{kind=link}

Bank earnings season opens in six days. Goldman Sachs reports before the bell on April 13. JPMorgan Chase, Citigroup, and Wells Fargo follow the morning after. Morgan Stanley and Bank of America arrive in the days after that. For most of the market, these releases will be read as a quarterly economic checkup. For investors tracking the capital markets cycle — particularly anyone with exposure to private equity, deal-dependent sectors, or the IPO pipeline — they carry a more specific signal: whether the M&A fee recovery that Wall Street has been predicting since late 2024 has actually arrived in the revenue line, or whether it is still, as JPMorgan’s fourth quarter suggested, a story about deals that keep sliding into the next quarter.

The setup has rarely been cleaner for a test like this. Global M&A volume exceeded a record $1.2 trillion in Q1 2026, according to LSEG data cited by Reuters, with dealmakers describing a pipeline that extends well into the year. That follows a 2025 in which global deal value rose roughly 40% to an estimated $4.9 trillion, the second-highest annual total on record, per Bain. The structural drivers — AI consolidation, private equity exits after years of compressed IPO markets, corporate spin-off activity — have not gone away. If anything, they have accelerated.

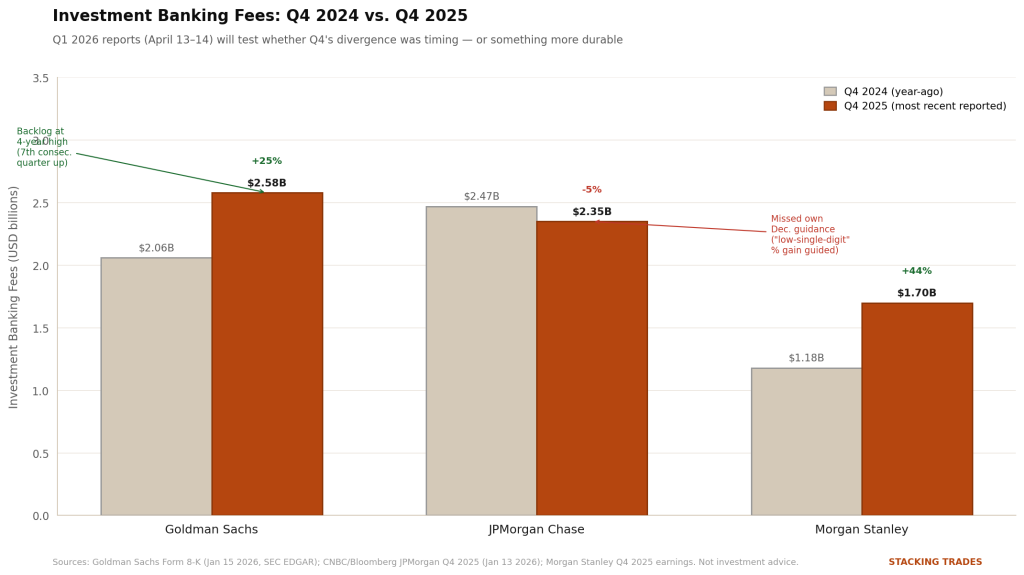

Yet when JPMorgan reported its Q4 2025 results in January, investment banking fees came in at $2.35 billion, down 5% year-over-year and materially below the bank’s own December guidance of a “low single-digit” percentage gain. CFO Jeremy Barnum attributed the shortfall to uneven deal timing — several large transactions originally scheduled for Q4 had been pushed into early 2026. The April report will show whether that explanation holds. If those deals closed in January and February, they show up in Q1 fee revenue. If they slipped again, something more structural is happening.

Goldman Walked In With the Better Story

Goldman Sachs is the more instructive data point going into this cycle. In its Q4 2025 earnings — reported on the same January morning as JPMorgan — the bank disclosed that its investment banking backlog had risen for a seventh consecutive quarter to a four-year high, driven primarily by advisory. Q4 investment banking fees reached $2.6 billion, up 25% year-over-year, with M&A advisory fees up 41%. Goldman’s full-year 2025 advisory fees totaled $4.7 billion, and the bank advised on more than $1.6 trillion of announced M&A — roughly $250 billion more than its nearest peer, according to the earnings transcript filed with the SEC.

That backlog figure matters for what happens April 13. A backlog is not revenue — it is pipeline that has not yet closed. When Goldman reports Q1, analysts will be looking for evidence that deals in that record backlog began converting to completed transactions and realized fees in the first three months of the year. If the advisory line accelerates, it confirms the thesis that the dealmaking surge is real and that Goldman’s market position is delivering. If it stalls, the Q4 backlog disclosure begins to look like a quantity measure that did not account for execution timing.

