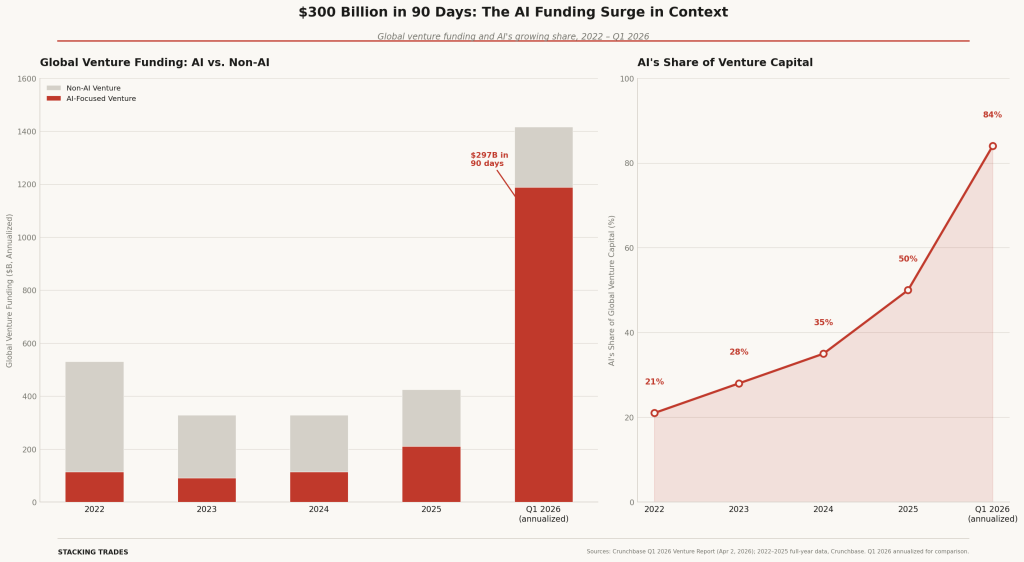

The first quarter of 2026 produced a number that no historical framework was built to absorb. Investors deployed $297 billion into roughly 6,000 startups globally between January and March, a sum that exceeds every full-year venture total before 2018 and equals nearly 70% of all capital deployed across the entirety of 2025. Call it what you want. The scale is without precedent.

The question sophisticated investors are asking is not whether the number is real. It is. The question is whether the capital concentration underlying it reflects rational conviction or the architecture of a crash in slow motion. The evidence, weighed carefully, tilts toward the former.

$297B

81%

$19B

Global VC deployed

Q1 2026 (Crunchbase)

Share flowing to

AI companies

Anthropic annualized

run rate, March 2026

Four Companies, $186 Billion, and the Case for Concentration

The headline figure is dominated by four rounds. OpenAI closed a $122 billion raise that pushed its valuation to $852 billion. Anthropic added $30 billion at a $380 billion post-money valuation. Elon Musk’s xAI pulled in $20 billion. Waymo secured $16 billion. Those four deals alone totaled $188 billion, or roughly 64% of all global venture activity for the quarter.

Critics have reached immediately for the word “concentration” as a synonym for fragility. That reading misses the structural logic. The AI buildout is not a software story in the old sense. It is simultaneously a compute story, an infrastructure story, and an energy story. Capital requirements of this magnitude are not a sign of speculation; they reflect the genuine cost of building systems that will underpin the next generation of enterprise software. These are not companies with a pitch deck and a domain name.

Early-stage funding grew 41% year-over-year, to $41.3 billion across 1,800 deals. Seed funding rose 31%. The ecosystem is not hollowing out below the megarounds. Every stage grew. The money at the top is not crowding out the next generation; it is pulling it forward.

The Revenue Underneath the Valuations

The most durable rebuttal to bubble-talk is not the funding numbers. It is the revenue curve. Anthropic’s annualized run rate hit $14 billion in February 2026, confirmed in the company’s own Series G disclosure. By March, that figure had crossed $19 billion, up from $9 billion at the end of 2025 and $1 billion in December 2024. That is not a valuation story. That is a sales story.

The growth rate has no precedent in enterprise software. More than 500 of Anthropic’s customers now spend over $1 million annually, and eight of the Fortune 10 are active Claude users. Anthropic now captures over 73% of spending from companies buying AI tools for the first time, a figure that stood at 40% just ten weeks prior. Enterprise adoption is not a lagging indicator here. It is the leading one.

“AI in 2026 is a story of capital building in silicon and steel, and in genuine utility. The doomsayers are making this millennium’s most expensive error: mistaking the most significant digital infrastructure overhaul for a speculative fantasy.”

