On March 17, 2026, StartEngine Crowdfunding, Inc. entered into an Agreement and Plan of Reorganization with Vinovest, Inc., a West Hollywood-based platform for fine wine and whisky investment. The deal closed the same day, with StartEngine issuing 8,750,000 shares to Vinovest stakeholders — including a 1,750,000-share holdback for potential indemnification claims — in a transaction structured as a full merger, with Vinovest becoming a wholly-owned subsidiary. The formal announcement landed on March 23. Financial terms beyond the share consideration were not disclosed.

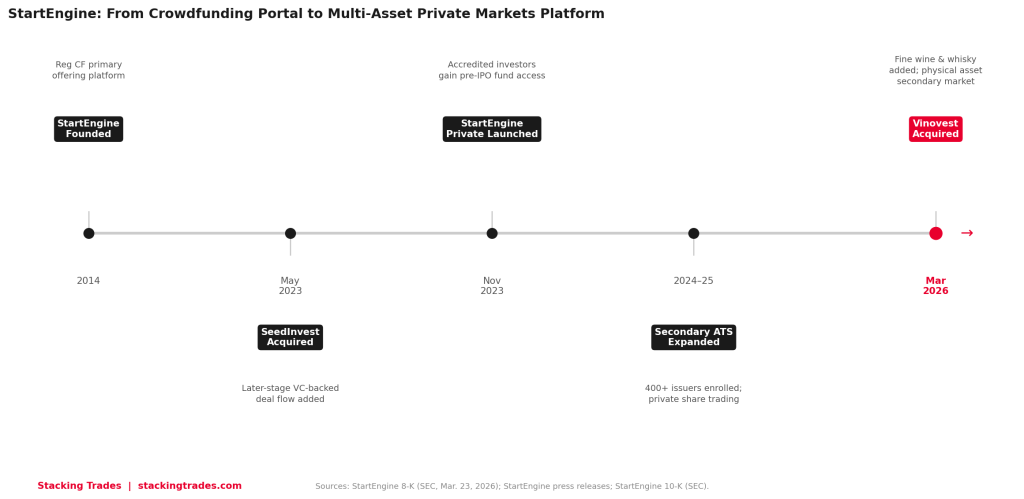

On its face, a crowdfunding platform buying a wine investment app is an odd headline. Looked at differently, it is the clearest articulation yet of what StartEngine is actually building — and it has nothing to do with crowdfunding, at least not in the original sense of the term. The Vinovest acquisition is the third major platform move in less than three years, following the 2023 asset acquisition of SeedInvest and the November 2023 launch of StartEngine Private, a product that gives accredited investors access to pooled vehicles holding pre-IPO shares in names like Anthropic, Stripe, and xAI. The pattern is not opportunistic. It is a deliberate pivot toward becoming a multi-asset retail private markets destination — a business model that competes less with Wefunder or Republic than it does with EquityZen, Forge Global, and eventually, the retail alternatives products being built by JPMorgan and Blackstone.

What the SEC Filing Actually Shows

StartEngine’s 8-K, filed with the SEC on March 23, is sparse on financial detail by design. The filing notes that no pro forma financial statements are required because the acquisition does not exceed 20% significance under any of the three tests in Regulation S-X 1-02(w) — meaning Vinovest’s assets, revenue, and net income are each less than 20% of StartEngine’s equivalent figures at the time of closing. That threshold tells investors something useful: Vinovest is a small acquisition relative to StartEngine’s current scale, not a bet-the-company move. The strategic value of the deal is not Vinovest’s financials. It is Vinovest’s asset class, its 200,000 registered users, and the roughly $140 million to $150 million in fine wine and whisky it has secured on behalf of clients since its 2019 founding.

The share-based consideration structure also matters. By paying in stock rather than cash, StartEngine preserves its balance sheet at a moment when it is investing heavily in platform infrastructure — the secondary ATS, the Private product, and now Vinovest integration. It also aligns Vinovest’s founding team with StartEngine’s long-term performance. Brent Akamine, Vinovest’s co-founder and CEO, remains with the business as it operates as a wholly-owned subsidiary under its existing brand.

