For weeks, Terafab read like a Musk announcement in search of an execution plan. The March 21 unveiling was characteristically ambitious: Tesla, SpaceX, and xAI would construct the largest semiconductor facility ever built in Austin, Texas, targeting one terawatt of annual compute output, combining logic, memory, and packaging under one roof, and breaking from the global foundry supply chain that every other AI hardware company still depends on. It was a compelling vision with one conspicuous gap. None of the three companies announcing it had ever built a chip fab.

That gap closed on April 7, when Intel announced it was joining the project. The announcement arrived as a post on X rather than a press release: “Our ability to design, fabricate, and package ultra-high-performance chips at scale will help accelerate Terafab’s aim to produce 1 TW/year of compute.” Intel CEO Lip-Bu Tan followed with his own post describing Musk as having “a proven track record of reimagining entire industries” and calling Terafab “a step change in how silicon logic, memory and packaging will get built in the future.” Intel shares rose roughly 4% on the news, finishing the day near their 52-week high of $54.60.

The stock reaction is the easiest part to explain. The strategic logic, for both parties, is more complicated, and more important for investors trying to assess whether this partnership changes Intel’s medium-term trajectory or simply adds to a long list of announcements the company has made in the past 18 months that have yet to show up in the revenue line.

What Intel Actually Brings to the Table

When Intel said it would help “refactor silicon fab technology,” the phrasing was deliberate and specific. Refactoring in semiconductor development refers to redesigning or improving existing manufacturing processes, not building from scratch. Scott Bickley, an advisory fellow at Info-Tech Research Group, described the language as implying “a potential redesign or improvement of existing methods” — a narrower scope than the greenfield chip factory that Musk’s March announcement had suggested.

What Intel concretely provides is an end-to-end semiconductor manufacturing capability that no other American company can currently match. Its 18A process node, the most advanced manufacturing technology developed on U.S. soil, is already running at its Chandler, Arizona facility at approximately 40,000 wafer starts per month, and was opened to external customers for the first time earlier this year after being largely reserved for internal use. Terafab, targeting 2-nanometer-class process technology, represents a natural fit for 18A’s capabilities. Intel also brings advanced chip packaging expertise, combining multiple chiplets into high-performance units, which Lip-Bu Tan has called “a very big differentiator” in the current AI hardware race.

The project envisions two fabrication facilities on the grounds of Giga Texas in Austin, one oriented toward automotive and robotics chips, including Tesla’s FSD hardware, Optimus humanoid robots, and Cybercab, and the other focused on high-performance AI data center infrastructure including designs intended for SpaceX’s proposed space-based data centers. According to reporting from The Tech Portal, Terafab plans to start at 100,000 wafers per month in its pilot phase, with total initial capital costs estimated between $20 billion and $25 billion.

“Terafab represents a step change in how silicon logic, memory and packaging will get built in the future.”

