{kind=link}

The SpaceX IPO is being covered as a milestone. It is also a stress test — for private market valuations, for passive index fund mechanics, and for the pre-IPO vehicle ecosystem that has spent four years building toward this moment. The milestone is the easy part. The stress test is what sophisticated investors need to be thinking about before the S-1 drops.

SpaceX filed its confidential draft registration statement with the SEC on April 1, 2026. The public prospectus is expected in the May 20 to 22 window based on SEC timing rules and the reported June 8 roadshow start, with pricing targeting June 11 and a Nasdaq debut under ticker SPCX on June 12. Goldman Sachs holds the lead left position in a 21-bank syndicate that also includes Morgan Stanley, Bank of America, Citigroup, and JPMorgan. The company is targeting a raise of up to $75 billion at a valuation between $1.75 trillion and $2 trillion — both figures reported, neither confirmed in a public filing. A 5-for-1 stock split is expected to complete around May 22, adjusting the per-share fair market value from $526.59 to approximately $105.32.

The financials available before the public S-1 are partial and drawn from secondary reporting rather than audited disclosures. SpaceX generated $18.67 billion in revenue in 2025 and posted a net loss of $4.94 billion, with the loss driven largely by costs associated with the February 2026 all-stock merger with xAI. Starlink, the satellite internet division, contributed $11.4 billion of that revenue and delivered operating profit of $4.42 billion — the only confirmed profit center in the business and the primary anchor for any valuation argument above $1 trillion.

What the Nasdaq Rule Change Actually Does

On March 30, Nasdaq approved two changes to how stocks enter the Nasdaq-100 index. The standard six-month seasoning period was cut to 15 trading days for any newly listed company whose market capitalization ranks among the top 40 in the index. The 10% minimum public float requirement was eliminated entirely. The rules took effect May 1. SpaceX is selling less than 5% of its shares in the IPO and will easily rank among the largest Nasdaq-listed companies at any reported valuation above $1.75 trillion. The rule changes were written, effectively, for this deal.

The consequences for passive investors are mechanical and immediate. Invesco QQQ Trust alone held $385 billion in net assets as of May 1, 2026 — one product among many tracking the same index. Every dollar in a Nasdaq-100 ETF is already invested. To make room for a new mega-cap, the fund must sell every other holding proportionally on the inclusion date. ETF strategist Dave Nadig has estimated that decision will force Nasdaq-tracking funds to buy roughly $7 billion of SpaceX stock in a single day. Former JPMorgan executive Chan Ahn puts the full ecosystem impact considerably higher.

“IPO euphoria and forced institutional demand now happen simultaneously, not sequentially.”<

— Chan Ahn, former JPMorgan executive, Benzinga, May 2026

Ahn estimates the rule change could trigger roughly $22 billion to $27 billion in forced buying from physically backed index funds alone, with potentially $60 billion or more across the broader Nasdaq-100 ecosystem. That demand arrives before SpaceX reports a single public earnings number and before insider lockups expire. In a normal listing, institutional investors decide whether to buy. In this one, a material share of institutional buying is non-discretionary — a function of index mechanics, not valuation judgment. The Wall Street Journal’s Jason Zweig called the Nasdaq fast-entry rule “arbitrary, unfair and potentially risky.” S&P Global is separately considering whether to accelerate its own inclusion rules, with feedback reportedly due by May 28 and a possible rule implementation before the June 8 roadshow opens.