— Sify Technologies analysis, January 2026

OpenAI, meanwhile, is running at an annualized revenue rate of approximately $25 billion, according to reporting from The Information. Epoch AI’s analysis projects that Anthropic could surpass OpenAI in annualized revenue by mid-2026 if current trajectories hold, a crossover that would represent one of the fastest competitive market shifts in enterprise software history.

This Is Not the Dot-Com Bubble. The Infrastructure Comparison Matters.

The dot-com analogy is the most repeated frame in AI skeptic commentary, and it is also the least instructive one. Pets.com raised money on a business model with no path to unit economics. Webvan tried to deliver groceries before the logistics existed. The companies absorbing the majority of Q1’s capital are generating tens of billions of dollars in annual revenue from paying enterprise customers. The comparison collapses on contact with the facts.

What the dot-com era did share with today is that transformative infrastructure buildouts look irrationally expensive until they don’t. Every fiber optic cable laid in the late 1990s that made the broadband internet possible looked like waste at the time. The waste was real. So was the infrastructure. The companies that built the physical layer of AI — data centers, specialized chips, power infrastructure — are creating assets that will be productive for decades regardless of which model wins the next benchmark.

Goldman Sachs estimates that AI capex now represents approximately 0.8% of GDP, still nearly half the 1.5% of GDP reached during comparable tech booms over the past 150 years. The cycle, by that measure, has more room to run before the historical warning signs activate.

Where the Legitimate Risks Sit

Acknowledging the bull case does not require pretending there are no risks. There are, and serious investors should hold both simultaneously.

The venture concentration is real. If three companies account for the lion’s share of a quarter’s capital, the health of that quarter is hostage to the health of those three companies. A major regulatory shock, a security incident, or a model capability plateau at any of the frontier labs would register not as a sectoral speed bump but as a funding crisis. The interdependencies run deep.

The exit environment remains thin. Only four US venture-backed companies exited above $1 billion in Q1 via IPO, against a backdrop of surging valuations and enormous unrealized paper gains sitting on LP balance sheets. The IPO market has not yet reopened at a scale commensurate with the private market’s ambitions. That gap will not close on its own.

Morgan Stanley’s strategists, in a February 2026 note, said plainly that “the AI buildout has become so large — and so well understood — that it no longer supports paying any price for the companies driving it.” That is a useful discipline for public market investors. It is also, notably, a statement about pricing discipline, not about whether the underlying technology or its commercial potential is real.

Unlike Any Previous Cycle

What distinguishes the current moment from prior technology booms is not just the dollar figures. It is the physical dimension of the investment. Capital is flowing into autonomous vehicles, robotics, and manufacturing alongside model development. The AI boom is simultaneously a software cycle and an industrial cycle, with capital requirements that match. That duality is new.

The secondary market for private stakes in AI companies is also maturing rapidly, with $240 billion in secondary transaction volume in 2025 and projections approaching $300 billion for 2026. Liquidity mechanisms that did not exist two years ago are creating pricing signals and investor discipline that help distinguish genuine value from hype at the asset level. The private market is developing its own immune system.

Q1 2026 will be studied for a long time. The more interesting question is whether the revenue growth that underlies these valuations continues to outpace the capital being deployed into them. So far, the answer is yes. That is the number to watch.

WHAT TO WATCH NEXT

- SpaceX’s public S-1 filing. The confidential filing is done. The public prospectus — expected roughly eight weeks later — will be the first hard look at the revenue and cost structure of the largest IPO ever attempted, and will test whether public markets can absorb AI-era private valuations at scale.

- OpenAI and Anthropic revenue pacing through Q2. Epoch AI projects a potential revenue crossover between the two companies by mid-2026. Whether that materializes — and how publicly either company discloses it — will be a significant signal for private market pricing across the sector.

- The IPO backlog. Only four US companies exited above $1 billion via IPO in Q1. The pressure on GPs to return capital to LPs is intensifying. Watch whether the SpaceX listing, if it proceeds, creates a window for other high-profile AI-adjacent companies to follow.

- Enterprise AI spend in Q1 earnings. The hyperscalers report Q1 earnings in late April. Any softness in cloud revenue or AI-related guidance will test whether enterprise adoption is accelerating as fast as the private market assumes.

- Secondary market pricing. As dry powder in dedicated secondary strategies approaches $327 billion, pricing premiums or discounts on AI company stakes will serve as the most honest real-time valuation signal available outside of a formal IPO.