{kind=link}

The U.S. House of Representatives passed the Incentivizing New Ventures and Economic Strength Through Capital Formation Act — the INVEST Act — on December 11, 2025, by a vote of 302 to 123. The margin was bipartisan: all Republicans present voted for it, and 87 Democrats crossed the aisle. The bill then moved to the Senate, where it was referred to the Banking, Housing, and Urban Affairs Committee. As of mid-April 2026, no Senate action has been taken.

That gap between passage and enactment is where private market investors need to focus. The INVEST Act is not one bill — it bundles more than 20 individual pieces of legislation. Some provisions are procedural and largely administrative. Others, if they survive Senate markup intact, would represent the most significant statutory change to private capital access since the JOBS Act of 2012. Understanding which provisions matter and how they interact is the work that the headlines have largely skipped.

What the Bill Actually Contains

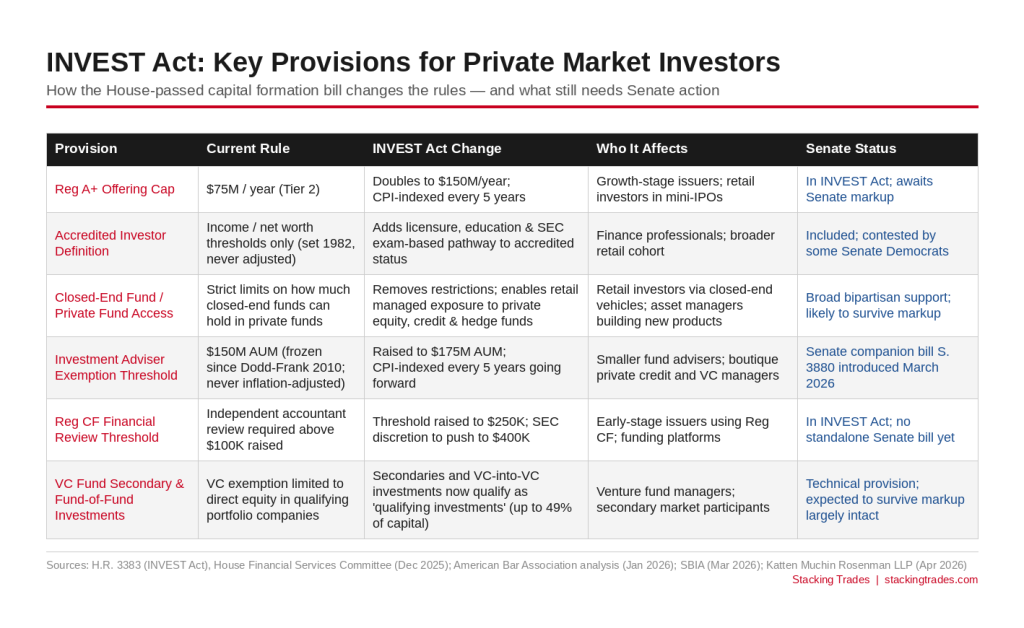

The INVEST Act touches four areas that matter directly to private market participants: Regulation Crowdfunding, the accredited investor definition, closed-end fund access to private funds, and the exemption thresholds for smaller fund advisers.

On Regulation Crowdfunding, the bill proposes raising the threshold at which issuers must provide reviewed financial statements from $100,000 to $250,000, with SEC discretion to push that floor to $400,000. It does not, notably, raise the overall $5 million annual Reg CF offering cap — that specific reform remains in a separate SEC petition process. The bill also separately includes the Regulation A+ Improvement Act, which would double the Tier 2 offering cap from $75 million to $150 million and add a CPI-linked inflation adjustment recalibrated every five years. As we have covered in detail, that cap has become a structural ceiling that drives mid-size issuers back into Regulation D and away from retail investors entirely.

The accredited investor definition change is arguably the most consequential provision for the investor side of the equation. Currently, the definition is anchored to wealth thresholds — $200,000 in annual income, $300,000 for couples, or $1 million in net worth excluding a primary residence — set in 1982 and never inflation-adjusted. The INVEST Act would add pathways based on professional licensure, education, and experience, and it would direct the SEC to create an exam-based route to accredited status. Anyone who passes a designated test could qualify, regardless of net worth. That change would open the accredited investor pool to a meaningfully broader segment of the professional class.

The closed-end fund provision removes existing constraints that limit how much registered closed-end funds can invest in private funds. Under current rules, a closed-end fund’s ability to own interests in private equity, private credit, or hedge funds is significantly restricted. The Increasing Investor Opportunities Act — folded into the INVEST Act — would relax those constraints, enabling asset managers to build closed-end vehicles that give retail investors managed exposure to private market strategies without the structural barriers that currently keep those strategies in institutional-only products.

The adviser threshold change — raising the Investment Advisers Act registration exemption from $150 million to $175 million in assets under management, with an inflation adjustment mechanism — is less visible to retail investors but operationally significant. As of March 2026, the companion Senate bill (S. 3880) had been introduced by Senators Ruben Gallego and Mike Rounds, signaling that at least some INVEST Act provisions are being pursued through parallel Senate channels even as the broader package awaits committee action.

