Rubin demand through 2027 — double the $500 billion figure he cited at GTC 2025 a year earlier. The problem is physics. Vera Rubin’s production ceiling for 2026 is estimated at 200,000 to 300,000 GPUs, constrained by TSMC’s N3 advanced packaging capacity and HBM4 supply from SK Hynix and Samsung. When total committed demand is measured in trillions and annual output is measured in hundreds of thousands of units, allocation becomes the competitive variable that matters most.

“My sense is that we’ll be supply constrained throughout the entire life of Vera Rubin.”

— Jensen Huang, CEO, NVIDIA, Q1 FY2027 Earnings Call, May 20, 2026

What Vera Rubin Actually Is — and Why the Architecture Matters for Allocation

Vera Rubin is not a chip. It is a complete rack-scale platform integrating seven different chip types into five purpose-built rack configurations that Nvidia describes as operating as a single AI supercomputer. The flagship NVL72 rack packs 72 Rubin GPUs and 36 Vera CPUs, connected through NVLink 6 at 260 terabytes per second of aggregate bandwidth. The system runs entirely on liquid cooling — there is no air-cooled variant — and on 800-volt DC power architecture, a departure from the 48-volt standard most existing data centers were built around. Both of those infrastructure requirements add 12 to 18 months of lead time for facilities that need to retrofit.

The performance numbers relative to Blackwell are meaningful enough that no serious AI infrastructure buyer can afford to stay on the prior generation indefinitely. Nvidia claims 10x inference per watt and 10x lower cost per token compared to Grace Blackwell. Independent analysis from SemiAnalysis validated the prior generation’s claims and actually exceeded them — Hopper-to-Blackwell delivered 50x performance per watt, against Nvidia’s stated 35x figure. If the same pattern holds for Vera Rubin, the performance gap between first-cohort customers and those waiting until 2027 will be larger than the official specs suggest.

The Allocation Queue and Who Controls It

Nvidia allocates GPU systems based on committed purchase volumes, typically 6 to 12 months before delivery. Organizations not already in the procurement pipeline for Vera Rubin as of mid-2026 are looking at 2027 availability at the earliest. That is not a logistics problem — it is a competitive moat problem. Hyperscalers that secured early allocation commitments can build and price inference capacity that smaller AI clouds and enterprise buyers simply cannot access yet. The first-cohort advantage compounds with time because the customers who get Vera Rubin earliest are the ones best positioned to attract the workloads that require it.

The concentration of early allocation among the largest players is not accidental. Nvidia’s Q1 FY2027 results showed that data center revenue split nearly evenly between hyperscale customers and what the company now calls ACIE — AI clouds, industrial, and enterprise. Hyperscale contributed roughly $38 billion; ACIE came in at $37 billion, up 31% sequentially. The widening of the customer base is real, but the widening of the supply queue is real too. As the hyperscaler capex commitments approaching $700 billion this year suggest, the largest buyers are not slowing their procurement — they are accelerating it, which compresses the supply available to everyone else.

Two Bottlenecks That Outlast the Launch

The binding constraints on Vera Rubin output are not demand-related and they are not going away quickly. The first is TSMC’s N3 process capacity. Vera Rubin’s GPU die runs on TSMC’s 3-nanometer node, which also serves Apple’s latest processors and AMD’s MI400 series. Nvidia has secured long-term capacity agreements, but the production ceiling is what it is. TSMC reported Q1 2026 revenue of $35.9 billion, with its 3-nanometer node accounting for 25% of total wafer revenue — already the highest-demand process in its portfolio. Meaningful capacity expansion takes years, not quarters.

The second bottleneck is HBM4 memory. Each Rubin GPU requires 288 gigabytes of HBM4 — roughly six times the memory per device compared to consumer GPUs. SK Hynix and Samsung began HBM4 mass production in Q4 2025, but yields remain below mature HBM3e levels, creating a supply curve that is separate from and slower-moving than the GPU production ramp itself. Nvidia halted production of China-bound H200 chips earlier this year and redirected TSMC capacity to Vera Rubin, which removes one source of demand pressure on the fab — but not on HBM. GPU systems equipped with HBM4 will have constrained availability for the first 12 to 18 months after launch. The math on that timeline puts broad availability in late 2027 or early 2028.

