OpenAI spent the better part of three years telling the world it was building a consumer revolution. Now, with a potential IPO as early as the fourth quarter of this year, it is telling a different story — one its investors, underwriters, and institutional buyers are far more comfortable with.

The shift became official on March 16, when Fidji Simo, OpenAI’s CEO of Applications, held an all-hands meeting with employees to outline a new strategic direction. Simo told staff the company needed to stop being distracted by “side quests” and pivot aggressively toward coding and business users. The Wall Street Journal reviewed a transcript of the meeting and reported the details first. CNBC confirmed that OpenAI could debut on public markets as soon as Q4 2026, though the timing remains subject to change.

The pivot is real. But so is the audience for it.

The IPO Machine Is Already Running

CFO Sarah Friar has been expanding the finance team in preparation for public market scrutiny, hiring Ajmere Dale, former chief accounting officer at Block, and Cynthia Gaylor, the former CFO of DocuSign, who will oversee investor relations.

OpenAI has also retained Wilson Sonsini Goodrich and Rosati — the law firm that managed Google’s 2004 IPO and LinkedIn’s 2011 listing — for IPO preparations. These are not the moves of a company still deciding whether to go public. They are the moves of a company on a clock.

The pressure behind that clock is partly competitive. OpenAI executives have privately expressed concern about Anthropic listing first. Both companies are preparing S-1 filings for the second half of 2026, and the first to list will set AI valuation benchmarks for public investors and capture pent-up retail demand.

A Product Story Built for Institutional Buyers

ChatGPT now supports more than 900 million weekly active users, and the company is framing the enterprise transition as a natural next step: convert that base into high-compute users by making ChatGPT a productivity tool.

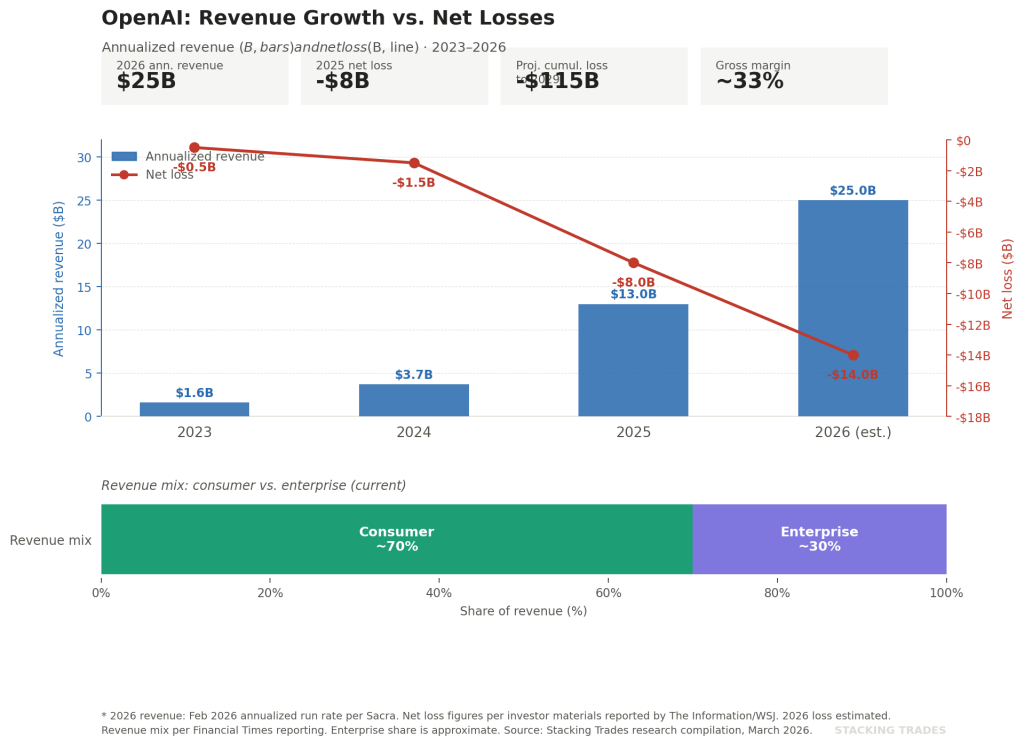

The consumer business remains the engine. Consumer subscriptions account for approximately 70% of OpenAI’s revenue base, per the Financial Times. The enterprise gap relative to Anthropic is what Simo’s pivot is designed to close.

