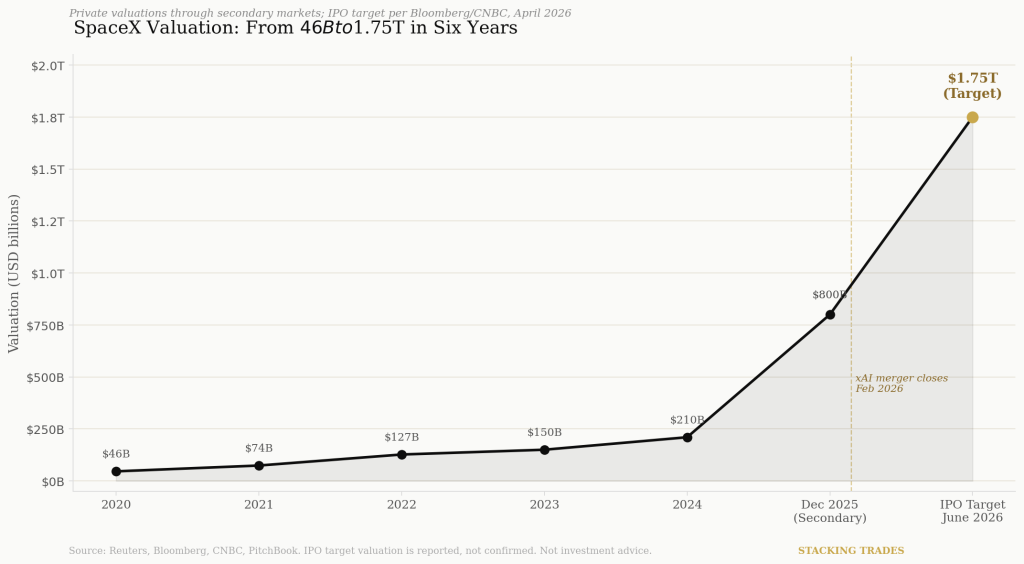

On April 1, 2026, SpaceX submitted its confidential draft registration to the U.S. Securities and Exchange Commission, setting in motion what could be the largest initial public offering in stock market history. Bloomberg reported the filing first. CNBC, Reuters, and the Wall Street Journal confirmed it within hours. The company is targeting a June listing. The valuation cited by multiple outlets is $1.75 trillion, with a capital raise that could reach $75 billion — more than double the $29 billion Saudi Aramco raised in 2019, which currently holds the record.

None of that is the story. The story is what investors don’t have yet.

A confidential filing — standard practice for large listings under the JOBS Act — allows SpaceX to work through SEC comments privately before its financials become public. Under SEC rules, the company must publicly file its full prospectus at least 15 days before the investor roadshow begins. With a June target, that prospectus is expected to land in April or May. Until it does, every valuation figure in circulation is a number derived from secondary market trades, analyst estimates, and sources who spoke to reporters anonymously. No audited revenue breakdown. No subscriber acquisition cost. No disclosed cash burn attributable to xAI. No formal cap table post-merger.

The Starlink Question Is the Only One That Matters

The $1.75 trillion valuation is not primarily a bet on rockets. Starlink ended 2025 with 9.2 million subscribers and generated over $10 billion in revenue, with analysts projecting that figure could reach anywhere from $15.9 billion to $24 billion in 2026 depending on subscriber trajectory and pricing mix. The wide range in analyst projections — a gap of more than $8 billion in a single year — is itself the problem. Nobody has seen the actual unit economics.

What does an average Starlink subscriber generate per month, net of satellite operations, customer support, and terminal subsidies? How much of revenue is consumer versus maritime versus aviation versus government? What is churn? These are the figures that underpin any credible discounted cash flow model, and right now none of them exist in public form. SpaceX’s total 2025 revenue has been estimated at $15 billion to $16 billion with roughly $8 billion in profit, but those are figures sourced from Reuters citing unnamed sources, not from audited financials.

For a company targeting a valuation higher than every S&P 500 constituent except Nvidia, Apple, Alphabet, Microsoft, and Amazon, the margin of uncertainty here is unusual.

The xAI Integration Adds an Entirely New Layer of Risk

In early February 2026, SpaceX completed an all-stock acquisition of xAI, Musk’s artificial intelligence startup, in a deal that valued SpaceX at $1 trillion and xAI at $250 billion — the largest merger in history by combined entity size. The stated rationale was building orbital data centers: using Starlink’s satellite constellation to move AI compute workloads into space, where solar power is abundant and cooling is free.