The Revenue Signal Investors Are Watching

Nvidia guided Q2 FY2027 revenue to $91 billion, a 12% sequential increase from a record Q1. That guidance assumes zero data center compute revenue from China — a floor, not a ceiling, if export restrictions were to change. CFO Colette Kress said on the earnings call that Nvidia aims to become the world’s leading CPU supplier, and that the new Vera CPU opens a $200 billion addressable market, with $20 billion in standalone CPU revenue expected this fiscal year alone. The Vera CPU’s four deployment configurations — paired with Rubin, standalone, with ConnectX-9 for storage, and with ConnectX-9 for confidential computing — give Nvidia a way to extract multiple revenue streams from a single piece of silicon.

The stock’s 5% drop in the session following the print reflected a market that had bid the expectations high enough that a record quarter required an extraordinary beat to produce a positive reaction. The underlying business dynamic, however, is unambiguous: Nvidia captures approximately 57 cents of every dollar hyperscalers spend on AI compute, and Vera Rubin’s ramp is expected to be faster than Blackwell’s, which was itself the fastest in the company’s history. Huang said on the earnings call that every frontier model company that skipped early Blackwell adoption will move directly to Vera Rubin from the start. That is not a prediction — it is a booking pattern that is already reflected in the order books.

What This Means for the Companies Behind the First Cohort

For investors tracking the AI infrastructure cycle, the Vera Rubin allocation story has a specific downstream implication: the inference capacity advantage that first-cohort customers build in H2 2026 will not be easily replicable by later entrants. CoreWeave, which has committed to scaling beyond 5 gigawatts of AI factory capacity with Nvidia by 2030, is positioned to offer Vera Rubin inference to enterprise customers who cannot build their own data centers. That creates a competitive dynamic between the hyperscale clouds and the AI-native infrastructure players that will become clearer as deployment data from H2 2026 surfaces in earnings commentary.

The Vera Rubin supply wall is also the upstream variable that determines downstream outcomes for companies that have built their products and pricing assumptions on a specific compute cost trajectory. Fireworks AI, which recently raised at a reported $15 billion valuation on the back of 416% ARR growth, competes on inference performance and cost. So does every other inference provider in the stack. The question of who gets Vera Rubin capacity, and when, is not a chip story. It is a business model story with a two-year tail.

What to Watch Next

- Nvidia Q2 FY2027 earnings, late August. The $91 billion guided midpoint is the first quarter where Vera Rubin revenue should begin to appear in the data center line. Watch for any split between Blackwell and Vera Rubin volume, and whether Colette Kress updates the $20 billion Vera CPU standalone revenue figure for the full year.

- Hyperscaler earnings in late July. Google Cloud, AWS, and Azure will all report Q2 results in the last week of July. Any commentary specifically referencing Vera Rubin deployment timelines or capacity availability will be the first external confirmation of how the allocation is actually converting into usable infrastructure.

- HBM4 yield improvement data from SK Hynix and Samsung. Both companies’ H2 2026 earnings calls will include memory pricing and volume commentary. Any acceleration in HBM4 yield maturation shifts the production ceiling estimate upward and could pull enterprise availability into late 2026 rather than 2027.

- AMD Helios shipments and enterprise reception. AMD’s first rack-scale system is expected to begin shipping in H2 2026. Its pricing, performance, and initial customer adoption will be the first real-world test of whether Vera Rubin’s supply constraint opens a durable window for competing platforms — or whether buyers simply wait in queue rather than switch architectures.

- TSMC N3 capacity expansion milestones. Any formal announcement from TSMC on expanding 3-nanometer output in the 2027 timeframe will directly affect how long the Vera Rubin supply wall holds. Given that TSMC’s 3nm node already represents 25% of its total wafer revenue and is still described as sold out, the expansion timeline is the longest-lead variable in the entire supply chain.