Most earnings calls handle tariffs the same way: acknowledge the headwind, cite mitigation, decline to put a firm number on it. That language has been useful for investor relations departments navigating genuine uncertainty, but it has also obscured something that sophisticated investors can now actually measure. A handful of companies have been unusually specific — and the differences between how they are accounting for tariff exposure are not just interesting as disclosure strategy. They are a window into margin trajectories, pricing power, and supply chain positioning that will separate winners from laggards in the back half of 2026.

The legal landscape that sits beneath those disclosures shifted dramatically on February 20. The U.S. Supreme Court ruled 6-3 in Learning Resources, Inc. v. Trump that the International Emergency Economic Powers Act does not authorize the President to unilaterally impose tariffs, striking down the broad reciprocal tariff regime that had been in place since early 2025. Hours after the ruling, the administration announced a 10% global tariff under Section 122 of the Trade Act of 1974, later raised to 15%, and launched Section 301 investigations into more than a dozen trading partners to rebuild tariff authority through a different statutory path. The Penn Wharton Budget Model estimated up to $175 billion in potential IEEPA refunds to importers, a figure that has not yet flowed through the system and remains mired in procedural complexity at the Court of International Trade.

The result is a situation where total tariff exposure varies enormously by company, where the refund opportunity exists in theory but not yet in practice, and where the 15% Section 122 tariff — due to expire July 24, 2026 unless replaced — introduces a second layer of planning uncertainty. Reading what each company is actually saying in its filings is now more analytically useful than any macro-level tariff commentary.

P&G: The Company That Counted Everything

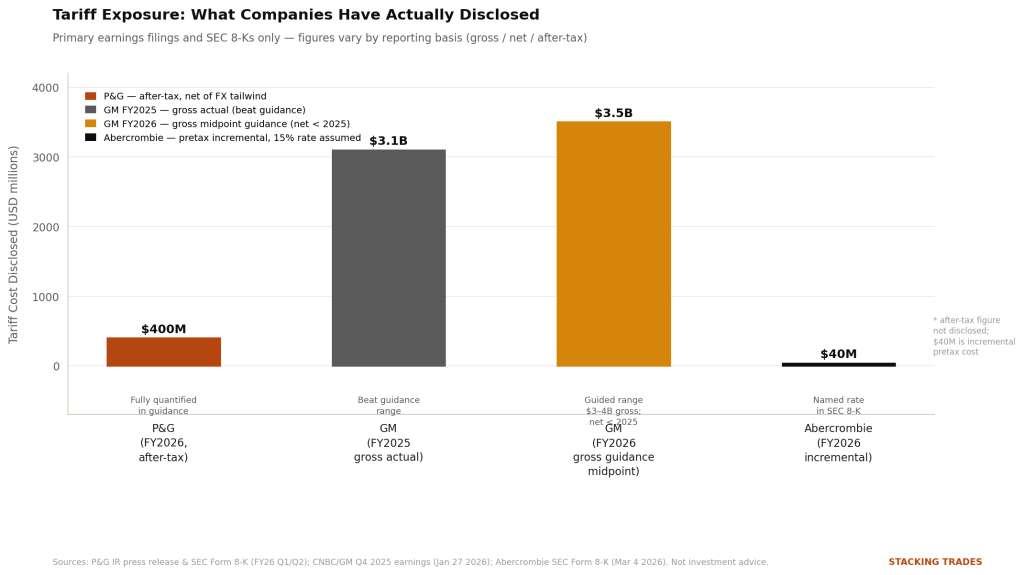

Procter & Gamble set the standard for tariff disclosure transparency. In its fiscal Q4 2025 earnings release in July 2025, the company disclosed a roughly $1 billion pretax hit from tariffs for fiscal year 2026, broken down by geography: approximately $200 million from Chinese trade, $200 million from Canadian imports, and $600 million from the rest of its global footprint, according to CFO Andre Schulten. That total was subsequently revised downward as the IEEPA tariffs were struck down. As of P&G’s most recent quarterly filing with the SEC, the updated tariff headwind stood at approximately $400 million after-tax for fiscal 2026, equating to a $0.19 per-share drag on core EPS growth.

What makes P&G’s disclosure particularly useful is the specificity of both the number and the mitigation response. The company raised prices on roughly a quarter of its product items in response to tariffs, and Schulten framed the strategy publicly as a multi-lever approach: sourcing flexibility, productivity improvements, and pricing with innovation. That transparency gives analysts and investors a clean basis for modeling margin recovery, rather than simply estimating it. P&G’s stock reaction to its updated tariff guidance has been measured precisely because the number was already known; there was no discovery risk in subsequent quarters.

GM: The Offset Playbook

General Motors took a different approach, and it has so far proven more effective as a capital markets strategy than the headline exposure would suggest. The automaker absorbed $3.1 billion in tariff costs in 2025, below its own guidance range of $3.5 billion to $4.5 billion, with CFO Paul Jacobson citing footprint adjustments and cost reduction initiatives that offset more than 40% of gross tariff costs. For 2026, GM guided to gross tariff costs in the $3 to $4 billion range — slightly higher than 2025 in gross terms — but simultaneously guided to net tariff costs below 2025 levels once offsets are factored in.

The distinction between gross and net tariff exposure is the most important analytical separation in how companies are reporting. GM is also projecting $500 million to $750 million in regulatory savings from policy shifts under the current administration, narrower EV losses of $1 billion to $1.5 billion from reduced production volumes, and a broader supply chain restructuring that shifts more domestic content into its highest-margin vehicles. Jacobson told investors in February that the company was “impacted pretty heavily by tariffs” but was tracking to restore North American margins to the 8% to 10% range roughly 12 to 18 months ahead of where most investors had modeled the recovery. That framing — tariffs acknowledged, quantified, and being actively neutralized — drove a stock reaction that treated the tariff number as manageable rather than alarming.