The Private Market Valuation Gap

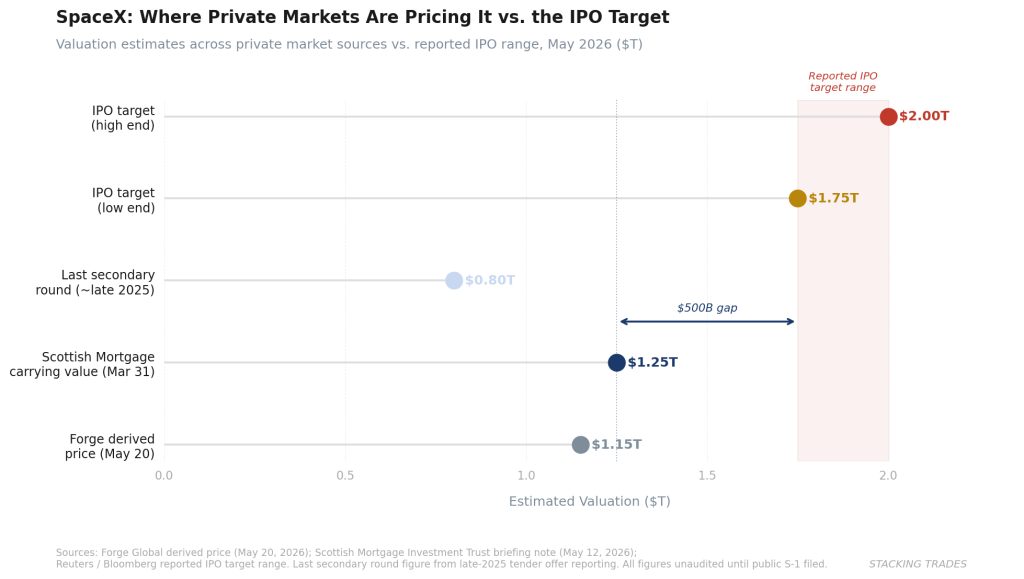

The most useful real-world benchmark for SpaceX’s private valuation is Scottish Mortgage Investment Trust, which disclosed in a May 12 briefing note that it values its SpaceX stake at $1.25 trillion as of March 31, 2026. Baillie Gifford’s valuation team, working with S&P Global as an independent third-party provider, values private holdings based on verifiable transactions rather than press reports — a methodology that deliberately places Scottish Mortgage’s carrying value $500 billion below the $1.75 trillion figure circulating in the press. Scottish Mortgage’s initial $200 million investment in SpaceX in 2018 has multiplied roughly nineteen-fold. The stake represents close to 20% of total fund assets. The trust has been issuing new shares at a premium to NAV in May — a technical signal that the IPO expectation has already repriced the fund above its intrinsic value, before SpaceX prints a single public share price.

That gap — $1.25 trillion versus $1.75 trillion — is the number that matters most for private market investors. Every LP, secondary buyer, and pre-IPO fund vehicle that has marked SpaceX exposure anywhere between those two figures is sitting on a valuation that will be resolved definitively at pricing. For vehicles that have marked at or above $1.75 trillion, the IPO is a confirmation event. For those that have been conservative — and Scottish Mortgage’s methodology suggests some managers have been — it is a mark-up. For any vehicle that followed secondary market rumors toward $2 trillion, a pricing at $1.75 trillion is a write-down on day one.

The secondary market on Forge reflects this uncertainty in real time. As of May 20, Forge’s derived price for SpaceX shares stood at $650.66 — a figure the platform calculates from secondary transactions, primary funding data, and indications of interest across private market platforms. That price implies a valuation in the low trillions, broadly consistent with the $1.25 to $1.75 trillion range where institutional managers appear to be anchoring. It is not consistent with the $2 trillion figure that has appeared in some reporting.

The Downstream Effects on Private Market Vehicles

For investors holding SpaceX exposure through the ecosystem of pre-IPO funds, closed-end vehicles, and secondary market positions, the IPO creates a set of decisions that the coverage has largely not addressed.

Lock-up mechanics are the first. SpaceX has not disclosed its lock-up structure in any public filing. Scottish Mortgage said explicitly in its May 12 briefing that it does not yet know what restrictions will apply to existing shareholders post-listing, how long any lock-up period will last, or whether the trust will be subject to different terms than other pre-IPO investors. That uncertainty applies to every vehicle holding pre-IPO shares. A standard 180-day lock-up would place the first insider supply event in December 2026 — after the Q3 earnings cycle, into a market that will be navigating holiday liquidity conditions.