— Lip-Bu Tan, CEO, Intel, April 7, 2026, via post on X

What Intel Needs More Than the Announcement

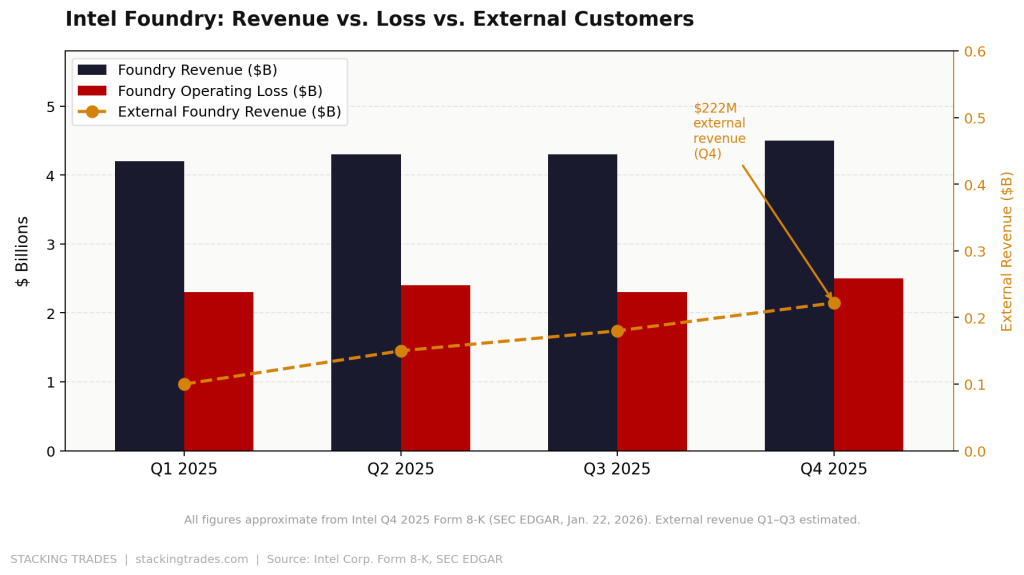

The Intel of 2026 is a company that has been saying the right things for two years and struggling to make them show up in the numbers. Its Q4 2025 earnings, filed as an 8-K with the SEC, showed revenue of $13.7 billion, down 4% year-over-year and Intel’s weakest full-year result since 2010 at $52.9 billion. The Intel Foundry segment, the linchpin of Lip-Bu Tan’s strategic pivot, generated $4.5 billion in quarterly revenue against an operating loss of $2.5 billion, a figure that widened by $188 million from the prior quarter due to the early ramp of the 18A process node. External foundry revenue in Q4 was $222 million, almost entirely from U.S. government projects and residual Altera activity after that subsidiary’s partial sale.

That $222 million figure is the most important number in Intel’s foundry story, and it is the one Terafab is designed to change. Intel has been building foundry capacity for two years with effectively no major commercial anchor customers. Its SEC filings explicitly flagged this as a risk: the company had not secured external foundry customers at meaningful scale on any of its process nodes. Lip-Bu Tan acknowledged on the Q4 earnings call that Intel had “invested too much, too fast” given the demand it had actually secured. The U.S. government holds a roughly 8.4% stake in the company, acquired through an approximately $9 billion equity investment, partly as a strategic backstop for domestic semiconductor capacity. That support has kept the foundry strategy alive. It has not replaced the commercial anchor customer Intel needs to justify its capital program at scale.

Terafab is that anchor customer, in theory. Analysts who follow Intel’s foundry strategy note that landing SpaceX, Tesla, and xAI as a combined demand source would provide the volume and technical complexity that Intel’s internal roadmap cannot generate on its own. The question is whether the partnership converts from a handshake-and-X-post to a signed foundry services agreement with committed volumes, and on what timeline.

The TSMC Dependency Musk Is Trying to Break

To understand why Terafab exists, it helps to understand the supply chain problem it is solving. Every major AI chip company, including Nvidia, AMD, Broadcom, and the in-house design teams at Google, Amazon, and Microsoft, currently depends on TSMC for advanced node manufacturing. TSMC’s Taiwan-based fabs produce the majority of the world’s leading-edge chips, and its capacity is spoken for years in advance. The geopolitical risk embedded in that concentration has been discussed at every level of U.S. industrial policy since 2022, which is why the CHIPS Act directed tens of billions of dollars toward domestic semiconductor manufacturing expansion.

Musk’s companies face this dependency acutely. Tesla’s FSD hardware, xAI’s training and inference infrastructure for its Grok models, and SpaceX’s ambitions for radiation-hardened orbital processors all require advanced chips at volumes that cannot be easily secured in the current TSMC queue without multi-year lead times and pricing leverage that smaller customers lack. Terafab’s vertical integration model, where design, fabrication, packaging, and testing happen in a single facility rather than across a fragmented global supply chain, is an explicit attempt to exit that dependency.

