The target date has been on the calendar since early March. When U.S. Customs and Border Protection told the Court of International Trade it needed roughly 45 days from March 6 to build a functional refund system, the math put a go-live window around mid-to-late April. CBP’s most recent court filings have confirmed late April 2026 as the target for Phase 1 of the Consolidated Administration and Processing of Entries system, known as CAPE. For the roughly 330,000 importers that paid duties under the now-invalidated International Emergency Economic Powers Act regime, that launch date is not an administrative milestone. It is an accounting event — and for publicly traded companies that have been conservative on IEEPA refund recognition, it may be the most consequential disclosure moment of the Q1 earnings cycle.

The legal predicate is settled. On February 20, 2026, the Supreme Court ruled 6-3 in Learning Resources, Inc. v. Trump that IEEPA does not authorize the President to impose tariffs unilaterally. The ruling invalidated approximately $166 billion in collected IEEPA duties, with some estimates placing the total closer to $175 billion once entries through early 2026 are included. The Court of International Trade ordered CBP to begin refunding those duties on March 4. CBP responded by requesting time to build a system capable of processing refunds at scale — and CAPE is that system.

What happens when CAPE goes live is not simply that refunds begin to flow. It is that companies which have been excluding IEEPA refund recovery from their guidance and their financial statements will face a concrete, operational trigger for the disclosure decision they have been deferring.

What CAPE Actually Does — and What It Doesn’t Cover Yet

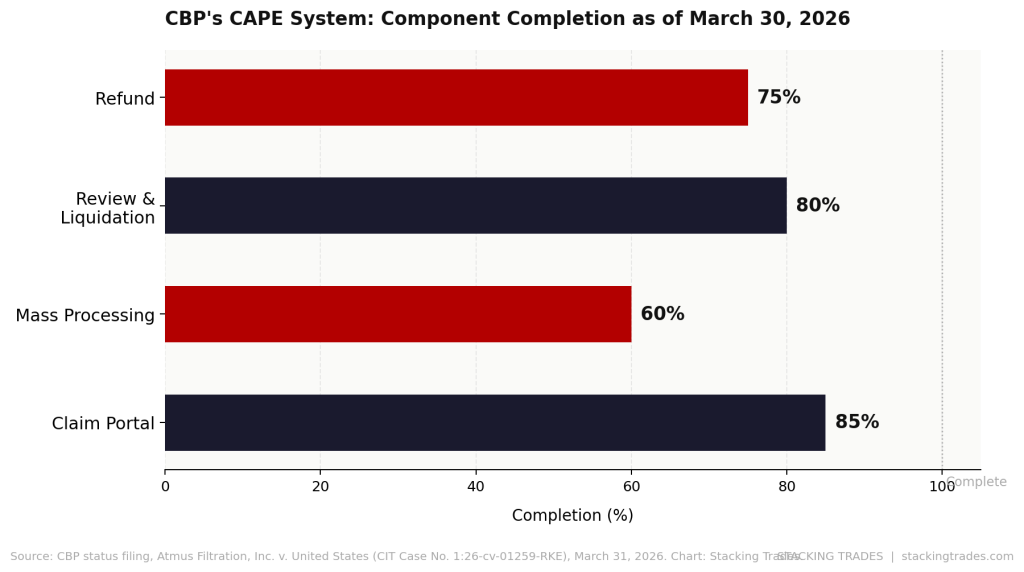

CAPE is a new module inside CBP’s existing Automated Commercial Environment system. As described in CBP’s March 31 status filing with the Court of International Trade, the system has four integrated components: a Claim Portal, Mass Processing, a Review and Liquidation/Reliquidation function, and a Refund component. As of March 30, CBP estimated completion at 85% for the Claim Portal, 60% for Mass Processing, 80% for Review and Liquidation, and 75% for the Refund component.

The process works as follows: importers or their customs brokers submit a CAPE Declaration through the web-based portal — a CSV file listing all entry summaries for which they are requesting IEEPA duty refunds. The system validates the submission, removes IEEPA-related tariff codes, recalculates duties as if IEEPA had never applied, and initiates a liquidation or reliquidation process. CBP has stated that the review and liquidation cycle will take up to 45 days from acceptance, with refunds delivered electronically via ACH payment.

Phase 1 is designed to cover approximately 63% of all entries on which IEEPA duties were paid. That percentage reflects unliquidated entries and entries within the 90-day voluntary reliquidation window, plus entries with suspended, extended, or under-review status, and warehouse and warehouse withdrawal entries. What Phase 1 will not immediately process are entries that have been finally liquidated — those for which the standard 180-day protest period has expired — although a March 27 court order from Judge Richard K. Eaton directed that even finally liquidated entries must ultimately be reliquidated without regard to IEEPA duties. CBP has said those will be addressed in subsequent phases.

One structural constraint matters for companies with large import volumes: as of March 26, only 26,664 importers of record had completed the ACH enrollment required to receive electronic refunds. Those importers represent 78% of entries and approximately $120 billion in IEEPA duty payments. The remaining 22% of entries — covering smaller importers who have not yet configured ACE portal access and banking details — will face automatic rejection when they attempt to file claims. That is an operational problem for smaller players, but for large publicly traded importers with active customs brokers, enrollment is largely complete.

The Disclosure Decision That Moves Stocks

The more consequential question for equity investors is not whether CAPE works, but what companies say about it in their next quarterly filings. As covered in our analysis of corporate tariff disclosures, the gap between companies that have quantified their IEEPA exposure and those that have excluded refund recovery from guidance is wide — and deliberate. Dollar Tree explicitly told investors it would not treat any potential IEEPA refund as a planning assumption. Abercrombie & Fitch built its guidance around a 15% Section 122 tariff rate with no refund benefit included. Carter’s projected a gross tariff impact of over $200 million in 2026 without incorporating any recovery assumption.