The Venture Capital Reforms Practitioners Are Watching

The bill also expands the venture capital fund adviser exemption in ways that matter for fund-of-funds and secondary market participants. Currently, venture capital funds relying on the Section 203(l) exemption under the Advisers Act must invest primarily in direct equity positions in qualifying portfolio companies. The INVEST Act would direct the SEC to expand the definition of qualifying investments to include secondary transactions and investments in other venture capital funds — so long as those investments don’t exceed 49% of aggregate committed capital. Pure venture fund-of-funds would still not qualify for the exemption, but the change would allow individual VC funds to meaningfully expand their strategy without triggering full SEC adviser registration.

Related to this, the bill expands the Section 3(c)(1) exemption for venture funds, loosening the investment company registration requirements that currently apply to smaller venture vehicles. For investors participating in earlier-stage rounds through crowdfunding platforms or direct syndications that feed into venture structures, these mechanics determine how efficiently capital can be deployed and how cleanly it can be structured on the fund level.

The Senate Path Is Not Straightforward

The INVEST Act’s House passage was achieved partly through the breadth of the package — bundling provisions with disparate constituencies, from retirement plan sponsors who wanted collective investment trusts in 403(b) plans to private equity managers who wanted expanded venture exemptions. That breadth made it easy to assemble a 302-vote majority in the House. It also creates more surface area for the Senate to disagree on.

Senate Banking Committee Chair Tim Scott has championed capital formation legislation in prior sessions and holds the committee chairmanship, which is a favorable structural position for the bill. His committee is also the primary venue for the digital asset market structure bill, which has consumed much of the committee’s bandwidth through early 2026 as bipartisan negotiations continue. As of late March, the INVEST Act had generated no public Senate committee action beyond its referral.

The opposition in the House came primarily from Democrats worried about investor protection rollbacks. Senator Elizabeth Warren has previously voiced skepticism about reforms that expand retail access to private markets without commensurate disclosure requirements. That tension — between broadening investor access and ensuring those investors have adequate tools to evaluate what they’re buying — will define the Senate debate if and when the bill reaches the floor. Platform consolidation in crowdfunding has already exposed that divide: the market’s largest raises have concentrated in financial-sector vehicles that retail investors may be poorly equipped to evaluate.

What Passes May Look Different From What the House Sent

The most likely Senate outcome, if the bill moves at all, is a narrowed package. Provisions with the broadest bipartisan support — the adviser threshold adjustment, the closed-end fund private market access expansion, and parts of the accredited investor definition reform — have the clearest path. The Reg A+ cap increase and the more contested retirement plan provisions are more likely to be amended or stripped in markup.

Even the SEC under Chair Paul Atkins could move some of this territory independently. At the agency’s March 4, 2026 private credit roundtable, Atkins indicated support for the “reasonable retailization” of private markets and said the SEC has an obligation to expand pathways with “appropriate investor protections.” Several of the INVEST Act’s provisions — particularly around the accredited investor definition and certain Regulation D and A+ parameters — are within the SEC’s rulemaking authority to adjust without Congress. Whether the agency moves ahead of, alongside, or in lieu of legislation is an open question with real timing implications for issuers and investors.

The bill that signed the original JOBS Act in 2012 produced Regulation Crowdfunding, Regulation A+, and the expanded accredited investor pathway that now underpins the entire $5 million Reg CF market. A decade of regulatory and market experience has revealed where those frameworks work and where they don’t. The INVEST Act is an attempt at a second-generation fix. Whether it arrives in a form substantive enough to matter depends on a Senate committee that has more on its plate than at any point in the past decade.

“Capital formation is the engine of American economic growth. The INVEST Act makes several important improvements that will help millions of American investors succeed. When we broaden investment opportunities, make it easier for businesses to raise capital, make available more retirement plan options, and streamline disclosure practices, investors and markets benefit.”

— Eric J. Pan, President and CEO, Investment Company Institute, December 11, 2025

What to Watch Next

- Senate Banking Committee markup timeline — whether Chair Tim Scott brings the INVEST Act or individual component bills to markup in 2026, or whether the digital asset market structure negotiations continue to crowd it out. Any committee hearing notice is the signal that the calendar has cleared enough for action.

- SEC independent rulemaking on the accredited investor definition — Chair Atkins has indicated support for broader private market access. If the SEC moves via rulemaking before the Senate acts, some INVEST Act provisions become moot and the legislative path narrows to what only Congress can do.

- The Reg A+ cap doubling — the Regulation A+ Improvement Act is included in the INVEST Act package. If the Reg A+ provisions survive Senate markup intact, the Tier 2 cap rises from $75 million to $150 million, with CPI indexing. Watch for Senate amendments that propose a different number or strip the inflation mechanism.

- The Senate companion bill for the Small Business Investor Capital Access Act (S. 3880), introduced in March 2026 by Senators Gallego and Rounds — its progress is the clearest indicator of whether Senate Democrats are willing to support at least the adviser threshold provisions of the broader INVEST Act package.

- Parallel activity at the SEC on the Reg CF $5 million cap — the INVEST Act does not raise the annual Reg CF offering limit. A separate SEC petition remains under review. Issuers and platforms need both tracks to move before the Reg CF ceiling becomes the binding constraint on market growth.