Intel’s position in this logic is strategic rather than financial, at least in the near term. It provides the technical credibility Terafab needs to be taken seriously as a manufacturing program rather than a press release. It gets, in return, the largest potential commercial foundry engagement in its history, access to a customer that will push its 18A and packaging capabilities to their limits, and a narrative shift at a moment when its stock is recovering from lows below $18 last year. The Cerebras IPO narrative, covered here in a prior analysis, and now Terafab are two different bets on the same underlying thesis: the AI chip stack is too concentrated in a single supplier, and the companies building alternatives now will extract significant value over a multi-year horizon.

The Execution Risk Nobody Is Pricing Yet

The 4% stock pop reflects enthusiasm. What it does not yet reflect is the difficulty of what has been announced. Building a leading-edge semiconductor fab at the scale Terafab describes is among the most complex industrial undertakings in existence. TSMC’s Arizona facility, by comparison, has faced repeated delays reaching full production despite years of preparation and a workforce that already knew how to make the chips. Terafab is proposing to build not one but two fabs on a site that was previously a vehicle factory, in a state with no existing semiconductor manufacturing ecosystem, on a timeline that analysts at Info-Tech Research Group described as yielding “near-term impact probability for this year close to 0%.”

The partnership is also still scant on contractual detail. Bloomberg reported that Intel’s role involves helping “refactor” an existing chip factory, a narrower mandate than the end-to-end fab construction that Musk’s March announcement implied. TechCrunch noted that the scope of Intel’s contributions “are unclear.” That uncertainty is not a reason to dismiss the announcement, but it is a reason to distinguish between what has been announced, a partnership with intent, and what has been committed, signed agreements with capital allocations and volume targets.

Intel’s next earnings report on April 23 will be the first opportunity to hear Lip-Bu Tan describe the commercial structure of the relationship, whether Terafab is already generating contracted foundry revenue or remains a pipeline commitment. The former would be a material positive for Intel’s foundry narrative. The latter would sustain the stock movement while postponing the fundamental question of when the customer translates into cash.

For investors tracking the AI chip stack broadly, the significance of April 7 is less about Intel’s quarterly trajectory and more about what it signals at the industry level. The era of Nvidia-plus-TSMC as the only viable path to frontier AI compute is being challenged simultaneously from multiple directions, Cerebras on inference speed, Eclipse’s physical AI fund on chip infrastructure investment, and now Terafab on vertically integrated domestic manufacturing. Whether any of these challenges resolves into a durable alternative is a question that will be answered over years, not quarters. What Intel’s participation in Terafab confirms is that the challenge is now serious enough to attract a company with the technical capability to actually execute it.

What to Watch Next

- Intel Q1 2026 earnings, April 23 — Lip-Bu Tan’s first public opportunity to describe the commercial terms of the Terafab partnership. Whether it is characterized as a signed foundry customer agreement or a letter of intent will determine whether the stock’s recent run has fundamental support or has outpaced the contract structure.

- External foundry revenue line — In Q4 2025, Intel’s external foundry revenue was $222 million, nearly all from government projects. Any meaningful Terafab volume commitment would need to begin showing up in this line within the next one to two quarters to validate the commercial narrative.

- Terafab ground-breaking or construction milestone — Musk-affiliated projects often announce aggressively and build on compressed timelines. A formal ground-breaking at Giga Texas’s north campus would signal that capital is being committed, not just announced.

- Nvidia’s response to domestic competition — Nvidia has no domestic foundry relationship that matches Terafab’s implied scale. If the project advances, it forces a strategic question about whether Nvidia’s TSMC dependency becomes a long-term liability in a policy environment that increasingly favors domestic semiconductor production.

- Google and Amazon packaging talks with Intel — Separate from Terafab, Intel has been in reported discussions with Google and Amazon for advanced packaging services. If those agreements are announced alongside the Terafab commitment, it would confirm that Intel’s foundry strategy is gaining commercial traction across multiple fronts simultaneously, not just through Musk’s ecosystem.

- The Cerebras Nasdaq listing — Cerebras and Terafab are both bets on alternatives to the dominant Nvidia-TSMC supply chain. If Cerebras prices successfully and trades above its $23 billion private valuation, it would increase institutional appetite for the broader AI chip diversification thesis that Terafab represents at the manufacturing layer.