When CAPE goes live, those conservative postures meet a concrete operational threshold. Under U.S. GAAP, a receivable can be recognized when the right to receive payment is both probable and estimable. CAPE’s go-live does not automatically satisfy that standard — the 45-day review window, the phased implementation, and ongoing court proceedings create enough uncertainty that most auditors will resist immediate full recognition. But the calculus changes. Companies that have been excluding IEEPA refunds on the grounds that the refund mechanism was undefined now face a mechanism that is, to varying degrees, defined. How each company’s finance team and auditors treat that shift is a company-specific judgment, and one that could generate material disclosures in Q1 filings — particularly for companies with large IEEPA duty exposures and strong cash positions that would make a receivable recognition meaningful relative to guidance.

“In our outlook commentary today, we have not incorporated any developments related to last week’s Supreme Court decision and subsequent action by the administration.”

— Richard Westenberger, CFO, Carter’s Inc., Q4 2025 Earnings Call, February 27, 2026

Trade analysts at TD Securities have estimated the timeline for most refunds to arrive at 12 to 18 months, reflecting the volume of entries, the phased system implementation, and the likelihood of government challenges to the process. That extended timeline counsels against treating a CAPE filing as equivalent to cash in hand. But it does not eliminate the disclosure obligation — it shapes it. Companies must decide whether IEEPA refund recovery is probable enough, and estimable enough, to warrant recognition or disclosure in their financials, even if actual receipt is months away.

The Consumer Class Action Overhang Nobody Has Priced

There is a second layer of exposure that has received almost no attention in equity coverage of the IEEPA refund story. Companies that paid IEEPA tariffs and passed those costs to consumers through higher prices are now facing a wave of putative class action lawsuits alleging unjust enrichment. The theory is straightforward: if a company raised prices citing tariff costs and will now receive those tariff costs back from the government, consumers who absorbed the price increases are entitled to a share of the recovery.

At least five federal class action complaints had been filed by early March, targeting companies including FedEx, UPS, and EssilorLuxottica. On March 27, a proposed class action was filed against Lululemon in the Eastern District of Michigan, alleging the company passed approximately $240 million in IEEPA tariff costs to consumers while simultaneously pursuing a full government refund. Plaintiffs’ firms are actively recruiting additional plaintiffs across retail, consumer goods, apparel, and logistics — any sector where tariff surcharges were itemized on invoices or publicly cited as the rationale for price increases.

This litigation risk is not yet reflected in most companies’ tariff disclosures or in analyst models. The legal theory is novel and untested, and courts may ultimately find that importers of record have no obligation to share government refunds with end consumers. But the litigation itself creates costs — defense, discovery, management distraction — and the public earnings call statements and press releases that plaintiffs are already citing in their complaints represent a disclosure risk that companies underestimated when they were transparent about tariff pass-through during 2025.

The implication for investors is that the IEEPA refund story has at least three moving parts that are not yet resolved simultaneously: whether CAPE Phase 1 launches on the late-April schedule and processes claims efficiently; whether companies with large exposures recognize refund receivables in their Q1 or Q2 filings, creating positive earnings surprises in sectors that have guided conservatively; and whether the consumer class action litigation constrains the net benefit of those recoveries in ways that have not been modeled. Companies with the clearest answers across all three — firms that have quantified their IEEPA exposure, prepared their ACE filings, and assessed their consumer-facing price increase communications — are in the strongest position to turn a legal victory into a financial one. Companies that assumed the refund was too uncertain to plan around may find, when CAPE goes live, that the planning window was shorter than they thought.

What to Watch Next

- CAPE Phase 1 go-live confirmation — CBP has targeted late April but has not committed to a specific date. The official launch announcement, when it comes, will open the filing window for approximately 26,664 enrolled importers representing an estimated $120 billion in IEEPA duties. The first week of claims volume will signal whether the system can process submissions at scale or whether technical bottlenecks slow the queue.

- Q1 earnings disclosures from large importers — Companies reporting April earnings with material IEEPA exposure — including Dollar Tree, Carter’s, Abercrombie & Fitch, and major apparel and consumer goods importers — will face direct analyst questions about whether the CAPE launch changes their refund recognition posture. Any company that shifts from excluding refund recovery to disclosing a probable receivable will generate a stock-moving earnings surprise in a sector that has guided conservatively.

- CBP’s Phase 2 timeline for finally liquidated entries — Phase 1 covers roughly 63% of IEEPA entries. The March 27 court order mandated that finally liquidated entries also be reliquidated without IEEPA duties, but CBP has deferred those to a subsequent phase with no committed date. Companies with large volumes of entries that have moved past the 90-day window are waiting for Phase 2 before they can quantify and file.

- The government’s appeal posture — CBP has until approximately early May 2026 to appeal the CIT’s March 4 refund order. Any appeal filing would reintroduce legal uncertainty into the refund timeline and give companies that have been conservative on recognition additional cover for continued exclusion from guidance.

- Consumer class action rulings on standing — The first substantive rulings on whether consumers have standing to claim a share of IEEPA refunds will set the litigation parameters for the broader wave of cases. Early decisions in the FedEx, UPS, and Lululemon matters will determine whether the consumer class action exposure is a manageable nuisance or a material liability that must be disclosed separately from the refund receivable itself.