The contrast with Anthropic is worth understanding. Anthropic has built its revenue model almost entirely on enterprise and API customers — coding tools, developer integrations, and corporate deployments that generate predictable, contract-backed cash flows. Public market investors historically assign higher multiples to that revenue profile. OpenAI’s consumer dominance is extraordinary, but subscription churn, pricing sensitivity, and competition from Google and Meta make it a harder story to tell at a valuation that currently implies more than 100 times trailing revenue.

Reuters reports OpenAI is in advanced talks with TPG, Advent International, Bain Capital, and Brookfield to create a new joint venture valued at around $10 billion that would push its enterprise products through PE-backed portfolio companies across industries. The company has also announced “Frontier Alliances” with McKinsey, BCG, Accenture, and Capgemini. The architecture of those partnerships is less about product adoption and more about distribution credibility before a roadshow.

“Every piece of news coming out of OpenAI right now is part of a jigsaw puzzle. There is one audience for this final picture — the bankers and institutional investors who will price the offering.“

— Om Malik, om.co, March 17, 2026

The Numbers Investors Will Actually Read

Sacra estimates that OpenAI hit $25 billion in annualized revenue in February 2026, up from roughly $20 billion at the end of 2025, driven by rising adoption across both consumers and enterprise customers. Paying business users surpassed 9 million as of February 2026, up from 5 million in August 2025.

Those are genuinely strong numbers. The problem is what sits beside them.

OpenAI recorded an $8 billion net loss in 2025. Internal projections reviewed by investors suggest cumulative losses through 2029 could reach $115 billion, with profitability not expected before the early 2030s. The company has also recalibrated its infrastructure spending target, telling investors it is now targeting roughly $600 billion in total compute spend by 2030 — down from the $1.4 trillion figure Altman had circulated previously.

Gross margins sit around 33%, constrained by inference costs that reached $8.4 billion in 2025 and are projected to rise to $14.1 billion in 2026. That is not a margin profile that supports a 100x revenue multiple without an unusually compelling narrative about what the business looks like in five years.

OpenAI projects total 2030 revenue exceeding $280 billion, with consumer and enterprise contributing roughly equally. Public investors will have to decide how much weight to give projections that stretch nearly a decade forward and depend on market conditions no one can reliably model.

The Valuation Question No One Can Answer Yet

OpenAI raised $110 billion in new funding from Amazon, Nvidia, and SoftBank, completed on February 27, 2026 — one of the largest private capital raises in technology history. That round sets the implied baseline that an IPO must either validate or exceed.

The scale of what could hit public markets this year is genuinely without precedent. PitchBook estimated that if OpenAI, Anthropic, and SpaceX each float 15% of their shares, the combined sum would roughly equal the total raised across all American IPOs over the prior several years.

That concentration is itself a risk factor. If the largest AI IPO in history prices poorly, it does not just hurt OpenAI shareholders — it recalibrates how public markets price the entire sector.

WHAT TO WATCH NEXT

- The S-1 filing. Everything disclosed above comes from investor materials, secondary reporting, and company statements. The actual prospectus will reveal customer concentration, revenue recognition details, Microsoft’s revenue-sharing terms, and the risk factors OpenAI’s own lawyers have identified.

- Anthropic’s timing. If Anthropic files before OpenAI, it sets the comparable. If OpenAI files first, it controls the narrative. The sequence matters.

- Enterprise revenue mix at IPO. Watch for whether business users as a share of total revenue has moved meaningfully from roughly 30% before the roadshow begins.

- The rate environment. The FOMC held rates at 3.5–3.75% on March 18 while signaling ongoing inflation concerns. A high-rate environment compresses growth stock multiples. A 100x revenue valuation is considerably harder to sustain if the 10-year holds above 4.5%.

- Any SEC comment letters. Confidential S-1 review processes often surface material disclosure issues that reshape the public filing significantly.