.jpg){kind=link}

On April 27, a federal jury in Oakland, California, will begin hearing the most consequential corporate governance lawsuit in the history of artificial intelligence. The plaintiff is Elon Musk. The defendants are OpenAI, Sam Altman, Greg Brockman, and Microsoft. The stakes, as framed by Musk’s own attorneys in a court filing dated April 7, 2026, are the unwinding of OpenAI’s for-profit conversion, the removal of its chief executive, and the disgorgement of what Musk’s legal team has described as more than $134 billion in ill-gotten gains — to be returned, in a notable pivot, not to Musk personally, but to the OpenAI nonprofit.

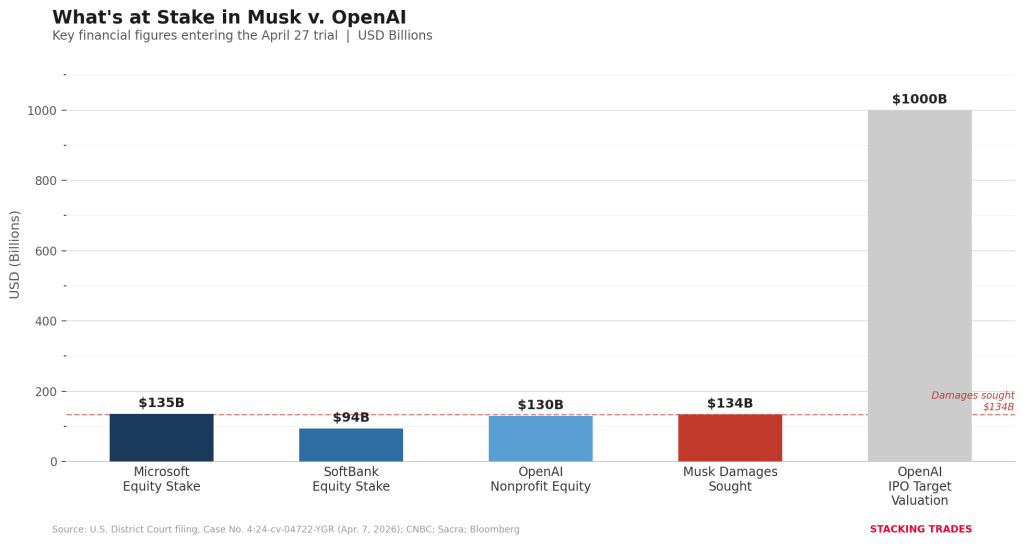

For investors, this is not a celebrity feud. It is a live legal proceeding that puts foundational questions about OpenAI’s corporate structure — and by extension Microsoft’s roughly $135 billion equity stake, OpenAI’s planned IPO, and the valuations of every company in the AI infrastructure supply chain — directly before a jury with the power to order structural relief no analyst has modeled into a stock price.

What Musk Is Actually Asking the Court to Do

The amended notice of remedies filed April 7 in Case No. 4:24-cv-04722-YGR is worth reading as a primary document rather than through the filter of press coverage. In it, Musk’s attorneys at Toberoff & Associates and MoloLamken LLP specify five forms of injunctive relief they intend to seek if the jury returns a verdict against the defendants. First, a permanent injunction requiring both the OpenAI nonprofit and any for-profit subsidiary to honor the original charter commitments of safety-first AI development and open research. Second, the removal of Sam Altman from the nonprofit board and of both Altman and Greg Brockman from their officer roles in the for-profit entity. Third, disgorgement to the OpenAI charity of all equity and personal financial benefits Altman and Brockman obtained from the for-profit operations. Fourth, disgorgement of Microsoft’s gains — the filing explicitly names Microsoft as a party required to return benefits to the charity. Fifth, the unwinding of OpenAI’s for-profit conversion and restructuring.

The filing states plainly: Musk “will not seek, either at trial or in equitable proceedings afterwards, a remedy directed to benefiting himself personally.” The strategic shift in posture — from Musk-as-aggrieved-donor to Musk-as-guardian-of-the-public-trust — is designed to neutralize the most effective line OpenAI has used against the lawsuit: that the billionaire founder of a competing AI company is using litigation as a competitive weapon. By redirecting any potential recovery to the nonprofit, Musk’s team makes it harder to argue the case is self-interested, even if the underlying motive remains competitive.