The index inclusion mechanics compound the lock-up dynamic. If $22 billion to $60 billion in forced Nasdaq-100 buying arrives within 15 trading days of the June 12 debut — while pre-IPO holders are locked out of selling — the inclusion-day price discovery reflects non-discretionary demand against a float representing less than 5% of the company. Any fund manager with actual valuation conviction trying to sell into that environment cannot. Any fund manager with no valuation conviction — index trackers — must buy regardless. The result is a price set by the least informed buyers in the market, buying into artificial supply scarcity, before a single lock-up has expired.

Retail investor allocation adds another layer. SpaceX is reportedly planning to allocate up to 30% of shares to individual investors — roughly three times the industry norm. On a $75 billion raise, that translates to approximately $22.5 billion in retail allocation. Combined with forced index buying, the demand architecture for the opening sessions is dominated by two categories of buyer who share a characteristic: neither is making a valuation decision. One is buying because they are excited. The other is buying because their fund has no choice.

What This Means for the Broader Pipeline

The private market effects of the SpaceX listing extend beyond SpaceX holders. As we noted in our analysis of prediction market signals in private company valuations, the pricing of SpaceX at IPO will function as the reference transaction against which every other large private company in the U.S. market gets re-marked. Anthropic, OpenAI, Anduril, Databricks — all have private valuations that will be tested against whatever SpaceX establishes as the public market’s willingness to pay for an AI-adjacent, mission-driven technology platform with a mix of recurring and government revenue.

A SpaceX pricing at $1.75 trillion on Starlink’s proven $4.42 billion in operating profit implies a roughly 400 times operating profit multiple — a number that is only defensible if the market treats it as an infrastructure platform rather than a technology company, and only sustainable if Starlink’s margin trajectory improves materially as the constellation matures. A pricing at $2 trillion on the same earnings base makes that argument harder. Either outcome sets a ceiling or a floor for what institutional allocators are willing to pay for the OpenAI and Anthropic prospectuses that follow.

S&P Global’s analysis suggests SpaceX, OpenAI, and Anthropic together could account for 2.9% of the S&P Global Index’s weighting once public — roughly equivalent to the entire Canadian market’s current weight. The index mechanics that have been engineered to accelerate inclusion for SpaceX will apply to those offerings as well. The SpaceX IPO is not a one-time event. It is the template for how the next wave of private giants enters public markets. Every passive investor with a Nasdaq or S&P 500 index fund exposure owns a stake in whether that template is set responsibly.

What to Watch Next

- The public S-1 prospectus on SEC EDGAR. The audited financials — Starlink subscriber economics, xAI integration costs, the precise use of proceeds, and the lock-up structure for existing shareholders — are the only numbers that matter. Every figure in current circulation is unverified. The prospectus resolves that.

- S&P Global’s index rule decision, feedback deadline May 28. If the S&P 500 accelerates its own inclusion timeline for SpaceX, the forced-buying dynamic extends well beyond Nasdaq-100 trackers. SPY alone holds more than $600 billion in assets. Any rule change before the June 8 roadshow open materially changes the demand architecture for the offering.

- Lock-up terms in the S-1. Scottish Mortgage does not yet know its lock-up structure. Neither does anyone else. The terms will determine when insider and early LP supply enters the market — and whether the December 2026 lock-up expiration creates a sell event into what may be a thinner holiday tape.

- Pre-IPO fund NAV disclosures through May. Any closed-end fund or pre-IPO vehicle that publishes a May 31 NAV will be marking SpaceX against the reported $1.75 to $2 trillion range. The spread between those marks and the eventual IPO price is the realization P&L for every LP in those vehicles.

- Starlink Q1 2026 subscriber and revenue figures in the S-1. Starlink ended 2025 with 10 million subscribers and $11.4 billion in revenue. Analysts project $15.9 to $24 billion in 2026 revenue from the division. The S-1’s Q1 figures will show whether that ramp is tracking — and whether the operating margin improvement that justifies the $1.75 trillion anchor is materializing on schedule.