For the first two months of 2026, the IPO market looked like it was finally ready to deliver on years of built-up expectations. Institutional investors talked openly of a booming listings environment. A deep backlog of private companies — OpenAI, SpaceX, Databricks, Kraken, Canva — had all been positioning for public debuts. Rate cuts were on the calendar. The window, by every measure, was open.

Then the U.S. and Israel attacked Iran.

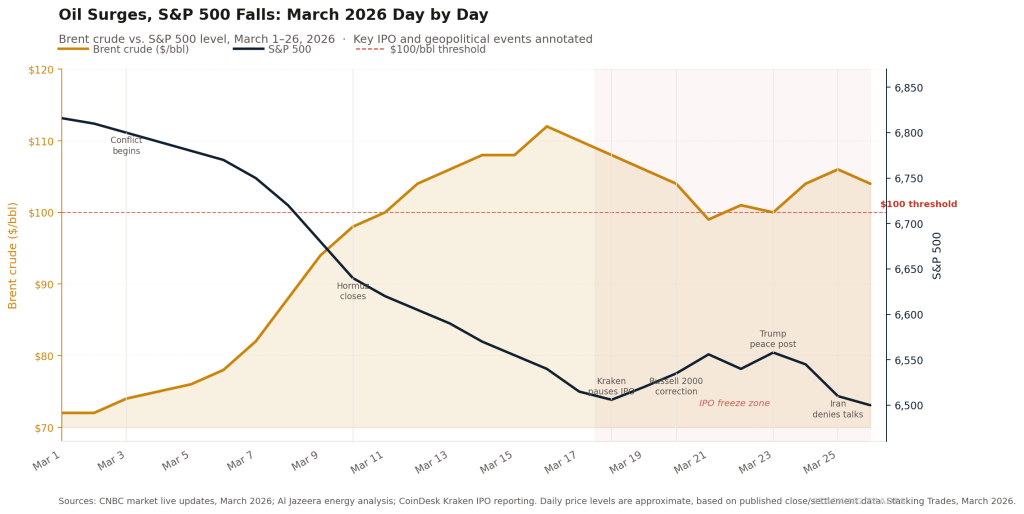

From March 3 to March 20, the S&P 500 fell from 6,816 to 6,506 — a decline of approximately 4.55%. The Russell 2000 slipped into correction territory on March 20, becoming the first major U.S. benchmark to confirm a 10% decline from its recent peak. Brent crude futures spiked more than 50% since the conflict began, while the Dow posted four consecutive weeks of losses.

The IPO pipeline didn’t just slow. It stopped.

What the Conflict Did to Oil — and What Oil Did to Markets

The mechanism is not complicated. Iran’s closure of the Strait of Hormuz — a waterway that carries approximately 20% of the world’s oil supply — forced Gulf producers to curtail output as storage capacity ran out. The International Energy Agency assessed it as the largest supply disruption in the history of the global oil market, with flows through Hormuz collapsing from 20 million barrels per day to a trickle.

At their peak, Brent crude futures topped $112 per barrel after Iraq declared force majeure at all foreign-operated oilfields and drones struck two refineries in Kuwait. Oil above $100 is not merely an energy story — it is an inflation story, a rate story, and ultimately a risk premium story.

The Federal Reserve, already cautious, struck a hawkish tone in March, projecting higher inflation and signaling only a single rate cut for all of 2026 — down from the two cuts investors had been pricing before the conflict began. With rate cuts off the table and inflation re-accelerating, the calculus for pricing a growth company at a high multiple collapsed almost overnight.

Kraken Blinked First

The most concrete evidence of the IPO freeze came on March 18, when Kraken’s parent company Payward quietly shelved its listing plans. Kraken had confidentially filed with the SEC in November 2025, raised $800 million at a $20 billion valuation — including a $200 million commitment from Citadel Securities — and had been positioning for one of the most closely watched crypto debuts in years.