The Logic Behind Adding Wine to a Pre-IPO Platform

Howard Marks, StartEngine’s co-founder and CEO, offered the rationale directly in the acquisition announcement: “What stood out to me is how similar our communities are: investors looking for uncorrelated investments for their portfolios. Pre-IPO funds and wines are uncorrelated assets.” That framing is the strategic thesis in two sentences. StartEngine Private investors are already comfortable with illiquidity, long hold periods, and assets that do not trade on public exchanges. Fine wine and whisky occupy the same psychological space — patient capital seeking returns that do not move in lockstep with the S&P 500 — with the added dimension that the underlying asset is a physical good stored in a bonded warehouse, insured, and appreciating through a process that has nothing to do with interest rates or earnings revisions.

The uncorrelated returns claim deserves scrutiny, and it holds up under a modest one. Fine wine has historically shown minimal correlation with public equity markets during downturns — during the 2008-2009 crash, when broad equity indices fell more than 50%, major wine indices declined in single digits. Rare whisky has demonstrated similarly low correlation over the same periods, driven by supply dynamics — distillation cycles, aging requirements, and finite cask inventories — that are structurally disconnected from financial market cycles. These are not guaranteed return profiles, and the wine and whisky market has its own volatility drivers, including currency movements, collector demand cycles, and storage risk. But the asset class’s historical behavior in equity bear markets is the specific quality that makes it relevant to an investor who already holds concentrated exposure to early-stage private companies.

The Secondary Market Piece Nobody Is Talking About

The most underappreciated element of the Vinovest acquisition is what it enables on StartEngine’s existing secondary ATS. StartEngine operates an SEC-registered Alternative Trading System — the StartEngine Secondary marketplace — that allows investors to trade shares in private companies post-offering. As of the company’s most recent 10-K, over 400 issuers had signed up for the platform, though active quoting remained limited to a smaller cohort. The secondary market for private equity securities is genuinely difficult to build — thin liquidity, wide bid-ask spreads, and the coordination problem of matching buyers and sellers in thinly-held private assets.

Wine and whisky have a structural advantage over private equity shares in secondary markets: the underlying asset has an established global trading infrastructure, third-party valuation benchmarks, and a buyer base that extends well beyond financial investors into collectors, restaurants, and individuals who want physical delivery. Vinovest already operates a proprietary trading platform that allows investors to sell holdings or take physical delivery of bottles. Plugging that infrastructure into StartEngine’s ATS creates a secondary market where at least one asset class has genuine liquidity characteristics — and that working example of secondary market function could help validate and normalize the broader secondary offering for the harder-to-trade private equity securities alongside it.

This is the same thesis that animates Republic’s Mirror Token product — create a liquid or semi-liquid wrapper around an otherwise illiquid private market asset — but executed through physical goods and an established commodities trading infrastructure rather than tokenization. As our recent analysis of platform divergence noted, the crowdfunding platforms that are building toward durable private markets infrastructure have a structural advantage over those that remain primary campaign marketplaces. The Vinovest deal is StartEngine’s clearest move yet in that direction.

The Institutional Headwind Coming From Above

The competitive context for this acquisition is not other crowdfunding platforms. It is the institutional money moving down-market. J.P. Morgan Asset Management’s 2026 Global Alternatives Outlook, published in December 2025, described private markets as having “matured into a structural mainstay of global finance” and cited growing retail and retirement system participation as a primary demand driver. J.P. Morgan Private Capital, the firm’s venture and growth equity arm, expanded its team with senior hires in March 2026, explicitly citing the blurring boundary between public and private markets and the fact that companies are now staying private for a median of fourteen years before listing. Blackstone, Apollo, and KKR have all launched or expanded retail-accessible alternative investment vehicles in the past 18 months. These products carry institutional brand credibility, established track records, and distribution through major brokerage platforms that crowdfunding portals cannot match.