The OpenAI Counteroffensive

OpenAI is not sitting still. On April 6, chief strategy officer Jason Kwon sent a letter to California Attorney General Rob Bonta and Delaware Attorney General Kathy Jennings urging them to investigate Musk for what he described as “improper and anti-competitive behavior” — specifically, coordinating with Meta and its CEO Mark Zuckerberg to undermine OpenAI’s restructuring. The letter argues that Musk’s lawsuit, seeking damages exceeding $100 billion from the nonprofit, would effectively cripple the organization. Kwon told the attorneys general directly: “These attacks are designed to take control of the future of AGI out of the hands of those who are legally obligated to pursue the mission of ensuring that AGI benefits all of humanity, and put it into the hands of competitors who lack mission-driven principles and spurn any responsibility for safety.”

That letter is a litigation strategy, not a regulatory filing — it asks state officials to investigate, not act. But it also signals that OpenAI’s courtroom defense will lean heavily on the argument that Musk’s lawsuit is itself anti-competitive conduct, designed to slow a rival while his own company, xAI, seeks to gain market share. The case will be tried before Judge Yvonne Gonzalez Rogers, who ruled in January 2026 that there was “plenty of evidence” for a jury to consider Musk’s fraud and unjust enrichment claims. That determination — that the case has enough factual basis to reach a jury — is the most important legal development the market has not priced.

“Defendants pocketed the benefits of that charitable status — tax exemptions, donor contributions, and the reputational credibility of a public-benefit mission — while secretly planning, and ultimately executing, a wholesale conversion of OpenAI into a for-profit enterprise that, along with profligate self-dealing, was designed to generate extraordinary personal wealth for Altman, Brockman, Microsoft, and other investors.”

— Plaintiff’s Amended Notice of Remedies, Case No. 4:24-cv-04722-YGR, filed April 7, 2026, U.S. District Court, Northern District of California

What the Trial Puts at Risk for Investors

The financial exposure here is not theoretical. Microsoft holds approximately 27% of OpenAI Group PBC — a stake valued at roughly $135 billion at OpenAI’s most recent $852 billion private valuation, which was established by a $122 billion fundraising round that closed March 31. Microsoft’s position is the single largest strategic AI investment in corporate history, a 17x return on roughly $13 billion deployed between 2019 and 2023. If the trial produces a verdict that requires disgorgement of Microsoft’s gains or structural changes to its commercial relationship with OpenAI — including the revenue-sharing arrangement under which Microsoft receives 20% of OpenAI’s revenue through 2032 — the impact on Microsoft’s balance sheet and forward earnings guidance would be material.

OpenAI itself is preparing for a public listing that multiple reports now place in Q4 2026, at a valuation that advisers are targeting at or above $1 trillion. The company crossed $25 billion in annualized revenue in February 2026, serves more than 900 million weekly active users, and has raised capital from SoftBank, Amazon, and Nvidia. None of those figures change what a jury verdict could do to the corporate structure that underlies the IPO. OpenAI completed its recapitalization in October 2025, converting into a public benefit corporation with the original nonprofit retaining a 26% equity stake. The Musk lawsuit directly challenges the legality of that recapitalization. A verdict in Musk’s favor would not automatically unwind the structure — post-trial equitable proceedings before Judge Rogers would handle that — but it would create regulatory and governance uncertainty that no underwriter wants to explain in a roadshow.

The New Yorker Factor and the Discovery Risk

The timing of a New Yorker investigation published April 7 — the same day as Musk’s amended court filing — adds a layer the market has not fully processed. According to reporting by Ronan Farrow and Andrew Marantz, Musk himself was involved in discussions about reconstituting OpenAI as a for-profit company as early as September 2017, and had demanded majority control of any for-profit structure. If that account holds up under cross-examination, it cuts directly against Musk’s fraud narrative: a plaintiff who demanded control of a for-profit structure cannot easily claim he was deceived into believing none would exist.

But it also means the trial is likely to produce document disclosures, deposition testimony, and internal communications from both Musk and Altman that no analyst has seen. That is the discovery risk that sophisticated investors tend to underweight in litigation of this kind. The trial is a four-week proceeding. The documents that surface during it — about OpenAI’s founding promises, its 2019 restructuring, the terms of Microsoft’s investment, and the internal governance of the nonprofit — will represent the most detailed public window into OpenAI’s early financial and strategic history before the IPO S-1 is filed. What comes out of that courtroom may matter more to IPO pricing than anything in the prospectus itself.