“Even with very strong accruals in the fourth quarter, our investment banking backlog rose for a seventh consecutive quarter to a four-year high, primarily driven by advisory.” — Goldman Sachs Q4 2025 earnings call transcript, January 15, 2026, via SEC Form 8-K

The Shift from Rate Spread to Fee Income

The broader context matters for investors evaluating bank stocks in a portfolio or as a proxy for deal market health. The banking sector spent most of 2023 and 2024 riding net interest income — the spread between what banks paid depositors and what they earned on loans — as the Federal Reserve held rates at elevated levels. That dynamic began compressing in late 2025 as the Fed cut rates, and JPMorgan now guides for roughly $103 billion in total net interest income in 2026, down slightly from 2025 levels on an adjusted basis.

What the market is watching replace that tailwind is fee income — specifically investment banking advisory, equity underwriting, and debt capital markets revenue. The KBW Bank Index was outperforming the broader S&P 500 by approximately 4% year-to-date through late March, a signal that institutional investors were already pricing in a fee recovery narrative ahead of the April reports. Whether that positioning was premature or prescient is what the next two weeks will determine.

The structural case for fees is not speculative. Morgan Stanley’s Global Co-Head of M&A described the 2025 deal market as unlocking years of pent-up consolidation demand, and projected that 2026 separation activity alone could run 50% higher than any year in the prior decade. Goldman’s own published 2026 M&A outlook pointed to AI as a “macrocurrent” reshaping deal strategy across industries, with private equity dry powder at $4.3 trillion available to deploy. PwC’s outlook noted that technology led megadeal activity in 2025 with 26 announced deals above $5 billion, the highest of any sector.

What the Gap Between Goldman and JPMorgan Actually Means

The divergence in Q4 outcomes between the two biggest names in investment banking is itself instructive. Goldman posted a fee beat on a strong backlog. JPMorgan posted a miss despite a recovering deal environment. The difference appears to trace to product mix and timing rather than market share collapse: Goldman’s strength was concentrated in advisory and debt underwriting, while JPMorgan’s weakness was most pronounced in debt underwriting, which fell 2% year-over-year against analyst models that had projected a near-20% rebound. Jefferies — a smaller firm with a more advisory-heavy mix — reported a 20% surge in investment banking revenue in the same period, suggesting the deal market itself was healthy and the shortfall was JPMorgan-specific.

JPMorgan’s CFO signaled optimism for 2026 fees on the January call, declining to give specific guidance but noting the bank was “obviously optimistic on investment banking fees generally.” That phrasing — deliberately cautious, directionally positive — sets a lower bar for the April 14 report than Goldman faces on April 13. If JPMorgan shows a meaningful recovery in debt underwriting alongside advisory, the Q4 miss gets reclassified as timing noise. If underwriting disappoints again, it becomes a pattern.

For investors using these earnings as a read on the private markets ecosystem — including the IPO calendar that platforms like this one track closely — the most important data point is pipeline guidance for the rest of 2026. SpaceX’s confidential S-1 filing, the Cerebras IPO targeting a Q2 Nasdaq debut, and a queue of private equity exits that have been building for three years all depend on the same conditions: functioning capital markets, institutional appetite for new issuance, and deal financing that clears at reasonable spreads. What Goldman and JPMorgan say about their pipelines on April 13 and 14 will be the first real-time read on whether that window is opening or still waiting.

The Credit Question Nobody Is Asking Yet

There is a secondary signal in these reports that gets less attention than the fee story but may matter more to the second half of the year. Bank of America’s early 2026 data showed mortgage delinquencies rising at an elevated pace in the broader market, even as BAC itself reported a low 0.99% delinquency rate on its own book. JPMorgan’s consumer credit metrics — card delinquencies, loss provisions, and guidance on consumer spending resilience — will provide the clearest picture of whether the macro backdrop supporting deal confidence is as solid as the M&A volume figures suggest, or whether there are cracks in household balance sheets that have not yet flowed into corporate deal appetite.

A fee beat paired with a consumer credit warning is a different signal than a clean beat across the board. The April reports will carry both stories simultaneously, and investors who read only the investment banking line will miss half the picture.

WHAT TO WATCH NEXT

- Goldman Sachs Q1 2026 earnings release, April 13 before market open — the advisory fee line versus Q4 2025’s $2.6 billion baseline and any updated language on backlog conversion will be the clearest indicator of whether the M&A recovery has arrived in earned revenue.

- JPMorgan Chase Q1 2026 earnings release, April 14 — debt underwriting is the specific line to watch after Q4’s miss; CFO Jeremy Barnum’s guidance language on full-year fee expectations will set the tone for the rest of the sector.

- Citigroup and Wells Fargo, also April 14 — Citi’s investment banking franchise has been rebuilding after the consumer business restructuring; its advisory and underwriting results will show whether the fee recovery is broad-based or concentrated at Goldman and JPMorgan.

- Deal pipeline guidance language — both quantitative (backlog levels) and qualitative (CEO confidence commentary, regulatory outlook) will determine whether Q2 is set up to sustain the Q1 M&A volume record or give some of it back.

- Private equity exit signaling — any commentary on sponsor-backed IPO timelines or secondary buyout activity will directly affect the private market calendar that income-seeking accredited investors track most closely.