What StartEngine has that those products do not is a community. Its 2.1 million registered users were not acquired through a brokerage relationship or a 401(k) plan. They self-selected into a platform that makes private market investing feel accessible and participatory — closer to Robinhood than to a private bank. The Vinovest community of 200,000 wine and whisky investors is a similar profile: self-directed, alternative-minded, comfortable with physical assets and illiquidity. The combined user base is a distribution asset that institutional players have not figured out how to replicate, even as they invest billions in retail product development.

“Vinovest opens the door to a new category of alternative assets for our investors, while staying true to our mission of expanding access to private markets. What stood out to me is how similar our communities are: investors looking for uncorrelated investments for their portfolios. Pre-IPO funds and wines are uncorrelated assets.”

— Howard Marks, Co-Founder and CEO, StartEngine, press release, March 24, 2026

What Investors Should Actually Evaluate

The Vinovest acquisition is not a financial event that moves StartEngine’s near-term revenue in a meaningful way — the 8-K’s own significance thresholds confirm that. What it is, is a signal about the direction of the business, and that signal is worth taking seriously for investors evaluating either StartEngine itself or the broader private markets platform category.

StartEngine is a publicly traded company on its own platform under the ticker STGC, having completed a Reg A+ offering in 2021. Its shares trade on the StartEngine Secondary marketplace — which means the company is both an operator and an issuer in the same system, a structure that requires careful reading of disclosure documents and conflicts-of-interest language. Investors evaluating STGC should track the revenue contribution from StartEngine Private specifically, which generated 57% of 2024 revenue in its first full year of operation, alongside the secondary market’s active quoting growth over the next two to three quarters as Vinovest integration is completed.

For investors using StartEngine as a deal source rather than as a direct investment, the practical effect of the Vinovest acquisition is an expanded alternative asset menu with a different risk and return profile than early-stage equity. Fine wine and whisky holdings, managed by Vinovest’s curation team and stored in bonded warehouses, carry physical storage risk, valuation opacity relative to public securities, and hold periods that typically run four to ten years before optimal exit. They also carry the specific quality that Marks identified in his acquisition rationale: genuine non-correlation to the assets most sophisticated investors already hold in quantity.

What to Watch Next

- StartEngine Private revenue disclosure in next 10-K — The product generated 57% of 2024 revenue in its first full year. Whether that concentration grows or diversifies across the Vinovest integration and other product lines will be the clearest indicator of whether StartEngine is successfully building a multi-asset platform or remains a pre-IPO fund story with wine added around the edges.

- Secondary ATS active quoting growth — Over 400 issuers are enrolled on StartEngine Secondary but active liquidity remains thin. If Vinovest’s physical goods trading infrastructure helps normalize secondary market activity on the platform, it could materially change the liquidity narrative that has constrained all retail private market platforms.

- SEC Reg CF cap petition outcome — A formal petition to raise the Reg CF offering limit from $5 million to $20 million remains pending. If approved, it shifts the competitive advantage to platforms with the infrastructure and investor depth to handle larger, more complex raises — a category that favors StartEngine’s current build-out over open-access platforms that have not invested in comparable compliance and distribution infrastructure.

- Institutional retail alternatives expansion — JPMorgan, Blackstone, and Apollo are all actively expanding retail-accessible private market products. How quickly those products reach the self-directed investor through mainstream brokerage platforms will define how much runway StartEngine has before its community advantage is eroded by institutional distribution.

- Vinovest integration timeline — The acquisition closed on March 17, with Vinovest operating as a wholly-owned subsidiary under its existing brand. Whether StartEngine integrates Vinovest’s wine and whisky portfolios into the existing app experience — or keeps them as a separate destination — will determine how much of the 200,000 Vinovest user base actually converts to StartEngine platform engagement.

- Tokenization of Vinovest holdings — StartEngine has previously announced plans to tokenize real-world assets using ERC-1450 smart contract standards. Applying that infrastructure to Vinovest’s bonded warehouse holdings could create genuinely liquid, on-chain tradeable representations of physical wine and whisky — a product that would put StartEngine at the intersection of the RWA tokenization trend and the passion asset market simultaneously.