s. The First Product Launches Will Show Whether the Pitch Holds.")

The policy architecture is nearly complete. The executive order was signed. The proposed rule is out for comment. The first product is already in the market. What is missing is the one thing that actually changes behavior: a Supreme Court ruling that tells plan sponsors they will not be sued for doing any of this.

Until that ruling arrives, the story of private credit entering America’s $14.2 trillion defined contribution market remains, at its core, a story about litigation fear dressed up as a product launch.

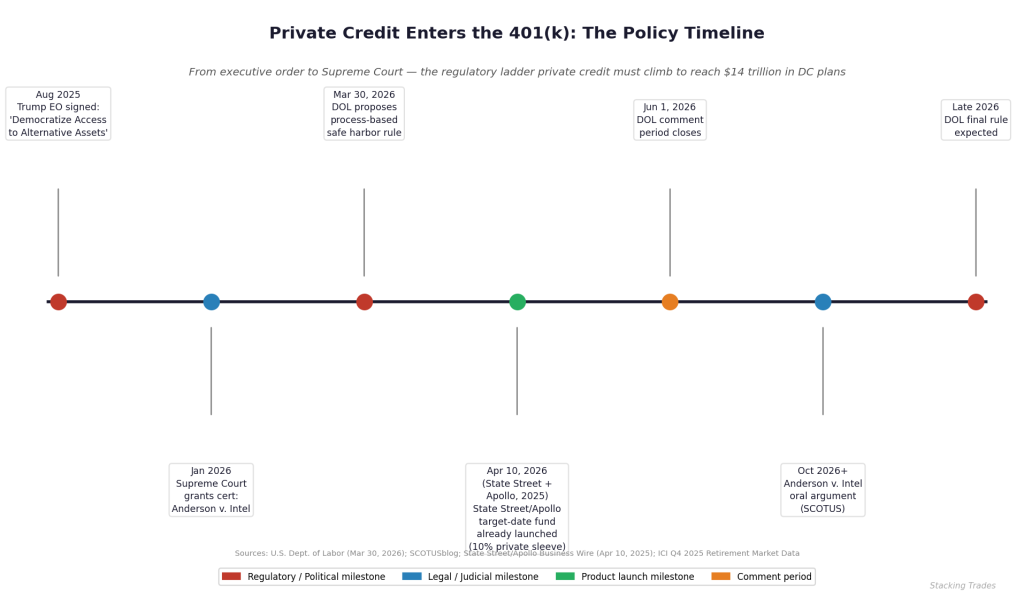

The Regulatory Ladder Has Been Built. The Last Rung Is in Court.

On August 7, 2025, President Trump signed an executive order directing the Department of Labor to ease restrictions on alternative investments in 401(k) plans. The DOL responded on March 30, 2026, releasing a proposed process-based safe harbor rule that would give fiduciaries a documented path to include private equity, private credit, real estate, and other alternatives alongside traditional fund menus. The comment period closes June 1.

“The department’s days of picking winners and losers are over. Our rule clearly spells out that managers must evaluate any and all potential product offerings by following a prudent process.”

— Keith Sonderling, Acting Secretary of Labor, March 30, 2026

The proposed rule identifies six factors fiduciaries must document when selecting alternatives: performance, fees, liquidity, valuation methodology, performance benchmarks, and complexity. Follow the process, and the rule creates a legal presumption of prudence. That presumption is the commercial unlock the industry has been waiting for since ERISA was passed in 1974.

But there is a complication sitting one floor above the regulatory stack. In January 2026, the Supreme Court agreed to hear Anderson v. Intel Corp., a case that asks whether ERISA plaintiffs must plead a “meaningful benchmark” to survive a motion to dismiss in fund underperformance cases. The case is scheduled for argument in the October 2026 term. A ruling favorable to plan sponsors would substantially raise the bar for the lawsuits that have historically kept private assets off 401(k) menus. A ruling the other way keeps that litigation risk alive regardless of what the DOL’s final rule says.

The First Product Is Already Live. Adoption Is Not.

State Street and Apollo were first out of the gate. In April 2025, State Street Global Advisors launched its Target Retirement IndexPlus Strategy, a collective investment trust that allocates 90% to public market index strategies and 10% to a private markets sleeve managed by Apollo. Shortly after, Great Gray Trust announced a comparable structure built in partnership with BlackRock, pairing BlackRock’s custom glidepath with private equity and private credit exposure at allocations ranging from 5% to 20% depending on participant age. BlackRock’s own research suggests adding private credit to a target-date structure could improve annual returns by roughly 50 basis points and generate 15% more assets over a 40-year savings horizon.