Microsoft’s Structural Position in the Crosshairs

Microsoft’s involvement as a named defendant — on claims of aiding and abetting breach of fiduciary duty and unjust enrichment — is the element of the trial that gets the least attention in market coverage. The FTC has been investigating Microsoft’s cloud and AI bundling practices since late 2024, issuing civil investigative demands to competitors and escalating into 2026. The OpenAI trial adds a parallel legal front. Microsoft attorney Russell Cohen argued in pretrial proceedings that the company had no direct contractual obligation to Musk and that any duty, if it existed, lay with OpenAI alone. Judge Rogers has allowed the aiding-and-abetting claim to proceed regardless.

The practical implication: a verdict that reaches Microsoft’s conduct would create simultaneous legal exposure on two fronts — federal antitrust scrutiny and state-law unjust enrichment liability — at precisely the moment the company is presenting its AI investment as its primary growth thesis. Microsoft’s commercial remaining performance obligation stood at $625 billion as of Q2 FY2026, with AI cited as a primary growth driver. As covered in the broader agentic AI valuation debate, investors are already struggling to price the transition from per-seat SaaS to outcome-based AI revenue. A trial verdict that introduces governance uncertainty into the OpenAI-Microsoft relationship would compress multiples further, regardless of the underlying revenue trajectory.

What a Verdict Actually Does — and Doesn’t — Do

It is worth being precise about what the April 27 trial can and cannot produce. The jury’s role is to determine liability — whether Musk’s fraud, breach of contract, and unjust enrichment claims are supported by the evidence. The jury does not order corporate restructuring. If it finds for Musk, post-trial equitable proceedings before Judge Rogers would address the injunctive relief he is seeking: the unwinding of OpenAI’s for-profit structure, the removal of Altman and Brockman, the disgorgement order against Microsoft. Those proceedings would likely take months and face their own appeals.

A defense verdict — a finding that OpenAI did not commit fraud or breach its founding commitments — would clear the legal cloud over the IPO and potentially accelerate the timeline. OpenAI has said it expects to file its IPO in the second half of 2026, with a listing that could extend into 2027. A jury that exonerates Altman and the company removes the single largest governance risk in the prospectus. A verdict for Musk creates the opposite: an injunction proceeding that likely extends well past any planned roadshow, a structural uncertainty that underwriters would have to disclose, and a scenario in which Microsoft’s equity stake becomes the subject of court supervision before it becomes liquid.

Neither outcome is priced. The trial begins April 27.

What to Watch Next

- Jury selection, April 27 — the first day of proceedings will determine how quickly the trial moves into substantive testimony. A jury that seats quickly suggests Judge Rogers has managed the pretrial calendar efficiently; delays signal that the forum-shopping and juror-bias arguments OpenAI has flagged may complicate the process.

- Internal documents entered into evidence — the founding-era communications between Musk, Altman, and Brockman from 2015 to 2019, including the September 2017 discussions flagged by the New Yorker, will be the trial’s most market-moving disclosures. Any document showing Musk was aware of for-profit planning will directly undercut his fraud narrative and affect how analysts model the IPO discount.

- Microsoft’s trial defense — the company’s attorneys will argue the aiding-and-abetting claim fails for lack of a direct obligation to Musk. If Judge Rogers grants a directed verdict on the Microsoft claims mid-trial, it removes the most systemic risk to the AI infrastructure investment thesis and is likely to move Microsoft stock.

- OpenAI IPO S-1 timing relative to trial conclusion — the trial is expected to run four weeks, concluding around May 22. If OpenAI files its public S-1 before a verdict, investors will be reading a prospectus with live litigation disclosure. If filing waits for the verdict, the IPO window compresses. Watch for any S-1 filing date signals from underwriters JPMorgan, Goldman Sachs, and Morgan Stanley in the weeks following trial close.

- The California and Delaware AG response to OpenAI’s letter — Kwon’s April 6 request for an antitrust investigation of Musk by both states is unlikely to produce formal action before the trial concludes, but any signal that either office is opening an inquiry would add regulatory dimension to the competition dynamic between xAI and OpenAI that currently has no official regulatory home.