SpaceX priced at $135 per share on June 11, opened at $150 on June 12, and closed its first day at $160.95 — a 19% gain over the offer price that valued the company above $2 trillion. By June 16, the stock had traded as high as $225.64. As of June 22, it sits around $165. None of those numbers is the number that matters most for private market investors. The number that matters is the spread between what they paid before the IPO and what the public market has now confirmed.

That spread is large in some cases, deeply negative in others, and in at least one structure — Republic’s Mirror Token — the payout mechanics are still working through their first real test at scale. The SpaceX IPO did not just create a new public company. It created a simultaneous mark-to-market event for an entire ecosystem of vehicles, instruments, and funds that had been pricing SpaceX in the dark for years. The verdict is not uniform, and the implications run directly into the next wave of AI company listings that follows.

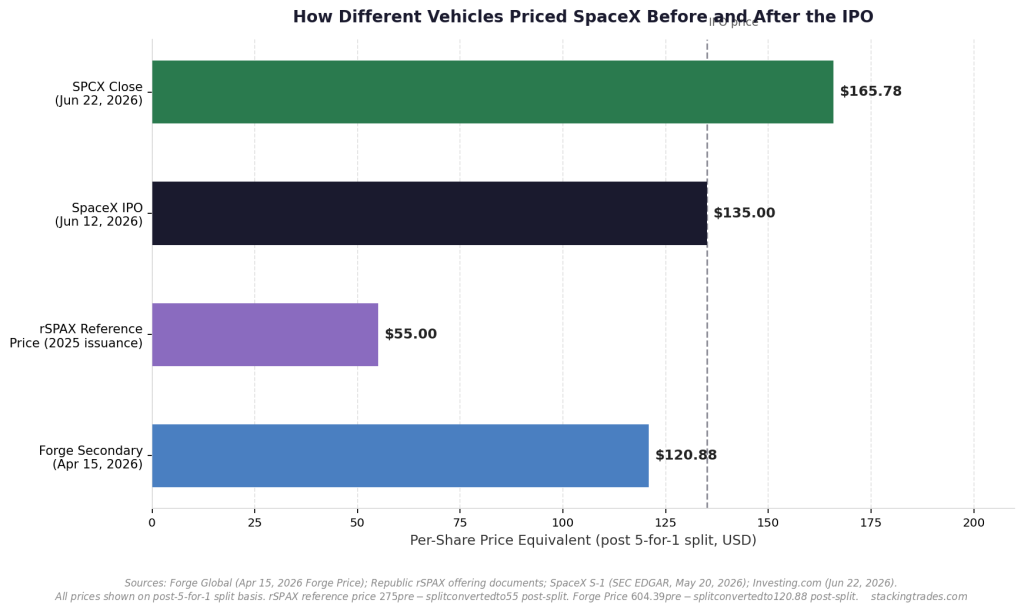

How the Secondary Market Got SpaceX’s Price Wrong — In Both Directions

Before the IPO, the main secondary platforms were pricing SpaceX at very different levels depending on their methodology and timing. Forge Global’s proprietary Forge Price, which incorporates primary funding round data and secondary market transactions, stood at $604.39 per share as of April 15 — on a pre-split basis, equivalent to roughly $120.88 per share after SpaceX’s 5-for-1 split in May 2026. The IPO priced above that at $135. The current market price is higher still. For secondary holders who transacted through Forge in the months before the offering, the public market arrived as a validation — their marks were directionally right, if not precisely calibrated to the final offer price.

Republic’s rSPAX Mirror Token tells a different story. The reference price for the initial rSPAX issuance was set at $275 per share on a pre-split basis — equivalent to $55 post-split. The IPO price of $135 is more than double that reference price. Under the Mirror Token’s payout formula, investors who bought rSPAX at the $275 reference price are entitled to a payout proportionally larger than their original investment, since the qualifying liquidity event value exceeded the reference. That is a good outcome for those holders. But the mechanics of actually executing that payout at scale — in USD or USDC through RepublicX’s wallet infrastructure — have not been tested at anything like this volume before.

The DXYZ Problem: When the Wrapper Trades at a Premium to a Company That Is Now Public

Destiny Tech100 (NYSE: DXYZ) is the most visible example of a structure that was built for a world where SpaceX was private. The closed-end fund reported a net asset value of $24.56 per share as of March 31, 2026, while trading in the $50 to $65 range on the open market — a premium to NAV of roughly 100% to 165%. SpaceX represented approximately 16.2% of the fund’s portfolio at that point. The fund’s purpose was to give retail investors access to private companies they could not otherwise reach. Once SpaceX began trading as SPCX, that access argument collapsed for its largest holding.

The closed-end structure means DXYZ cannot immediately sell its SpaceX position. Like all pre-IPO holders, the fund is subject to lock-up provisions that govern when shares can be sold. SpaceX’s tiered lock-up schedule allows eligible holders to sell 20% of their locked shares after the first quarterly earnings report — expected around September — with additional tranches releasing at 70, 90, 105, 120, and 135 days post-IPO. The fund filed plans to sell up to $1 billion in stock through an at-the-market program, but that was its own shares, not the underlying SpaceX position. The gap between what investors were paying for DXYZ and what the NAV actually supports — always a risk with closed-end funds trading at a premium — became considerably more visible once the underlying asset acquired a daily public price.

“This is a big step forward on our quest to make the private markets more accessible and liquid — globally. By combining regulation and blockchain innovation, we’re unlocking a future where anyone, anywhere, can invest in the companies shaping our world.”