The concept is technically ambitious. Whether it is financially credible is something the prospectus will need to answer. At the time of the merger, xAI was burning roughly $1 billion per month, according to Bloomberg, as it raced to build out infrastructure against OpenAI and Google. That burn rate, absorbed by SpaceX at the moment of the filing, now sits inside the entity investors are being asked to value at $1.75 trillion.

“The valuation jump from $1.25 trillion at merger close to $1.75 trillion at filing reflects expectations around the combined entity’s space and AI ambitions — not disclosed financials.”

—TheStreet, April 2, 2026

Then there is the talent picture. xAI co-founders Jimmy Ba and Tony Wu departed in February, shortly after the merger closed. By early March, Zihang Dai and Guodong Zhang had also left. Of the 12 people who co-founded xAI with Musk in 2023, only two remain — Manuel Kroiss and Ross Nordeen. Musk publicly acknowledged on X that xAI “was not built right first time around” and needed to be rebuilt from its foundations. That statement, made weeks after the largest merger in history closed at a $250 billion xAI valuation, will almost certainly surface in the prospectus’s risk factors — and will need to be reconciled with the financial picture investors are presented.

The Governance Structure Has No Precedent

SpaceX’s governance heading into a public offering is unlike any company that has come before it. Musk simultaneously holds the CEO role at SpaceX, Tesla, and leads DOGE in a senior advisory capacity. Tesla disclosed that it invested $2 billion of shareholder money into xAI in its Q4 2025 earnings report — and then SpaceX acquired xAI days later. Legal analysts tracking the deal note that consummating a conflicted merger between founder-controlled private companies before going public defers — but does not eliminate — the scrutiny around related-party dynamics. That scrutiny will arrive when the S-1 is public and securities lawyers start reading it.

SpaceX is also reportedly considering a dual-class share structure that would preserve insider voting control, and plans to allocate up to 30% of shares to retail investors — roughly three times the typical allocation in a large IPO. The retail allocation is an unusual move that deserves attention: it broadens the investor base and generates enthusiasm, but it also introduces a class of shareholders with limited governance recourse under a dual-class structure.

What the 21-Bank Syndicate Actually Signals

SpaceX has lined up at least 21 banks for this offering, with Goldman Sachs, JPMorgan Chase, Morgan Stanley, Bank of America, and Citigroup in senior underwriting roles. The deal is internally codenamed “Project Apex.” A syndicate of this size indicates that demand management is already the primary concern — no single bank wants the concentration risk of placing $75 billion in a single offering. It also means the roadshow, when it happens, will be one of the most heavily orchestrated investor events in market history.

One detail worth noting for index-aware investors: Nasdaq recently updated listing rules in a way that could allow SpaceX to join the Nasdaq 100 within 15 days of listing. That would trigger forced buying from index-tracking funds — a mechanical demand wave that has nothing to do with the underlying fundamental case. Investors who intend to evaluate SpaceX on its merits should be aware that initial price behavior after listing may reflect index inclusion mechanics more than actual price discovery.

Stacking Trades has covered the broader conditions shaping the IPO market this spring, including how macro headwinds in early 2026 rattled the IPO window — context that matters when assessing whether a $1.75 trillion listing can clear the market in June regardless of how good the underlying story is.

The Number That Investors Actually Need

The prospectus, when it arrives, will contain information that no source has yet provided: audited revenue by segment, Starlink subscriber economics, the precise mechanics of the xAI acquisition and how xAI’s assets and liabilities are carried on SpaceX’s balance sheet, the terms of the dual-class structure, and the risk factors Musk’s lawyers have deemed material enough to disclose to the investing public.

That document will be the first moment at which a credible, independently verified number can be placed next to the $1.75 trillion figure. Until then, every model being built against that valuation is working from incomplete information. That does not make the offering unattractive. It means the starting gun has been fired — and the race to price it properly has not yet begun.

WHAT TO WATCH NEXT

- The public S-1 prospectus: Expected in April or early May. The Starlink revenue breakdown, per-subscriber economics, and xAI integration terms are the first numbers worth modeling against the $1.75 trillion target.

- xAI’s disclosed cash burn post-merger: At roughly $1 billion per month at acquisition close, any updated figure in the prospectus will materially affect the combined entity’s free cash flow profile.

- Dual-class share structure details: The voting power Musk retains — and what that means for board independence and related-party transaction governance — will be the section securities lawyers read first.

- Nasdaq 100 inclusion timing: If confirmed at listing, forced buying from index funds could distort early price discovery. Watch for Nasdaq’s formal ruling.

- OpenAI and Anthropic IPO timelines: Bloomberg has reported both companies are weighing public offerings in 2026. SpaceX’s pricing and reception will set the reference point for that entire class of mega-listings.