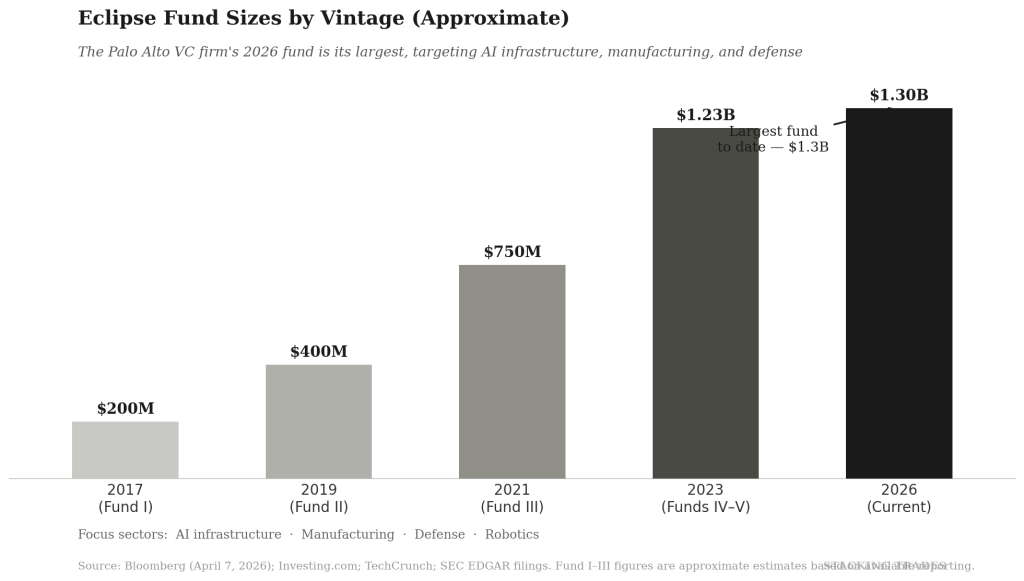

Venture capital firm Eclipse disclosed a $1.3 billion fundraise this week in filings with the Securities and Exchange Commission, making it the firm’s largest fund to date. The capital is split across two vehicles: $720 million for early-stage startups and $591 million for later-stage deals. The target sectors are AI infrastructure, manufacturing, and defense — not another frontier language model.

The timing matters. Eclipse is closing its fund in the immediate wake of a quarter in which $300 billion flowed into global startups, with 65 cents of every venture dollar going to four companies: OpenAI, Anthropic, xAI, and Waymo. That concentration is historically extreme. And Eclipse is making a direct argument — embedded in the fund’s structure and its decade of investments — that the next chapter of AI will be written in steel, silicon, and supply chains rather than in another generation of chat interfaces.

The Thesis That Was Early, Then Right, Then Crowded — Now Urgent

Eclipse was founded in 2015 by Lior Susan, a former Israeli Defense Forces special forces officer who had previously led the hardware investment platform at Flex, a multinational manufacturer. Susan’s original pitch to limited partners was unfashionable by design: he argued that the physical industries underpinning global GDP — manufacturing, energy, agriculture, logistics, defense — were ripe for digital transformation at a moment when the rest of the venture industry was chasing SaaS multiples.

The argument is now a mainstream thesis. In a statement accompanying the fundraise, Eclipse said it has spent the past 11 years building an ecosystem focused on “national strength, sovereignty and security.” That language would have sounded unusual in 2015. In April 2026, with oil above $112, an Iran war anchoring commodity markets, and every major Western government accelerating defense technology procurement, it reads as a market call with geopolitical tailwinds.

The firm’s portfolio tracks the evolution of that thesis. Known investments include Wayve, the British self-driving software company, and Redwood Materials, which recycles battery supply chains — two bets on physical infrastructure that have attracted significant co-investment from strategics. Eclipse was also an early backer of Cerebras Systems, the AI chipmaker that filed confidentially for an IPO in February 2026 and is targeting a $23 billion Nasdaq listing as early as this month.

“Companies in physical industries are built differently.”

— Eclipse, fund announcement statement, April 2026

Why Physical AI Is Having Its Moment

The term “physical AI” has been circulating in venture conversations for roughly two years, but it only started attracting serious capital in Q1 of this year. Crunchbase data shows that among the 10 companies that raised $1 billion or more in Q1 2026 outside the frontier lab megarounds, the sectors spanned generative and physical AI, autonomous vehicles, semiconductors, data centers, robotics, and defense — a pattern that reflects where applied AI is generating deployable, contract-backed revenue rather than consumer growth stories.