These are real products. They are in the market. But Morningstar’s analysis, published in early 2025, noted that as of that point, the only well-known firm to have launched something was State Street. BlackRock’s target date rollout for 401(k) plans was still being described as a first-half 2026 initiative. Empower, the second-largest U.S. retirement services provider, announced it would offer access to private investments in some workplace plans this year. The list of announced intentions is considerably longer than the list of plan sponsors who have pulled the trigger.

The reason is not ignorance of the product. Jaret Seiberg, financial services analyst at TD Cowen, put the obstacle plainly in a research note following the DOL’s March announcement: fiduciaries will remain skeptical until the courts have confirmed the proposed language actually protects them from litigation. “That means it could be several years before we see the real impact from this proposal,” Seiberg wrote. The history of ERISA litigation gives that caution a solid empirical basis. The Anderson v. Intel case itself involves a plan that included custom target-date funds with private equity exposure. The plaintiffs alleged imprudence based on underperformance, and the resulting litigation has now reached the Supreme Court.

The Number That Explains the Stakes

Total U.S. retirement assets reached $49.1 trillion as of December 31, 2025, according to the Investment Company Institute. Defined contribution plans, which include 401(k)s, held $14.2 trillion of that. Pension plans, which have faced none of the ERISA litigation constraints that govern participant-directed plans, have historically allocated roughly 16% of assets to private markets. If DC plans ever approach that allocation level, the math produces a capital flow of more than $2 trillion into an asset class that currently manages approximately $1.5 to $2 trillion in total direct lending volume globally.

Private credit managers have understood this arithmetic for years. Apollo, Blackstone, Ares, and Blue Owl have each built or acquired retail distribution infrastructure aimed at bringing credit products to non-institutional investors. Blackstone’s credit and insurance segment reached $432 billion in assets under management as of Q3 2025. Apollo’s private credit AUM stood at $723 billion as of the same period. These firms are not waiting for the regulatory outcome to position themselves — they are already at the table. The open question is which recordkeeping platforms and plan sponsors will go first, and on what timeline, once the DOL’s final rule and the Supreme Court’s Anderson decision are both in hand.

What the industry has not yet seen is a named first-mover product announcement from a major recordkeeper — a Fidelity, Vanguard, or large insurance platform committing to a specific private credit sleeve inside a target-date or managed account structure at scale. The State Street and BlackRock/Great Gray launches are meaningful. But neither Fidelity nor Vanguard, which together manage the largest share of defined contribution assets, has made that announcement. When one of them does, the conversation shifts from policy to practice in a way that none of the regulatory milestones alone can accomplish.

The Comment Period Is the First Real Signal

The DOL’s proposed rule on Federal Register attracted over 37,000 comments before the June 1 close — a volume the agency has not seen since the Biden-era Retirement Security Rule. The breadth of the response reflects how much is at stake. Private fund managers, plan sponsors, labor unions, and consumer advocacy groups all submitted substantive comments. Senator Elizabeth Warren opposed the rule directly, arguing it exposes retirement savers to unnecessary risk. The Managed Funds Association and the American Retirement Association expressed support, with ARA characterizing the proposal as “continuity of, not a departure from, the established ERISA fiduciary framework.”

The final rule is expected by the end of 2026. Whether that timeline holds, and whether the rule survives the legal challenges that accompanied the Biden DOL’s fiduciary rulemaking, will determine how quickly the product pipeline actually reaches participants. For investors watching this space, the comment volume is less interesting than the comment quality. The most consequential submissions will be from major plan sponsors and recordkeepers describing what explicit protections would change their behavior. Those comments are the blueprint for the final rule’s most commercially relevant provisions.

What to Watch Next

- The DOL’s response to the comment period after June 1 — specifically whether the agency adds an explicit litigation safe harbor or narrows the six-factor test in response to legal challenges anticipated from consumer groups. That language will determine whether major plan sponsors treat the rule as actionable guidance or wait for further judicial clarity.

- Anderson v. Intel oral argument, scheduled for the Supreme Court’s October 2026 term. A ruling that raises the bar for ERISA fund-underperformance claims would be the single most consequential event for accelerating DC plan adoption of alternatives — more so than any regulatory guidance the DOL can issue on its own.

- BlackRock’s Great Gray target-date fund adoption metrics. BlackRock has described the first half of 2026 as the rollout window. Any disclosure of plan sponsor commitments or participant enrollment numbers will provide the first real-world test of whether early-mover demand matches the industry’s projections.

- Whether Fidelity, Vanguard, or a major insurance-platform recordkeeper announces a specific private credit sleeve in a managed account or target-date structure. That announcement has not happened yet and remains the most direct signal that the category has crossed from policy debate to mainstream practice.

- Private credit market conditions through H2 2026. Evergreen private credit funds held $644 billion in assets as of mid-2025. Any meaningful softening in credit quality — particularly in middle-market direct lending, where most DC-accessible products are concentrated — would give both regulators and plan sponsors new grounds for caution before the Anderson ruling arrives.