Sources told CoinDesk the company is still considering an IPO but probably not until market conditions improve.

The timing mattered. Eleven crypto companies raised $14.6 billion through public offerings in 2025, up sharply from $310 million the prior year. But many had since underperformed. Circle’s shares had dropped more than half from their peak. BitGo, the only crypto firm to go public in 2026, had seen its stock fall 44% since listing in January. Kraken looked at that evidence and decided a discounted debut was worse than no debut at all.

It was not alone. In India, over 160 companies holding regulatory approvals for approximately $17.2 billion in listings paused their plans. The most high-profile casualty was PhonePe, the Walmart-backed fintech, which put its $1.3 billion public issue on hold despite an internal valuation target of $9 to $10 billion.

“The war in Iran and the resulting surge in oil prices continue to dampen risk appetite. Any sustainable market recovery will require meaningful progress toward a peace agreement and a reopening of the Strait of Hormuz.”

— Adam Turnquist, Chieft Technical Strategist, LPL Financial, March 26, 2026

The Whipsaw Market That Makes Pricing Impossible

What has made Q1 2026 particularly brutal for deal-makers is not just the direction of markets — it is the volatility. On March 23, Trump announced via social media that the U.S. and Iran had held “very good and productive conversations.” Oil fell sharply and stocks soared. Iran’s foreign minister immediately denied any direct talks. Markets retreated. The following week, Trump offered Iran a 15-point peace plan, oil dipped below $100, and the S&P 500 ripped 1% higher. Iran’s state media dismissed the plan. Oil climbed back above $104.

PNC Financial’s chief investment strategist Yung-Yu Ma described the environment plainly: “There’s just so much uncertainty now, it’s very difficult for investors to position around what look like binary events that could come down to the wire.”

For an investment bank trying to price a roadshow — or a CFO deciding whether to file an S-1 — that environment is effectively unworkable. Valuation depends on comparable multiples, and multiples are moving 3–5% on a single social media post.

What History Says — and Why This Time Is Different

The natural instinct is to reach for historical precedent. Geopolitical shocks have historically been buying opportunities. Ed Yardeni of Yardeni Research acknowledged the pattern but drew a distinction: “Greenland was a sideshow. Venezuela was a sideshow. Cuba is a sideshow. This is about as big as it gets.”

Al Jazeera’s analysis of the energy markets highlighted a structural difference from 2022: when Russia invaded Ukraine, the global system absorbed the shock through rerouting and substitution. The Hormuz closure, by contrast, is a physical chokepoint — it obstructs not just trade routes but the very ability of producers to export. Unlike sanctions-driven disruptions, it cannot be compensated for through market mechanisms alone.

That distinction matters for IPO timing. If the Hormuz closure is structural — dependent on a ceasefire that has not materialized — the rate and inflation pressure it creates could persist well into H2 2026, compressing the window that issuers had been counting on.

WHAT TO WATCH NEXT

- Strait of Hormuz reopening. This is the single variable that moves everything else. Every peace negotiation signal has caused immediate market relief; every denial has reversed it. Watch for a formal ceasefire framework, not just social media diplomacy.

- SpaceX S-1 timing. Reports suggest SpaceX may file IPO paperwork within days. If it proceeds in this environment, the pricing and reception will be the most consequential data point for the broader 2026 IPO pipeline.

- Fed language in May. Macquarie has argued the Fed’s next move could be a rate hike, pushed to H1 2027, if energy-driven inflation persists. Any shift in Fed language at the May meeting would either open or further close the IPO window.

- India’s Q3 pipeline. Indian market experts suggest the IPO window may gradually reopen toward Q3 2026, once the geopolitical shock is absorbed. The U.S. timeline is likely to track a similar arc.

- Kraken’s next move. The company still has its confidential filing in place and will be among the first major issuers to signal whether conditions have normalized. Watch for any bank engagement or roadshow preparation news.