“We should end up at a position where our net tariffs are actually lower in 2026 than they were in 2025.”

– Paul Jacobson, CFO, General Motors, Q4 2025 Earnings Call, January 27, 2026, via CNBC

Abercrombie: The Company That Named a Rate

Abercrombie & Fitch did something most companies deliberately avoid: it put a specific tariff rate assumption into its official fiscal 2026 guidance. The company’s Q4 2025 earnings release, filed as a Form 8-K with the SEC on March 4, stated that its outlook includes the estimated impact of a 15% tariff on all goods imported into the United States, based on the February 21, 2026 announcement, assumed to be in effect for the entirety of fiscal 2026. The company quantified this at approximately $40 million in incremental tariff expense, translating to roughly 70 basis points of full-year margin impact, front-loaded in Q1 at 290 basis points before lapping comparables.

CFO Robert Ball elaborated on the earnings call that the company was not planning significant price increases, had taken steps to avoid moving prices in a way that would damage customer value perception, and had structured its guidance to reflect the 15% assumption holding through the back half under Section 122 or a successor mechanism. That clarity comes with its own risk: if tariffs change materially — either through the Section 301 investigations or an expiration of Section 122 without a replacement — Abercrombie’s guidance becomes stale faster than a company that left the rate assumption out entirely. But for investors modeling the stock, having an explicit rate in the guidance removes a major source of uncertainty that competitors left in place.

Dollar Tree: The Refund Nobody Is Counting

The contrast is sharpest with Dollar Tree. CFO Stewart Glendinning told investors the company had already paid tariffs on its current inventory before the Supreme Court ruling and would not be treating any potential IEEPA refund as a planning assumption. His exact framing: the company remains cautious because of the potential for further near-term policy changes and because of freight and other cost pressures related to the conflict in the Middle East. Dollar Tree explicitly excluded potential IEEPA refunds from its guidance.

That conservatism is procedurally defensible. The IEEPA refund process is genuinely uncertain. The Court of International Trade ordered CBP to begin paying refunds on March 4, then suspended the immediate compliance requirement on March 6 while CBP builds a new automated processing system — CAPE — that it estimated would take 45 days to stand up. PwC’s analysis of the ruling noted that more than $170 billion in IEEPA-related tariffs had been collected, but that the pathway to refunds depends on further court proceedings and administrative guidance that remain unresolved. For a mass-market retailer with millions of low-cost imported items, inventory already sold means the economic benefit of a refund may not flow back to the importing entity in any meaningful timeframe.

The gap between Abercrombie’s named-rate transparency and Dollar Tree’s refund agnosticism illustrates the range of disclosure postures currently in play across retail alone. Neither is wrong. But they create very different analytical problems for investors trying to build accurate forward models.

What the Divergence Actually Signals

The companies with the most transparent tariff disclosures tend to share two structural characteristics. They have either already absorbed most of the cost and can speak to it with precision, or they have significant pricing power that makes the pass-through math workable enough to discuss publicly. P&G can quantify its tariff hit because it has already executed price increases on a quarter of its product line and can model the margin recovery. GM can describe a net improvement because it has enough supply chain flexibility and regulatory offset capacity to close the gap between gross and net exposure.

Companies with less transparent disclosures often face one of two different problems: either they genuinely do not know what the final rate environment will look like — a defensible position given that Section 301 investigations are now underway against more than a dozen trading partners — or they lack the pricing power or supply chain agility to offer a credible mitigation story alongside the gross number. Retailers with thin margins and East Asian sourcing concentration, where the prior IEEPA reciprocal rates were highest, fall into the latter category. For those companies, the 15% Section 122 rate is lower than what they faced six months ago, but Section 301 outcomes could restore or exceed those rates within 12 to 18 months.

For investors, the first-order question is not which companies face tariff exposure — virtually every company in consumer goods, autos, apparel, and electronics does. It is which companies have been specific enough in their disclosures to allow accurate forward modeling, and whether the specificity reflects genuine confidence in their mitigation capacity or simply better investor relations management. The two are not always the same thing.

WHAT TO WATCH NEXT

- CBP’s CAPE system launch — the Consolidated Administration and Processing of Entries system was estimated to be ready approximately 45 days from March 6, placing a target around April 20. When it goes live, companies with significant IEEPA exposure will face a decision about whether to recognize a refund receivable in their next quarterly filings, a disclosure event that will move stocks in sectors that have been conservative.

- Section 301 investigation timelines — the Trump administration launched investigations against more than a dozen trading partners after the IEEPA ruling. Historical Section 301 timelines run 6 to 18 months before implementation, meaning new country-specific tariffs could arrive in Q4 2026 or Q1 2027. Companies currently guiding on 15% Section 122 rates may need to revise once those outcomes become clearer.

- Section 122 expiration on July 24, 2026 — the current 15% global tariff is a 150-day temporary measure. What replaces it — whether through Section 301 outcomes, bilateral deals, or a new executive mechanism — will reset the tariff planning assumption for virtually every U.S. importer. Q2 earnings calls in July will be the first reporting cycle where companies must address the post-July 24 environment.

- P&G’s next quarterly update — the company’s fiscal Q3 2026 results, expected in late April, will show whether the $400 million after-tax tariff headwind is tracking as modeled and whether the pricing actions taken on a quarter of its product items are holding volume without demand destruction.

- Abercrombie’s Q1 2026 results — the company guided explicitly to 290 basis points of Q1 margin pressure from tariffs. That specific, quantified forecast creates a precise test: if Q1 operating margins land near that guidance, it confirms the modeling. If they miss on the tariff line, the named-rate transparency strategy backfires and the stock pays for the precision.