Defense technology is part of that shift. In 2025, the value of venture capital deals in the sector hit a record $49.1 billion, up from $27.2 billion the prior year, according to PitchBook data. The number of venture firms actively investing in defense tech increased 41% in 2025 alone, as institutional investors reframed defense as national-interest infrastructure rather than an ethically fraught sector. The question heading into 2026 was not whether defense tech would attract capital — it was which firms had the operational relationships to differentiate their deal flow.

Eclipse’s answer is its operator-first model. The firm’s investment team includes executives with backgrounds at Apple, Amazon, Samsara, and Bridgewater, and it runs an in-house venture-equity arm that incubates companies from scratch alongside its fund capital. That structure, which sits between a traditional VC and a holding company, has given Eclipse visibility into industrial supply chains, DoD procurement timelines, and manufacturing bottlenecks that most software-focused funds do not have.

The Cerebras Overhang

The fund announcement lands at a delicate moment for Eclipse’s most visible portfolio bet. Cerebras Systems, where Susan sits on the board, is pursuing a public listing that has already been delayed once due to national security review of a UAE-based investor and customer. Cerebras refiled confidentially in February 2026 after raising a $1 billion Series H that valued the company at $23 billion — nearly three times its previous valuation from October’s aborted IPO attempt.

The company’s technology is genuinely distinct: its wafer-scale engine, the WSE-3, packs 900,000 compute cores on a single chip roughly the size of a dinner plate, and the company claims inference speeds of more than 2,000 tokens per second versus single-digit hundreds from comparable Nvidia GPU configurations. In January, OpenAI signed a $10 billion compute deal with Cerebras, making it the largest non-Nvidia AI infrastructure supplier to win an OpenAI contract. That deal effectively addressed the most damaging knock against the company heading into its first IPO attempt — excessive customer concentration in a single UAE-based client that had drawn CFIUS scrutiny.

A successful Cerebras listing would mark the first major AI hardware exit for Eclipse. It would also validate the firm’s decade-long argument that the physical infrastructure of artificial intelligence — the chips, the data centers, the supply chains — is where durable franchise value gets built, not in the software running on top of it.

The Structural Argument for the Unfashionable Bet

There is a contrarian case embedded in Eclipse’s timing. When a single quarter concentrates 65% of global venture dollars into four companies, the remainder of the market compresses. Early-stage valuations in sectors that are not frontier AI have softened, deal terms have improved for lead investors with domain expertise, and the talent market for hardware engineers and manufacturing specialists has remained less frothy than the software equivalent.

Morgan Stanley’s global thematic research team flagged the same structural argument in a recent outlook, recommending self-sufficiency plays in energy, critical materials, manufacturing capacity, and AI capabilities. The recommendation is directed at public-market allocators, but the underlying logic — that geopolitical fracturing creates durable demand for domestic industrial capacity — is the same bet Eclipse has been making since 2015.

The $1.3 billion is Eclipse’s largest raise to date, topping the $1.23 billion it raised across two funds in 2023. It is not a radical departure from what the firm has always done. But the context in which it lands — record frontier lab megarounds, surging defense budgets, geopolitical instability driving oil above $100, and a Cerebras IPO potentially weeks away — makes this a fund that is easy to read as a crowded-market hedge.

WHAT TO WATCH NEXT

- Whether Cerebras prices its Nasdaq listing in April or slips to Q2, and where the initial trading range settles relative to the $23 billion private valuation — the outcome will test Eclipse’s largest known public exit.

- DoD fiscal year 2027 budget line items for autonomous systems, AI-enabled manufacturing, and collaborative combat aircraft, which will define the addressable market for the next wave of Eclipse-style defense tech investments.

- VulcanForms and other Eclipse portfolio companies in advanced manufacturing: whether they can demonstrate the production-at-scale milestones that PitchBook analysts say will separate winners from overcapitalized also-rans in the defense tech cohort.

- How LPs in frontier AI-heavy funds respond if the OpenAI or Anthropic IPO processes extend into 2027 — and whether physical AI funds benefit from reallocation pressure in late 2026.