— Kendrick Nguyen, CEO, Republic, Official Press Release, June 25, 2025

Mirror Tokens: The Payout That Was Always the Point

Republic’s rSPAX Mirror Token was designed explicitly for this moment. The product is a Contingent Payout Note — a debt instrument issued by RepublicX LLC that pays holders based on SpaceX’s common stock performance at a qualifying liquidity event. The IPO qualifies. The reference price of $275 per share (pre-split) now sits well below the IPO price of $675 pre-split equivalent, which means the payout formula should generate returns for holders who invested at or near issuance. The cap on the initial offering was $8 million, which limits the aggregate payout exposure to a manageable level. But as the SEC’s silence on Mirror Token classification has remained a feature rather than a bug, the question of how payouts execute in practice — and whether RepublicX’s balance sheet is capitalized adequately to handle them — is now a live operational question rather than a theoretical one.

The Seedrs-listed version of the rSPAX product added one important wrinkle: the Europe offering specified that the redemption price on an IPO would be measured after the typical lock-up period of 180 calendar days, not at the IPO price itself. That means European rSPAX holders will not receive their payout based on the $160.95 first-day close or the $225.64 intraday high. They will receive it based on wherever SPCX trades around December 2026 — which introduces meaningful additional market risk for investors who thought they were getting exposure to a known IPO event. The distinction between an IPO close and a post-lockup price is not small. Historically, the two numbers diverge significantly for high-hype offerings.

The Lockup Schedule Is the Next Pricing Event

SpaceX’s lock-up structure is deliberately non-standard. Rather than a flat 180-day cliff, the S-1 established a staggered release: 20% of insider holdings become eligible to sell after Q2 2026 earnings (expected around early September), with additional 7% tranches releasing at 70, 90, 105, 120, and 135 days post-IPO. A further 10% unlocks if SPCX closes at least 30% above the $135 IPO price for at least five of the ten trading sessions following the first earnings report. The full 180-day lock-up expires in early December 2026. Elon Musk, who controls approximately 42% of equity and 82% of voting power, is carved out entirely from the early-release provisions and remains locked until June 2027.

The staggered structure was framed as investor-friendly, and it does avoid the single-day supply cliff that has damaged other large IPOs. But for private market vehicles that are themselves subject to the same or similar lock-up terms, each release date is also a potential NAV repricing event. DXYZ’s SpaceX position, for example, cannot be monetized until the applicable lock-up windows open. The gap between the fund’s current market price and its NAV will only close when the underlying position converts to cash — and that process will take most of the rest of 2026. Investors who bought DXYZ at a 150% premium to NAV on the expectation that the SpaceX IPO would immediately unlock value are discovering that the structure does not work that way.

What This Means for OpenAI, Anthropic, and Every Vehicle Behind Them

The SpaceX situation is a preview of a much larger dynamic. Anthropic confidentially filed its IPO prospectus in June, with OpenAI expected to follow. Both companies have extensive secondary market histories, multiple tokenized exposure products, and at least one Mirror Token issuance through Republic. The rAnthropic token was issued with its own reference price; the spread between that reference price and whatever Anthropic ultimately prices at in the public market will determine payouts for a far larger pool of retail investors than the rSPAX pool. The same payout infrastructure — RepublicX’s balance sheet, its USDC distribution system, the INX trading venue — will be handling it.

The secondary market pricing problem that the SpaceX IPO created is not really a problem for investors who got the direction right and held through to the liquidity event. It is a problem for three specific groups: holders in vehicles with premium-to-NAV risk who cannot immediately realize the underlying gain; investors in products where the payout reference date is post-lockup rather than IPO day; and anyone who built a position in a product that was mechanically constrained from tracking the public market in real time. The SpaceX IPO compressed all three of those risks into a single ten-day window. The AI IPO wave will do it again, at considerably larger scale, before the year is out.

What to Watch Next

- RepublicX’s rSPAX payout execution. The first mass Mirror Token payout is now a qualifying liquidity event in progress. Watch for Republic to disclose the timeline for distributing USD or USDC to rSPAX holders, and whether the Seedrs-listed European version confirms a post-lockup reference date. How cleanly this executes will set the credibility baseline for the rAnthropic payout when Anthropic goes public.

- DXYZ’s SpaceX lock-up release schedule. The fund becomes eligible to begin selling SpaceX shares in tranches starting around early September, following the Q2 2026 earnings release. Watch for any DXYZ 8-K or press release confirming it is participating in the early-release provisions, and how it plans to reduce the SpaceX concentration. The NAV premium or discount at that point will tell you whether investors have already priced in the monetization or are still extrapolating from hype.

- SEC guidance on Mirror Token classification. The agency has not issued a formal no-action letter or comment on Republic’s Mirror Token structure. If SpaceX payouts proceed without regulatory challenge, it removes the largest structural risk for rAnthropic and any future issuances. If the SEC moves to classify the instrument differently, the entire product category requires restructuring before the next AI IPO cycle.

- SPCX stock performance through the December lockup expiration. Early insiders including Founders Fund, Sequoia, and Alphabet’s Google hold positions that begin converting to sellable stock across the staggered schedule through December. The stock’s ability to absorb that supply — against a tight 4% float and significant index-inclusion buying pressure — will be the clearest real-world test of whether the valuation holds without the scarcity premium that characterized the IPO.

- OpenAI and Anthropic Mirror Token reference prices versus likely IPO valuations. Anthropic’s most recent private valuation was reported at $900 billion. OpenAI’s round is targeting comparable scale. If either company prices its IPO at a meaningful premium to the Mirror Token reference prices, the payout math works — but RepublicX’s operational capacity to handle two mass payouts in a single calendar year is a separate and unresolved question.